California love … but not so much the taxes

Between the beautiful weather, excellent cuisine and some of the country’s best beaches, there’s a lot to love about being a California resident. From San Diego to Orange County to the Venice and Santa Monica beaches, we find near-perfect weather and a great outdoor lifestyle. Some of the world’s best wines come from the Central Coast, Napa and Sonoma. The Bay Area is known as the technology hub of the U.S. And let’s not forget the farmlands of the Central Valley, the source of so much of the wonderful cuisine enjoyed in California! So much to love, in fact, that California is home to almost 40 million people. With a population greater than that of America’s other two most popular sunny states—Texas and Florida—the Golden State has staked its claim as the world’s fifth-largest economy—as measured by gross domestic product (GDP)—for several years in a row.

Where we choose to live is a choice, and in the case of most Californians, the feeling is well, yeah! Made a great choice. But choices often come with costs, and in the case of California that could come in the form of what is known as the sunshine tax. That's because California is also famous for having high taxes—in fact, the highest in the nation. Residents of California can be subject to tax rates on investment income as high as 54.1%. That’s a high price to pay for sunshine and good wine. But it doesn’t need to be an A-versus-B choice.

For many investors, the choices they make with their investments are about getting from point A to point B, with point B being a comfortable retirement. There are many ways to invest and many investment options to choose from. But the impact of taxes needs to be considered. Taxes can have an outsized impact on savings, one that you may not notice until it’s too late. You can count on sunshine most days in California … but the rare times it rains can ruin a day at the beach. Taxes can have a much bigger and longer-lasting impact on your retirement savings. Let’s look at how much.

California state taxes – What you need to know

There are a couple of things you need to know about how the taxes of your state can impact your after-tax return.

- State income tax rates scale up at a faster pace than federal taxes. This means you could be in a higher state tax bracket at a much lower income than federal taxes.

- In California, capital gains aren’t given preferential treatment. Most investment income is taxed as ordinary income.

- State taxes are only deductible up to a maximum of $10,000 a year from your federal tax return. There is a very good chance that your real-estate taxes have used most of if not all the benefit, and you may have very little to no ability to deduct state income taxes from your federal taxes.

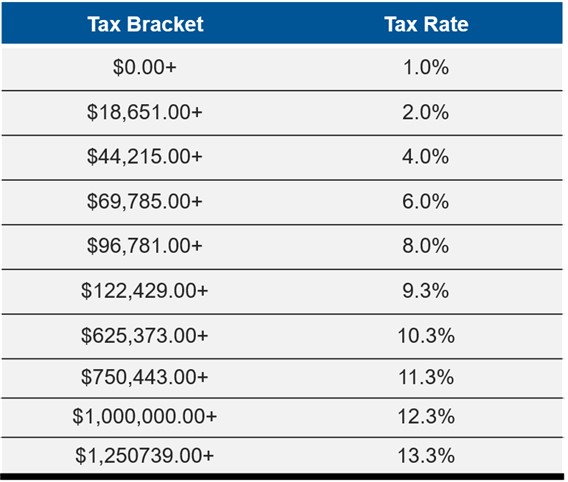

California: Married Filing Jointly

Notice how quickly one’s income level pushes a taxpayer into a relatively high tax rate?

Does California tax investment income?

What is causing these taxes? The short answer is: your income plus the distributions out of your investment holdings.

The long answer isn’t that much more complicated, but it is longer. While at the federal level tax-exempt bond interest is exempt from taxes, this is not the case when you get to state-level taxation. Only tax-exempt bonds from your specific state get the tax-exempt benefit when it comes to state income taxes. Additionally, while at the federal level qualified dividends and long-term capital gains receive preferential treatment with a lower tax rate, this isn’t true when it comes to California taxes. Outside of tax-exempt interest from California state and municipal tax-exempt bonds, all interest, dividends and realized capital gains are taxed as ordinary income.

