Quarterly market overview

June Quarter 2025

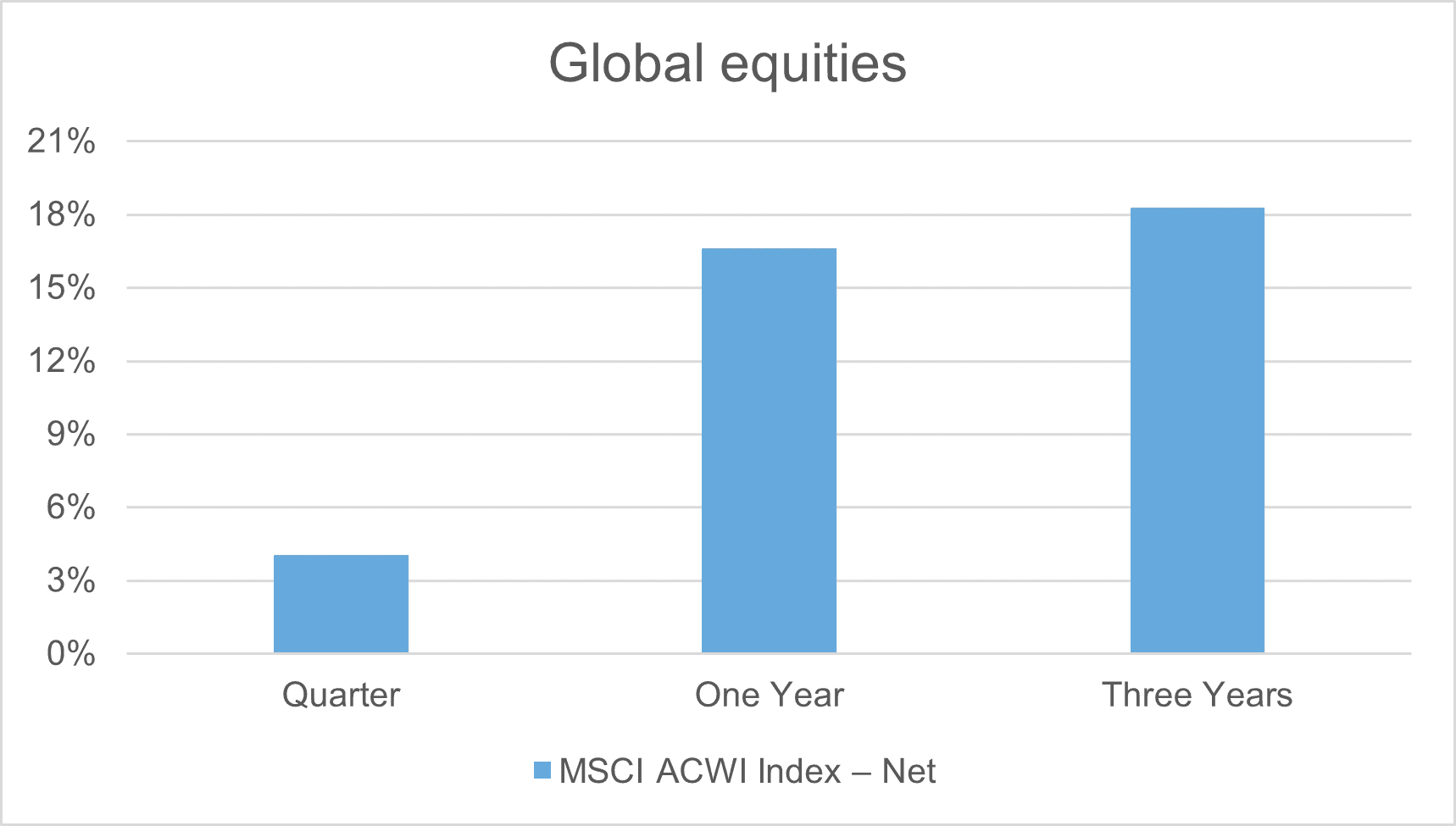

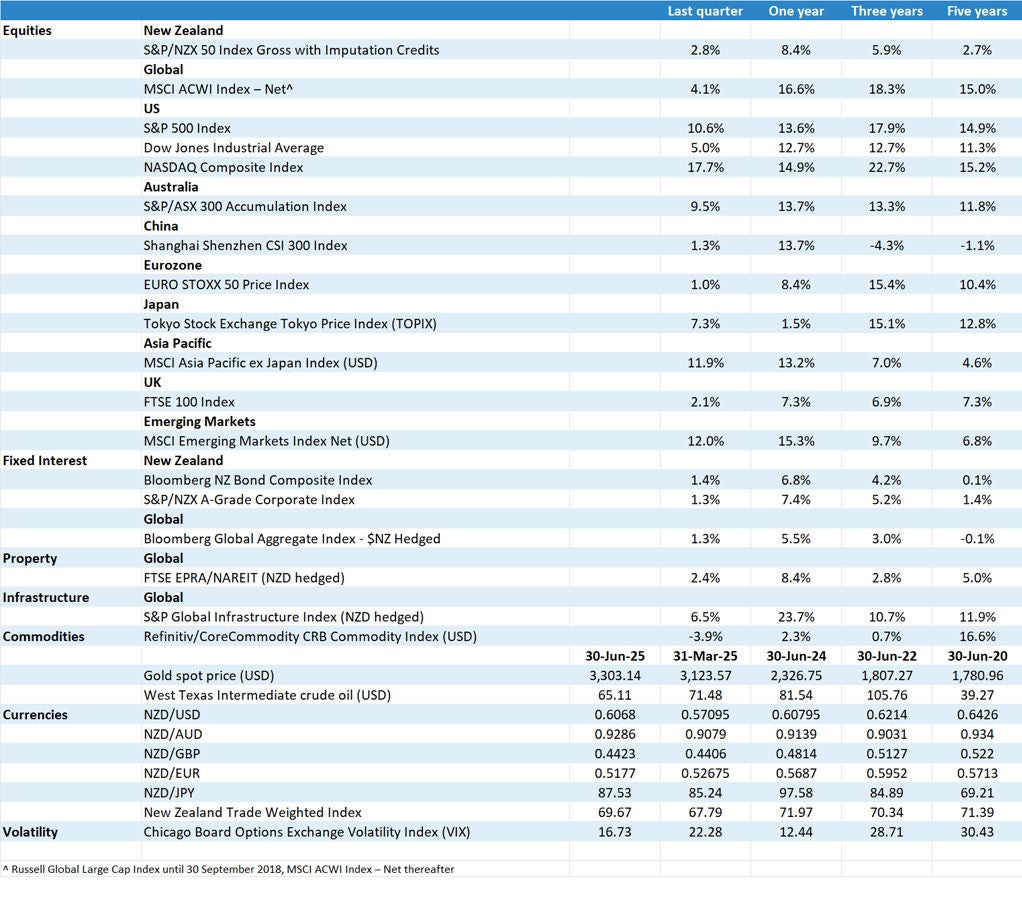

Global shares

Global share markets made good gains in the June quarter, with the MSCI ACWI Index ‒ Net returning 4.1% in unhedged New Zealand dollar (NZD) terms. Much of the gains were driven by encouraging trade developments; notably US-China trade relations. The relationship between the world’s two largest economies sunk to new lows in April following US President Donald Trump’s ‘Liberation Day’ announcement; the day on which he revealed higher-than-expected ‘reciprocal’ tariffs on over 180 countries and territories, including China. However, the two sides, who for more than a month had exchanged tit-for-tat tariff hikes, came together for talks in Geneva in early May, with officials agreeing to significantly reduce tariffs against one another for 90 days, effective immediately. Washington agreed to lower tariffs on Chinese imports from 145% to 30%, while Beijing said it would reduce levies on US goods from 125% to 10%. The outcome of the talks, which far exceeded market expectations, contributed to a strong rally across risk assets as investors pinned their hopes on the two sides using the 90-day window to strike a more comprehensive trade agreement. Perhaps highlighting the lingering tensions between the two countries, both Washington and Beijing accused the other of violating the Geneva trade agreement ahead of a second round of talks in London in June. Ultimately, though, officials were able to agree on a framework on how best to implement the terms established in Geneva. We also saw the beginnings of a US-UK trade agreement and progress in US negotiations with many of its other trading partners, including the European Union, India, Taiwan and Vietnam. Limiting the gains were concerns over America’s fiscal position after Moody’s downgraded the country’s credit rating and heightened geopolitical risks; notably escalating tensions in the Middle East after Israel and the US bombed Iranian nuclear facilities.

At the country level, the benchmark US S&P 500 Index (10.6%), the tech-heavy NASDAQ Composite (17.7%) and the Dow Jones Industrial Average (5.0%) all recorded strong gains for the quarter. In fact, both the S&P 500 Index and the NASDAQ Composite hit record highs toward the end of the period; the S&P 500 Index also topping the 6,200 mark for the first time. Stocks were also higher in Japan (7.3%1), UK (2.1%2 ) China (1.3%3 ) and the Europe (1.0%4 ).

