Value and Growth Investing: How are you positioned?

Conventional wisdom has long held that value stocks and growth stocks work in different ways, and therefore wouldn’t be found in the same mutual fund. In recent years it has become increasingly difficult to tell the difference between a value and growth manager’s portfolio. With more common holdings than ever, what does this overlap mean for your investment choices and what do you need to know when constructing a portfolio for your clients?

An Unlikely Paring

The popularity of value and growth has ebbed and flowed over the years. Nearly two decades ago, with value in the doldrums, some value fund managers closed shop. But to give our clients the best chance of pursuing their financial goals, we need to stay true to what we know and remain invested for the long run regardless of which factor is driving the market. While returns on value funds have lagged their growth counterparts recently, have you ever wondered if your client portfolios are tilted more toward value or growth and how stocks are categorized as value or growth? Put more simply, how are value and growth stocks defined?

Value stocks tend to be characterized by low price-to-earnings (P/E) and low price-to-book (P/B) ratios, while growth stocks generally have high P/E and high P/B ratios. Value stocks generally have fundamentals to support higher valuations (excluding value traps), but have fallen out of favor among market participants. Growth stocks, meanwhile, may be seen as having above-average earnings growth and may also seem expensive and overvalued. But many stocks can have a mix of both characteristics.

A good example of this is Apple, the technology giant. By most holdings-based measures, it could be considered a growth stock, based on its expected earnings potential. At the same time, it could also be considered undervalued, based on a manager’s valuation. Its P/E is 20.3x, roughly the same for the Russell 1000 Index's average of 20.4x P/E. While you may have your particular view of whether Apple is a growth or value stock, both growth and value managers have good arguments to include it in their funds.

What’s in your portfolio?

Have you stopped to consider the overlap of value and growth stocks in your client portfolios? It has become increasing difficult to delineate between value and growth as many funds hold overlapping securities. For example, the overlap in stocks between one US all-cap value portfolio and the S&P 500 Growth Index is 71%, up from 60% just five years ago.1

Most fund managers use some sort of risk model to categorize stocks based on past returns or more common holdings-based measures including weighted average of P/E, P/B and possibly other factors. A recent Morningstar article found that the value funds which have performed the best recently, have been “casting a wider net” and redefining value parameters 2. For example, technology companies have larger intangible assets that may not be fully recognized by a risk model’s holdings-based measures.

Remember, leadership rotates

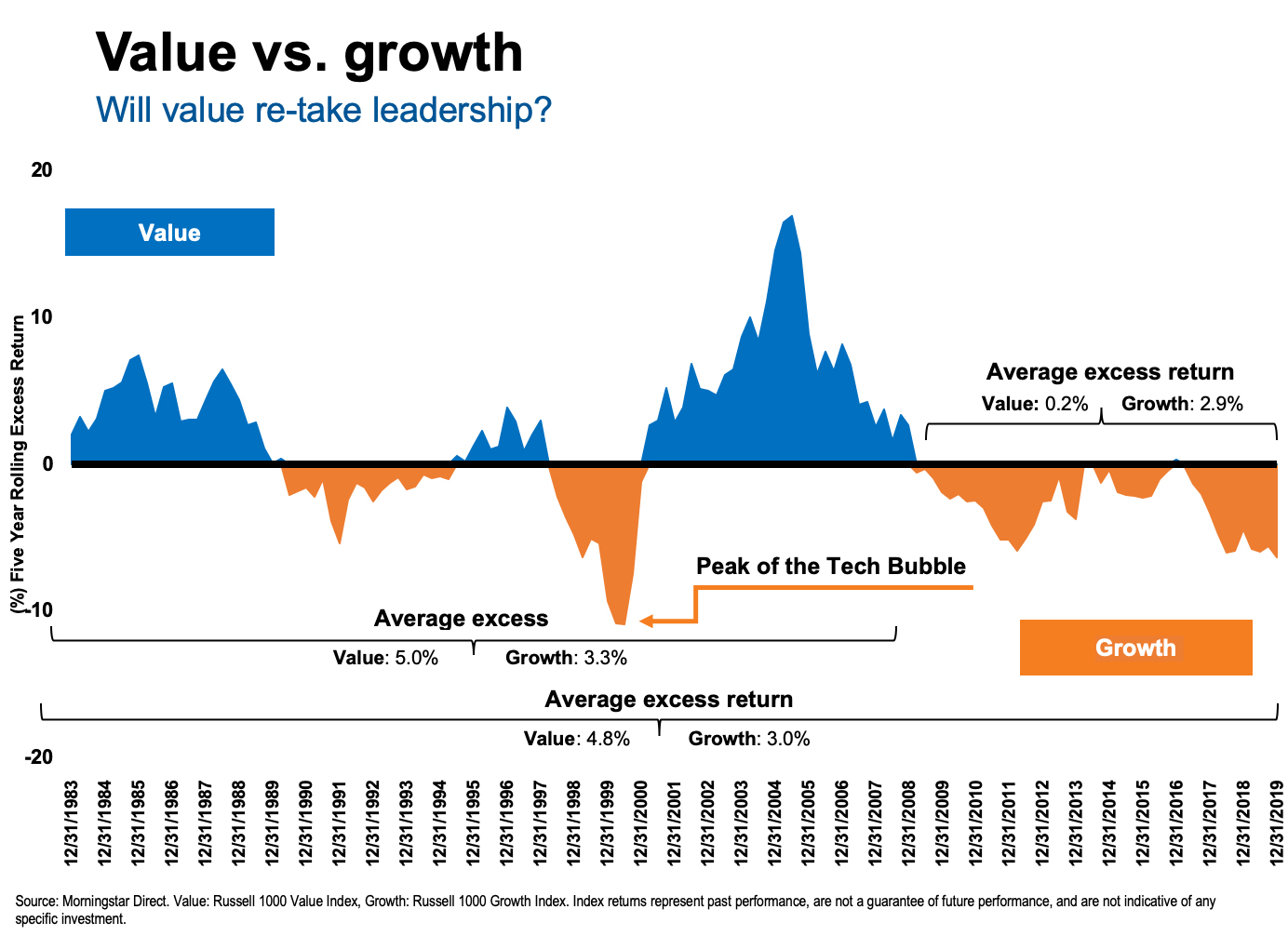

The chart below shows the rolling five-year excess return performance of the Russell 1000 Value Index, compared to the Russell 1000 Growth Index as of September 2019. As you can see, over the longer term, value has outperformed growth, which confirms the widely held notion that value outperforms growth. But since the 2008 Global Financial Crisis (GFC) to present-day, growth has outperformed. That’s an awfully long time at the top. This leads us to think value may be coming back soon to rule the roost and shows why investors should have exposure to both.

Figure 1: Value vs. growth: Rolling five-year excess return performance

Given the potential for differing views and the rotation of different factors, wouldn’t it make sense to allocate to both? We believe this to be the case. At Russell Investments, our portfolio managers often have strategic weights to both the value and growth factors within our portfolios. We believe a properly constructed portfolio should be diversified across factors to avoid periods of under performance over the entire market cycle, in much the same way as we champion global diversification.

By paying attention to overlap in your portfolios and diversifying factor risk, you’ll help your clients stand a better chance of performing well in all markets and enjoying a smoother ride along the way.

1 Source: Morningstar Direct, Russell Investments

2 www.morningstar.com October 8, 2019 “Value vs Growth: Morningstar Analysts Open Their Notebooks; “Forest lands or The Next Big Thing.