How does a tax-managed mutual fund work?

Executive Summary:

- Tax-managed mutual funds are becoming popular because they help minimize an investor’s tax burden

- They use a variety of strategies to minimize taxable transactions

- Tax-managed mutual funds aim to minimize capital gains

Everybody loves a bargain - Buy one, get one free. The diner’s daily special. Your favorite clothing store holding a sale. Most of us jump at the chance to save money.

Our desire to keep more of our money in our own hands is one reason why tax-managed mutual funds have become so popular in the United States and are likely to become more popular in Canada. Amid volatile markets, rising inflation, higher taxes and other issues that are nipping at our portfolios and pocketbooks, we all look for ways to keep more of our money working for us. Tax-managed mutual funds can help us do that.

These unique mutual funds are designed to minimize the embedded year-end capital gain distributions that trigger capital gains taxes. This is important because these taxes can impact the value of a taxable portfolio.

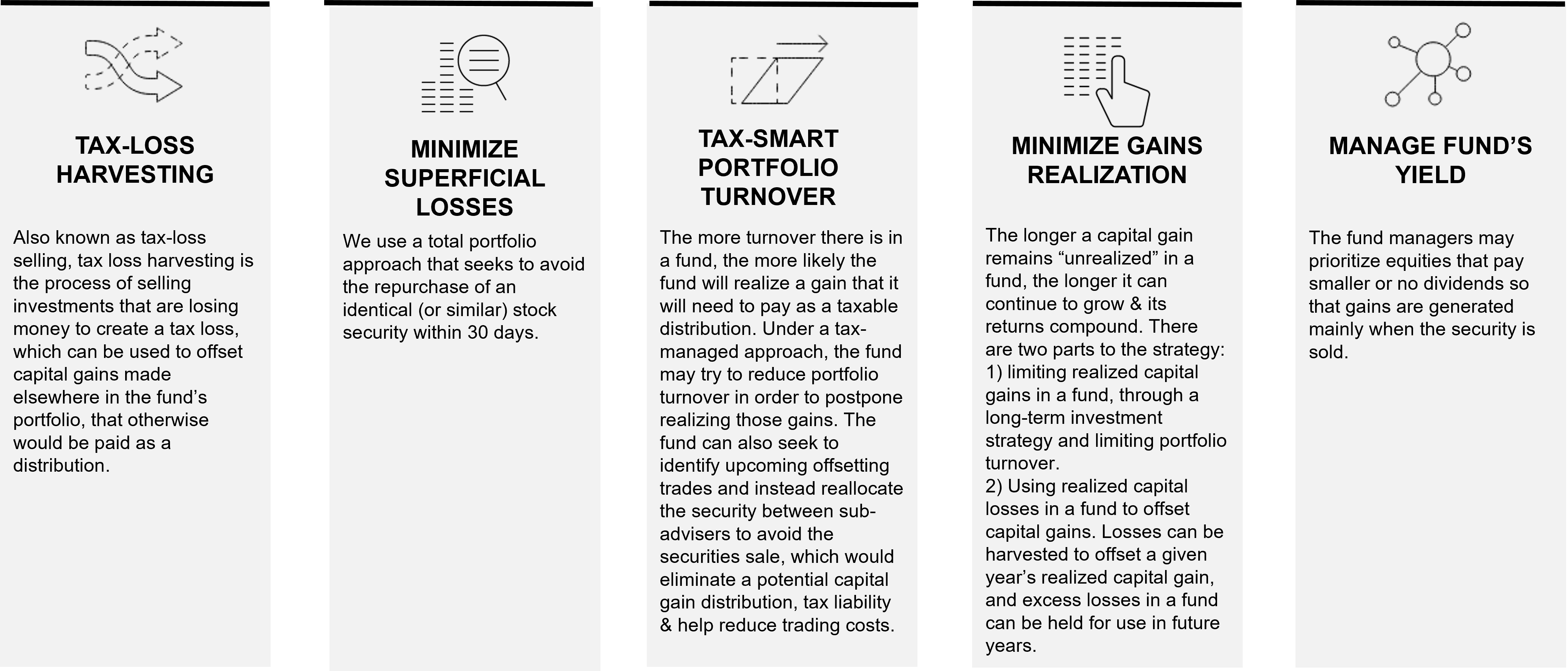

The objective of a tax-managed mutual fund is to generate returns via price increases, while avoiding annual capital gain distributions. Their investment objectives are generally to provide returns similar to non-tax managed funds, but tax-managed mutual funds also aim to minimize taxable transactions within the fund itself, in order to minimize adverse tax consequences. They do this in several ways, whether by selling some stocks at a loss to offset other gains, eliminating wash sales, managing the fund’s yield, or by minimizing gains realization.