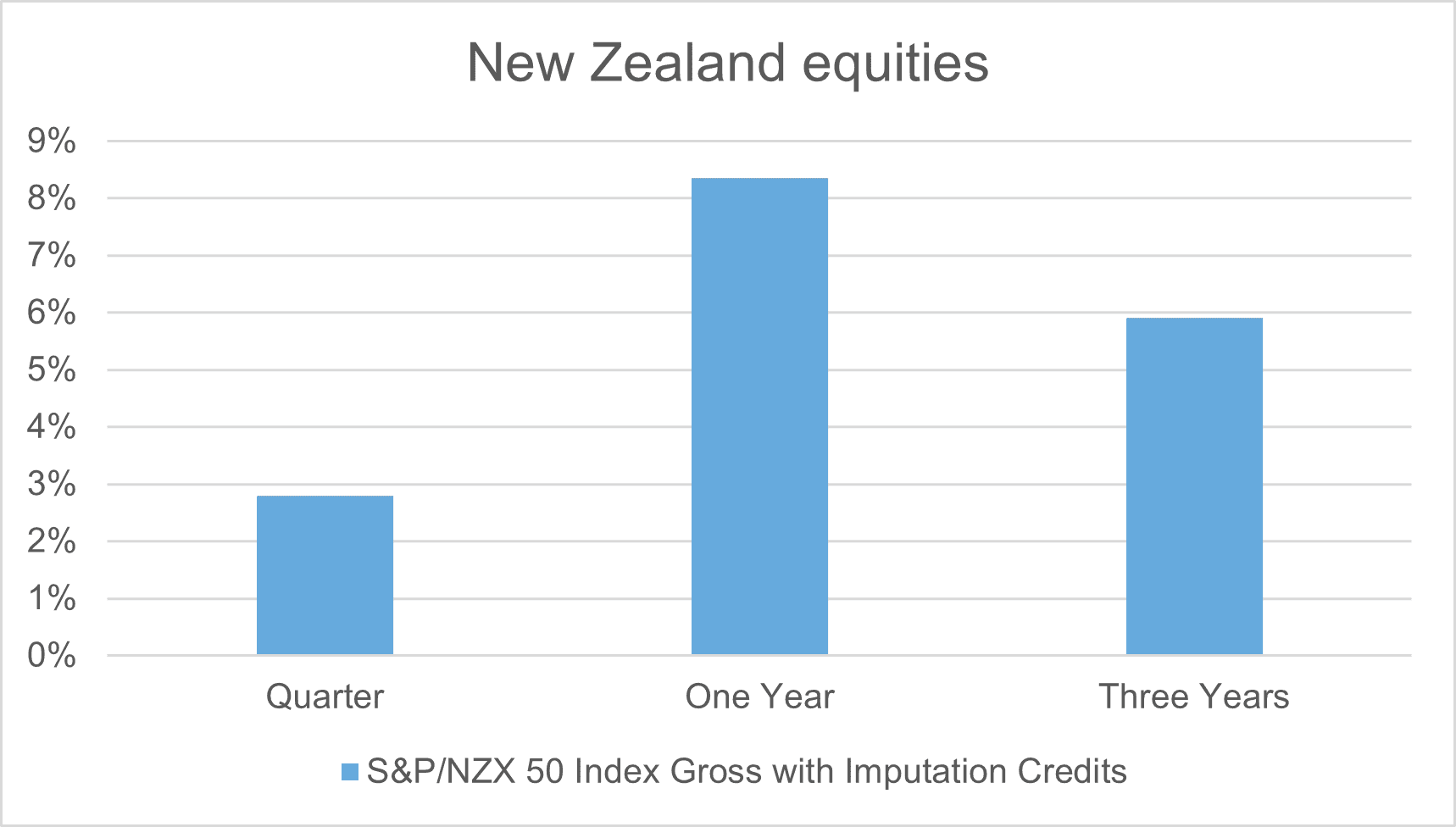

New Zealand shares

The New Zealand share market underperformed its global counterparts over the period; the local market returning 2.8%5 . Like its global peers, the New Zealand market benefited from improving trade relations between Washington and Beijing. Stocks also benefited from further domestic rate cuts, with the Reserve Bank of New Zealand (RBNZ) lowering the official cash rate twice over the period. The Bank cut by 0.25% at both its April and May meetings (the RBNZ didn’t meet in June), taking the official cash rate to 3.25%. The RBNZ has now cut interest rates by 2.25% since it began its easing cycle in August last year. In the Bank’s May posting-meeting statement, officials noted that the New Zealand economy is recovering after a period of contraction, with high commodity prices and lower interest rates supporting overall economic activity. The Bank added that inflation is within the 1-3% target band and officials remain well placed to respond to domestic and international developments to maintain price stability over the medium term. [Note: the RBNZ left the official cash rate on hold at 3.25% following its early July gathering.] The local market also benefited from stronger-than-expected growth in China – our largest trading partner – and some encouraging earnings results; though many companies who reported better-than-expected earnings did warn of uncertainty moving forward due to Trump’s tariff agenda.