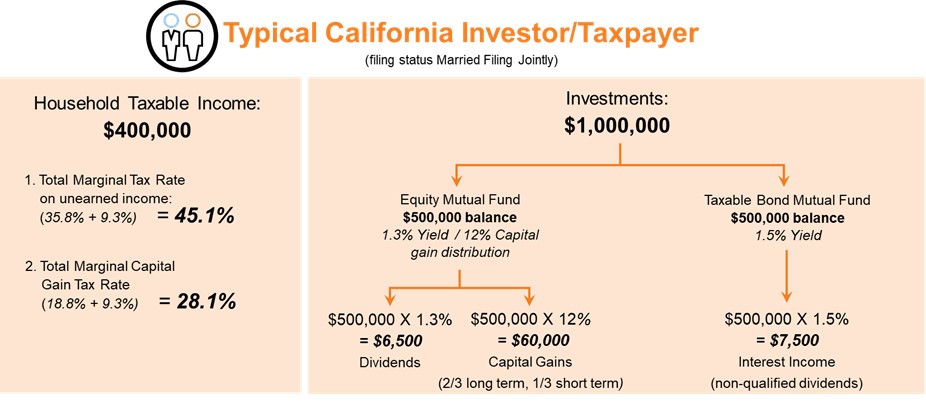

Let’s look at a specific albeit hypothetical scenario: a married couple filing jointly in the latter part of their working years with income of $400,000.Let’s assume that our fictional couple, Joe and Joan, have a portfolio with a value of $1 million, split evenly between stocks and bonds in order to keep the math somewhat simple. Using some averages from last year, we can hypothetically deduce how much income their portfolio created. You can also see what their marginal combined tax rates look like.

Click image to enlarge

For illustrative purposes only. Tax rates used at $400K income level for married filing jointly: 35% Federal income tax rate, 3.8% Net Investment Income Tax (NIIT), 15% capital gains rate, and 9.3% California State income tax rate.

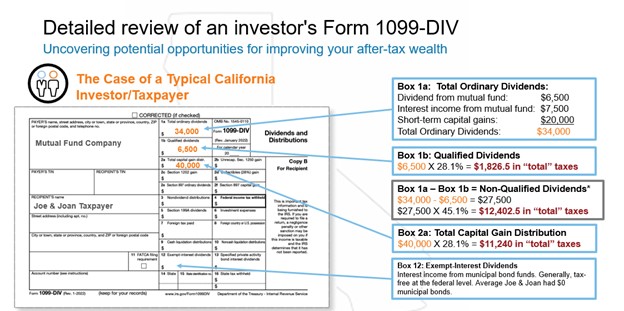

This information is great, but by itself it doesn’t mean much unless we make the math happen. From here we go to the Form 1099-DIV, which the Internal Revenue Service mails out to investors in February or March:

Click image to enlarge

For illustrative purposes only. Tax rates used at $400K income level for married filing jointly: 35% Federal income tax rate, 3.8% Net Investment Income Tax (NIIT), 15% capital gains rate, and 9.3% California State income tax rate. *Any non-qualified dividends are taxed as ordinary income at 35.8%.

This is what the 1099 DIV looks like for this hypothetical investment couple. To make sense of the picture, stay tuned. But while we are on the 1099-DIV, we added in some calculations on the right as well as listed out what the primary boxes are that need to be looked at further. This is a case where knowledge is power, but we also need a calculator.

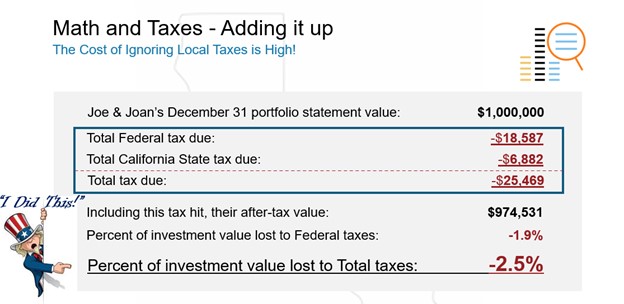

In the end though, what matters most is how much this is costing the investor. And, how much of the investment return is lost to tax drag (tax drag = tax cost; and tax cost is basically a hidden fee) (financial professional login required).

Click image to enlarge

For illustrative purposes only. Tax rates used at $400K income level for married filing jointly: 35% Federal income tax rate, 3.8% Net Investment Income Tax (NIIT), 15% capital gains rate, and 9.3% California State income tax rate.

Ouch. As if the cost of taxes at the federal level wasn’t enough.

In summary, at just the federal level on this 50/50 portfolio, almost 2% of return was lost to taxes. When you add in the tax drag created by state taxes, the impact increases to a full 2.5%. While federal taxes are still the biggest bite out of your return, the state tax impact is not negligible. A full half a percent lost to taxes is a big deal, especially when you consider the impact of that lost return compounding over the long term.

You better pay attention to state taxes, too!

Taxes are a cost. There are a lot of things in an investment portfolio that can trigger a tax bill to grow. While many investors primarily consider income as the source of their tax liability, interest, dividends, and capital gains are primary sources of tax drag on investment returns, especially when you pay both federal and state-specific taxes. This is why tax management is important at every level. The more that can be done to control the drag that taxes have on your investment return, the more likely you are to achieve your investment and retirement goals.