When a mutual fund is labeled as “tax-managed”, what does it mean?

When a mutual fund has words alluding to “tax-managed” or “tax-efficient” in its name, it is reasonable to expect that fund to have dual investment objectives, one of them being to minimize its investors’ tax burden. Most investment objectives found within the prospectus of equity mutual funds are “to provide long-term capital growth” or “long-term capital growth and current income”. Tax-managed mutual funds will generally include “on an after-tax basis”, “tax-managed capital appreciation”, or “a tax-efficient investment return” within the language of their stated investment objectives.

While it is true that index-focused mutual funds and exchange-traded funds (ETFs) are more tax efficient than traditional mutual funds, that is simply a byproduct of their construction and function. Many index funds have fairly low portfolio turnover and tend not to pay out distributions, but that's not always the case. Sometimes stocks get booted out of indexes with market-cap constraints or factor tilts when they no longer meet the indexes' criteria for inclusion (note: in-kind is taxable in Canada). Certain types of ETFs are more likely to make distributions, such as actively managed ETFs or currency-hedged ETFs that employ derivatives contracts.

These types of investment vehicles do not have an explicit obligation to minimize their investors’ tax burden and generally do not carry the label of “tax-managed” in their names.

How does a tax-managed mutual fund work?

Tax-managed mutual funds work in the same way that traditional mutual funds do regarding their portfolio managers buying and selling stocks, with the intention of providing a return to unitholders. Both a traditional and a tax-managed mutual fund could have the same general objective to outperform the S&P 500 Index (representing US stocks), for example, and ultimately own a similar combination of stocks to achieve that goal. The main difference is that a tax-managed mutual fund takes proactive measures to minimize taxable transactions within the fund (i.e., buying and selling of stocks).

At Russell Investments, our investment approach aims to minimize any distributions that could result in a tax liability—and all trading is centralized, eliminating the overlap common to multi-manager funds. The diagram below outlines the techniques and strategies used in tax-managed mutual funds, in order to make them tax efficient.

How tax managed mutual funds work

Click image to enlarge

We know that tax-managed mutual funds works differently than traditional mutual funds but to better understand, let’s consider the example of tax-loss harvesting, one of the key pillars of tax-managed investing. Tax-managed mutual funds proactively harvest capital losses by employing the same strategy as individuals who sell investments in their taxable investment accounts (e.g. not in a registered account such as an RRSP, TFSA, etc) to harvest losses. Whether it is the result of a significant market downturn or via the process of periodically reviewing capital gain and loss positions throughout the year, portfolio managers for tax-managed mutual funds can often proactively identify positions with unrealized losses and realize some losses in order to offset future gains. Traditional mutual funds cannot prioritize such tax-loss harvesting strategies with investments they intend to own for an extended period of time.

How do tax-managed mutual funds help investors lower their tax bill?

As we know, most traditional mutual funds distribute capital gains based on the trading activity that took place within the fund during any given year. Capital gains will be taxed at the corresponding capital gains tax rate, which can be as high as 26.75% in Ontario, for example. The unitholder must pay these taxes because of capital gain distributions, even if those distributions are reinvested back into the fund. Over a long-term investment horizon, these annual capital gain taxes can have a meaningful impact on after-tax wealth.

Tax-managed mutual funds aim to minimize or eliminate capital gain distributions. Additionally, tax-managed funds attempt to manage dividend income, which is taxed. A lower amount of dividend income results in lower taxes due.

Simply put, taxes can negatively impact your clients’ portfolios by reducing potential investment returns. Using the strategies in the diagram above to minimize this tax drag can help investors maximize their after-tax returns, giving them a potential “after-tax edge”.

As inflation and fees impact portfolios, managing the tax liabilities from distributions can be a valuable strategy to maximize after-tax wealth.