At the sector level, energy, communication services and real estate recorded the biggest gains for the quarter. Healthcare and utilities also performed well, while materials, consumer discretionary and industrials trailed the broader market.

Australian shares

Australian shares made very strong gains, with the S&P/ASX 300 Accumulation Index closing the quarter up 9.5%. Much of the market’s advance was driven by positive developments in US-China trade relations. China is Australia’s largest trading partner and a key consumer of the country’s commodities. Stocks also benefited from the Reserve Bank of Australia (RBA)’s decision to cut interest rates in May; the central bank lowering the official cash rate by 0.25% to 3.85%. It was the RBA’s second rate cut this year and came amid further evidence that price pressures continue to ease. Speaking after the meeting, RBA Governor Michele Bullock flagged the prospect of additional rate cuts if inflation remains sustainably within the Bank’s 2-3% target range. Bullock also revealed that officials had considered cutting rates by 0.50% (to 3.60%). The implication that the RBA’s thinking had shifted from gradual rate reductions to a willingness to cut more aggressively if needed saw the market move to price in up to three additional rate cuts by the end of the year. More broadly, the market benefited from strong gains across most of the ‘Big Four’ banks – notably index heavyweight Commonwealth Bank of Australia, which returned more than 22% for the quarter – and encouraging Chinese growth.

