Neutral equity outlook

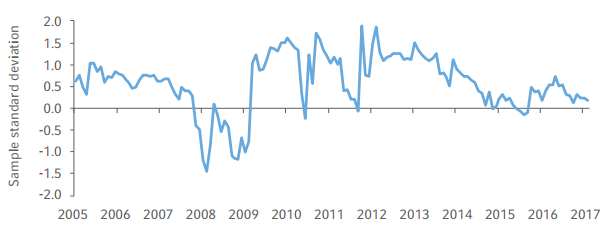

Our model for U.S. equities versus U.S. fixed income, continues to show a neutral preference as of March 15, 2017, without much change since our annual outlook report.

EAA4 U.S. equity vs. U.S. fixed income aggregate signal

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

- Business cycle: Our model that estimates the likelihood of being in a bull or bear market neutralised during the first quarter of 2017. The U.S. Business Cycle Index (BCI) still shows the economy on a path of moderate growth with low probability of recession over the next 12 months.

- Valuation: Our Fed model stayed positive, but became more muted as the earnings yield

decreased relative to bond yields.

- Sentiment: Equities are hitting historic highs. As such, the 12-month declining weighted average signal of excess equity momentum stayed positive and has steadily increased over the last quarter. However, the overall sentiment signal is slightly dampened by our mean reversion model. This contrarian model says that equities are overbought.

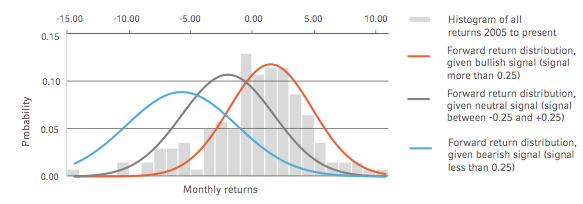

The following graph shows the distribution of forward returns, conditional on the U.S. equity/U.S. fixed income model’s signal. Given our signal is neutral, we expect a return distribution close to the dark gray line.

Distribution of returns, conditional on EAA U.S. equity vs. U.S. fixed income aggregate signal

Source: Russell Investments as of March 15, 2017.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

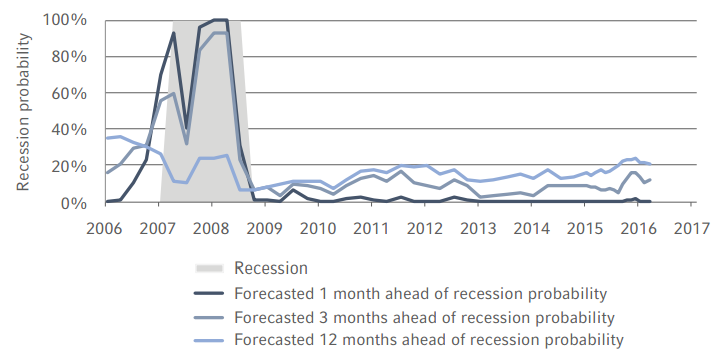

Recession probabilities: short-term risks faded

The Business Cycle Index (BCI) model uses a range of economic and financial variables to estimate the strength of the U.S. economy and forecast the probability of recession. The index estimates that the probability of recession in the next 12 months is only 20%. Risks had been gradually building over the last few years, but declined a bit recently. We conclude that a near-term U.S. recession is unlikely, but we should monitor this aging bull market cycle.

BCI model: Historical forecasted-recession probabilities

The recent decrease in recession probabilities is driven by a steepening yield curve and lower credit spreads — indicators that reflect stronger future growth expectations and lower financial risk. This optimism is echoed through a range of business, consumer and CEO surveys that show increased confidence in the U.S. economy. Although we observed a recent boost of positivity in early 2017, it may be difficult to reduce recession probabilities to the levels we saw two years ago, given we’ve already had such a long expansion. The pace of job growth is still steady but it is likely to moderate as we push toward full employment.

In addition, medium-term (two- to three-year) recession risks are building as the U.S. cycle continues to age. The unemployment rate has dropped below its sustainable level, suggesting that the labour market may be overheating. When unemployment is very low, employers are forced to bid up wages to attract the scarce pool of qualified workers, which gradually cuts into corporate profits. Firms often respond to weak profits by cutting investment and hiring, hurting consumer spending, which can feed into a negative spiral and start the onset of a recession. In the last nine economic cycles, it historically took an average of 2.5 years from the time the unemployment gap closed until the next recession.

Overall, we think that the U.S. economy is still on a path of moderate growth with low probability of recession over the next 12 months but risks are building at the three-year horizon. We’d maintain a balanced risk portfolio and look for opportunities to buy the dips and sell the rallies.

4 Enhanced Asset Allocation (EAA) is a capability that builds on Strategic Asset Allocation (SAA) by incorporating views from Russell Investments’ proprietary asset class valuation models. EAA is based on the concept that sizable market movements away from long-term average valuations create opportunities for incremental returns. The EAA Equity-Fixed Income Aggregate Signal is based on the S&P 500 and Bloomberg Barclays U.S. Aggregate Bond Index.