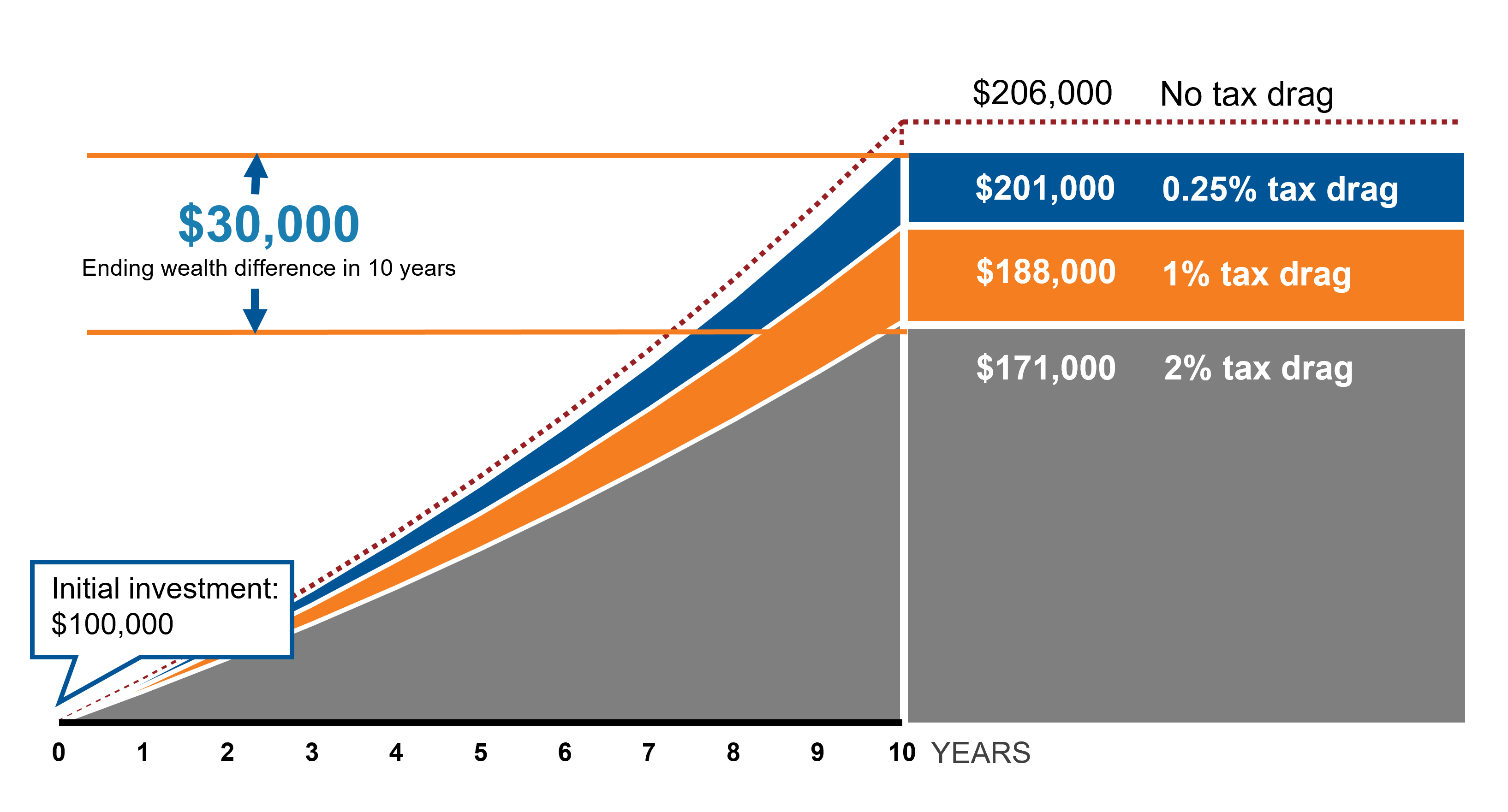

To put some visual context around this concept, consider the hypothetical example below which illustrates the difference of returns over 10 years with: no tax drag, 0.25% tax drag, 1% tax drag and finally 2% tax drag. The more you pay in taxes, the less money remains in your portfolio to potentially compound and grow. This can have a significant impact. Over 10 years, the hypothetical difference of a $100k portfolio paying 2% versus 0.25% in taxes would result in more than $30,000 in additional return.

THE AFTER-TAX EDGE – 10 YEARS

Hypothetical growth of $100,000 over 10 years at 7.5% per year1Click image to enlarge

Source: Russell Investments. 10-year hypothetical impact of taxes, assumed annual return: 7.5%1

Next steps? Understanding your clients’ tax sensitivity levels is a great place to start! Use the below checklist as a guide:

Tax-smart investing checklist

- Do you KNOW each client’s marginal tax rate?

- Do you PROVIDE intentionally different investment solutions for taxable and non-taxable assets?

- Do you EXPLAIN to clients the potential benefits of managing taxes?

- Do you HAVE a process for partnering with local Chartered Public Accountants?

- Do you REVIEW your client’s T3, T5, T5008 and other tax forms which cover distributions, income and capital gains (or losses)?

1This is a hypothetical illustration and not meant to represent an actual investment strategy. Tax drag is the reduction of potential investment returns due to taxes. Taxes may be due at some point in the future and tax rates may be different when they are. Investing involves risk and you may incur a profit or loss regardless of strategy selected.