Global listed property

Global listed property made good gains in the second quarter, returning 2.4%6 in hedged NZD terms. Property stocks, like other growth assets, benefited largely from the trade agreement struck between Washington and Beijing. The market was also supported by mostly lower long-term government bond yields. At the regional level, Australia posted the biggest gains, followed by Continental Europe, Asia ex Japan, the UK and Japan. North America recorded positive returns for the quarter; though this disguised mixed country performances, with Canada posting strong gains while the US trailed the broader market. In terms of sectors, US technology-related names and Japanese developers were amongst the best performers, while US residential and industrial stocks were noticeably weaker.

Global listed infrastructure

The global listed infrastructure market performed well over the period, returning 6.5.%7 in hedged NZD terms. Emerging markets recorded the biggest gains for the quarter, driven by strong returns in Mexico, Brazil and China; the latter benefiting from better-than-expected growth and Beijing’s promise of further stimulus measures. Japan, Continental Europe, the UK and Australia also performed well, while Asia ex Japan was relatively flat. At the sector level, water utilities, airports and marine ports were amongst the best performers over the period. In contrast, energy-related names struggled on the back of sharply lower oil prices.

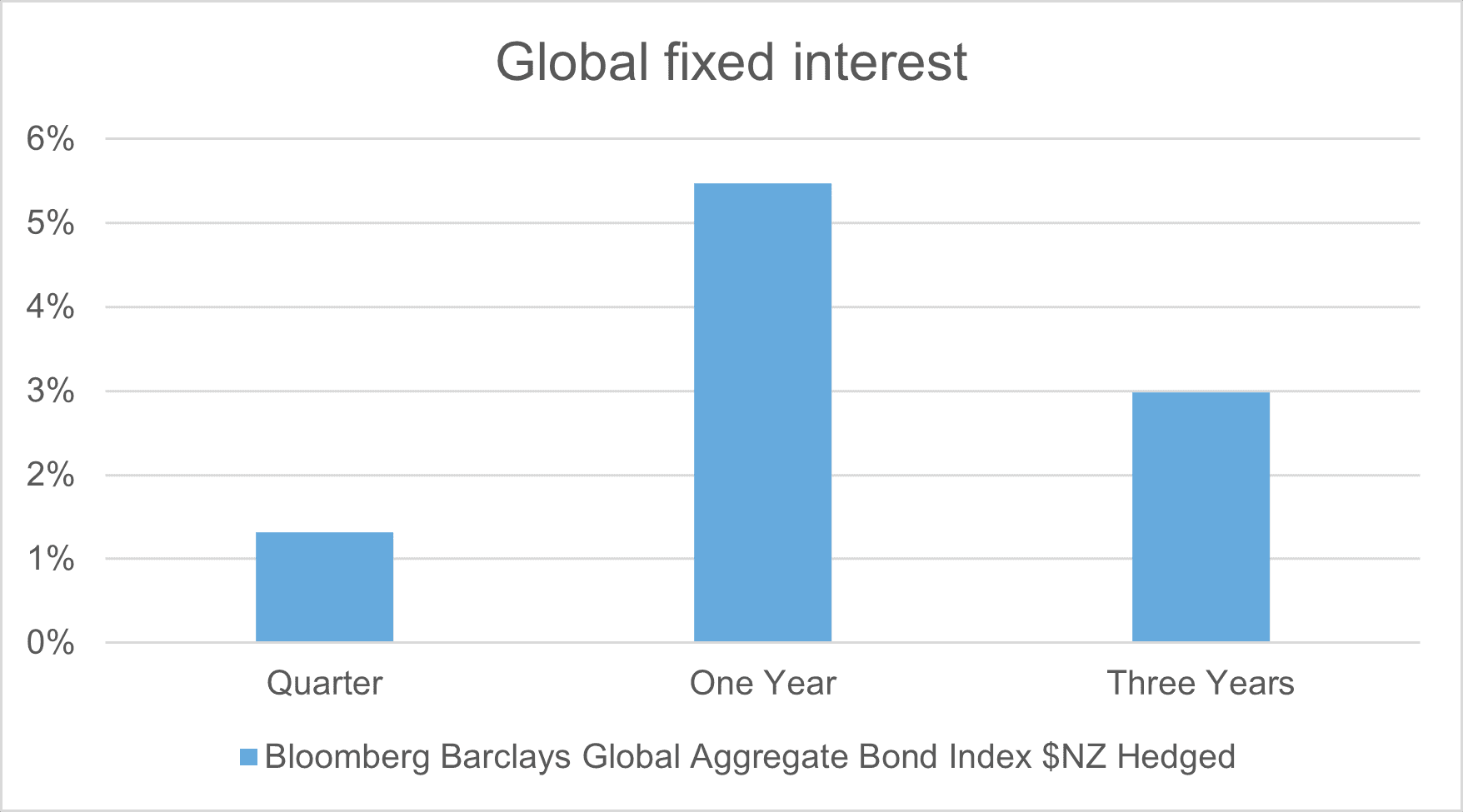

Global fixed income

Global bonds were positive for the quarter, returning 1.3%8 in hedged NZD terms. Longer-term government bond yields were mostly lower (prices higher) over the period, driven in part by the asset class’s traditionally defensive characteristics in the wake of Trump’s sweeping tariff announcement and heightened geopolitical risks. Limiting the gains were expectations of fewer US interest rate cuts this year and concerns over America’s fiscal position after Moody’s downgraded the country’s credit rating. Global credit markets were stronger for the quarter, with spreads on US and European investment-grade and high-yield debt tightening over the period. Hard and local currency emerging markets debt also performed well.

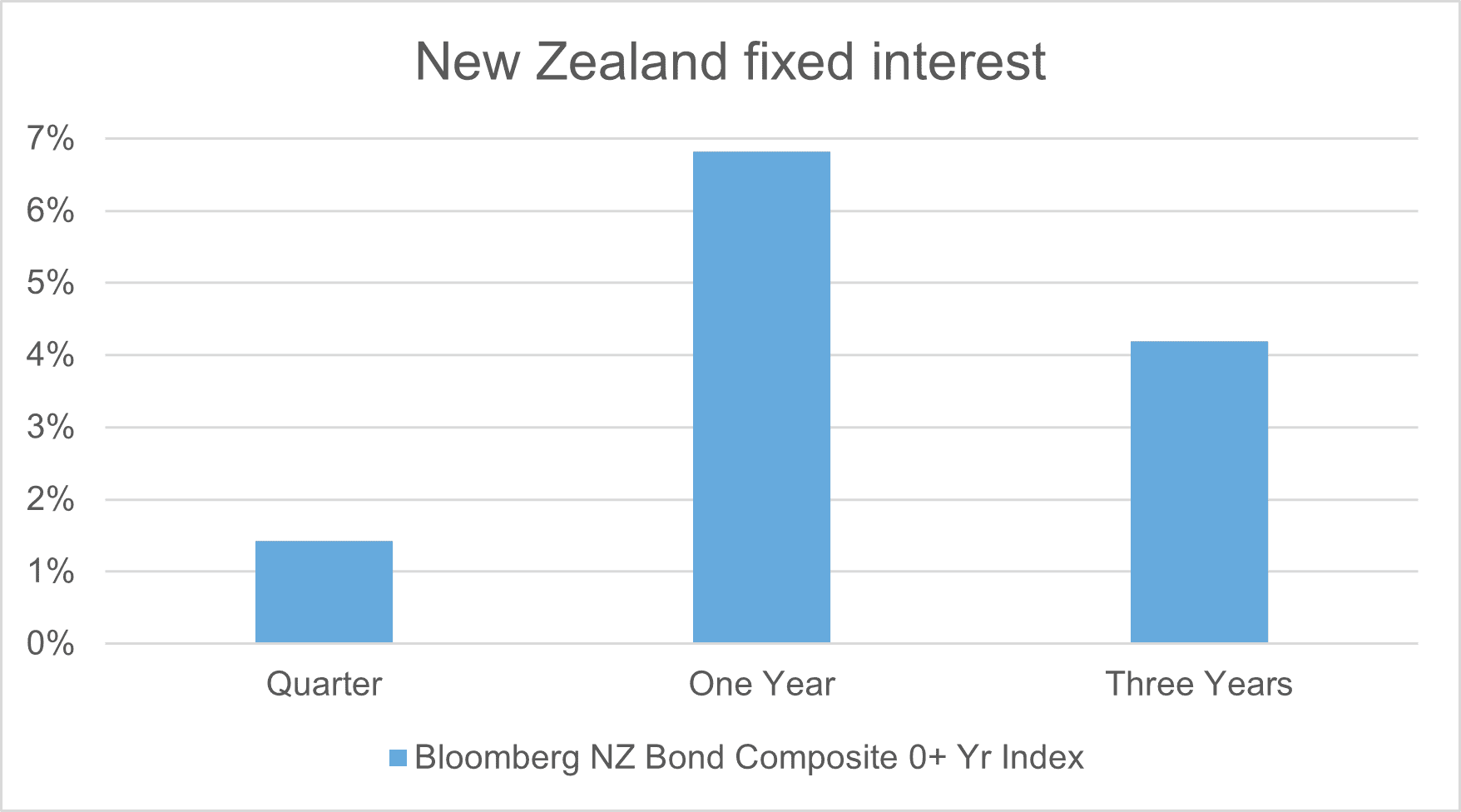

New Zealand fixed income

The New Zealand bond market made reasonable gains over the period, returning 1.4%9. Domestic long-term government bond yields rose (in aggregate) in the second quarter; though only modestly. Like its global counterparts, the local bond market benefited from its traditionally defensive qualities amid heightened trade and geopolitical risks. Partly offsetting this was the RBNZ’s more cautious tone regarding the pace of future rate cuts following its May gathering. The yield on New Zealand 10-year government debt closed the quarter just four basis points higher at 4.5350%. Local credit markets were slightly weaker, with spreads widening over the period.

New Zealand dollar

The New Zealand Trade-Weighted Index10 rose 2.8% in the second quarter, driven largely by US dollar (USD) weakness; the USD falling sharply amid Trump’s tariff agenda, a deteriorating growth outlook and concerns over the country’s ballooning debt. The local currency also benefited from hopes the US and China can work out their trade differences. Limiting the advance were further RBNZ rate cuts and heightened geopolitical uncertainty. The NZD gained 6.3% against the USD, 2.7% against the Japanese yen, 2.3% against the Australian dollar and 0.4% against the British pound. It fell 1.7% against the euro.

^ Russell Global Large Cap Index until 30 September 2018, MSCI ACWI Index ‒ Net thereafter

Note: all returns are in local currencies unless otherwise stated.

Disclaimer

The information contained in this publication was prepared by Russell Investment Group Limited. It has been compiled from sources considered to be reliable, but is not guaranteed. This publication provides general information only and should not be relied upon in making an investment decision. Before making an investment decision, you need to consider whether this information is appropriate to your objectives, financial situation and needs. All investments are subject to risks. Past performance is not a reliable indicator of future performance.

Copyright © 2025 Russell Investments. All rights reserved. This information contained on this website is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments.

1 Tokyo Stock Exchange Tokyo Price Index (TOPIX)

2 FTSE 100 Index

3 Shanghai Shenzhen CSI 300 Index

4 Dow Jones EuroStoxx 50 Price Index

5 S&P/NZX 50 Index with imputation credits

6 FTSE EPRA/NAREIT Developed Real Estate Index Net NZD Hedged

7 S&P Global Infrastructure Index (NZD hedged)

8 Bloomberg Global Aggregate Index – $NZ Hedged

9 Bloomberg NZ Bond Composite 0+ Yr Index

10 The trade-weighted index for the NZD is an indicator of movements in the average value of the NZD against the currencies of our major trading partners.