Separately Managed Accounts with Direct Indexing: A tax planning tool for baby boomers

Executive summary:

- As baby boomers enter their retirement years, many will be downsizing or selling a small business. Here's how advisors can help them manage these events without getting a hefty tax bill.

- Our innovative Personalized Managed Accounts program can be a useful tool for advisors to help their clients plan years in advance for these potential cash windfalls.

- By using Separately Managed Accounts with direct indexing, advisors can address three key issues: markets go up more often than they go down, tax-loss harvesting should be done all year, and investors don't like paying taxes.

"To plan, or NOT to plan, that is the question."

If I am honest, I don't remember much from my high school English classes, but I do remember a variation of that quote from William Shakespeare's play Hamlet. I share it with you because I think it has a lot to do with the state of financial advice in 2023. As I enter my 19th year at Russell Investments, here are a few life lessons I've learned along the way:

- Markets go up more often than they go down (73% of the time since 1926 if you're looking at the S&P500 Index) 1

- If you wait to tax-loss harvest until November and December, you're likely to miss many opportunities

- Investors don't like paying taxes to Uncle Sam

I know, these are not shocking revelations. But how does this connect to planning?

Well, many of the advisors we partner with have been working with their clients for MANY years and they know a lot about them and their situations. Knowing details about their clients' families, jobs, careers and potential future liquidity events helps in the planning process.

We've all heard the statistics about 10,000 baby boomers (born between 1946 and 1964) reach retirement age every day. According to Pew Research Center, baby boomers are retiring at a faster pace since COVID-19 began. Nearly 29 million Boomers retired in 2020— three million more than in 2019. By 2030, 75 million more Boomers are expected to retire.2

As this group leaves the workforce and looks to decumulate their portfolios, events like the ones listed below are going to increase:

- Selling a business

- Downsizing home/selling real estate

- Selling appreciated stock

- Exercising stock options

- Decumulating portfolio for income/systematic withdrawal

- Tax-efficient rebalancing or reallocating

The planning opportunity for advisors is that MOST of these liquidity events will be taxable in nature.

How does this connect to Russell Investments and my time here?

Russell Investments: A history of innovation

Russell Investments has been an innovator since our firm's founding in 1936.The most recent evolution at Russell Investments is the introduction of our Separately Managed Account (SMA) portfolios and, more specifically, Direct Index Separately Managed Accounts through the Personalized Managed Accounts (PMA) program. A Direct Index SMA allows investors to have passive market beta exposure in a separately managed account which holds a sampling of the individual securities that track the specified index and doing so while potentially generating tax assets.

How is this different from the commingled product options on the market (e.g., mutual funds and ETFs)? Well, let's look at returns for the last five years for a taxable account, bearing in mind that a 0% tax rate is always the best tax rate (remember life lesson #3 above). One of the techniques that investors and advisors have used to help maximize after-tax returns is tax-loss harvesting—i.e., creating a tax asset that can be used to offset gains in other areas of the portfolio. The matching of gains and losses allows more money to compound without the drag of owing taxes.

If you simply buy and hold an index fund or ETF, then you're only able to tax-loss harvest when the entire market that index fund or ETF represents is negative. If markets go up 73% of the time, then you're really limiting your ability to tax-loss harvest with these types of products.

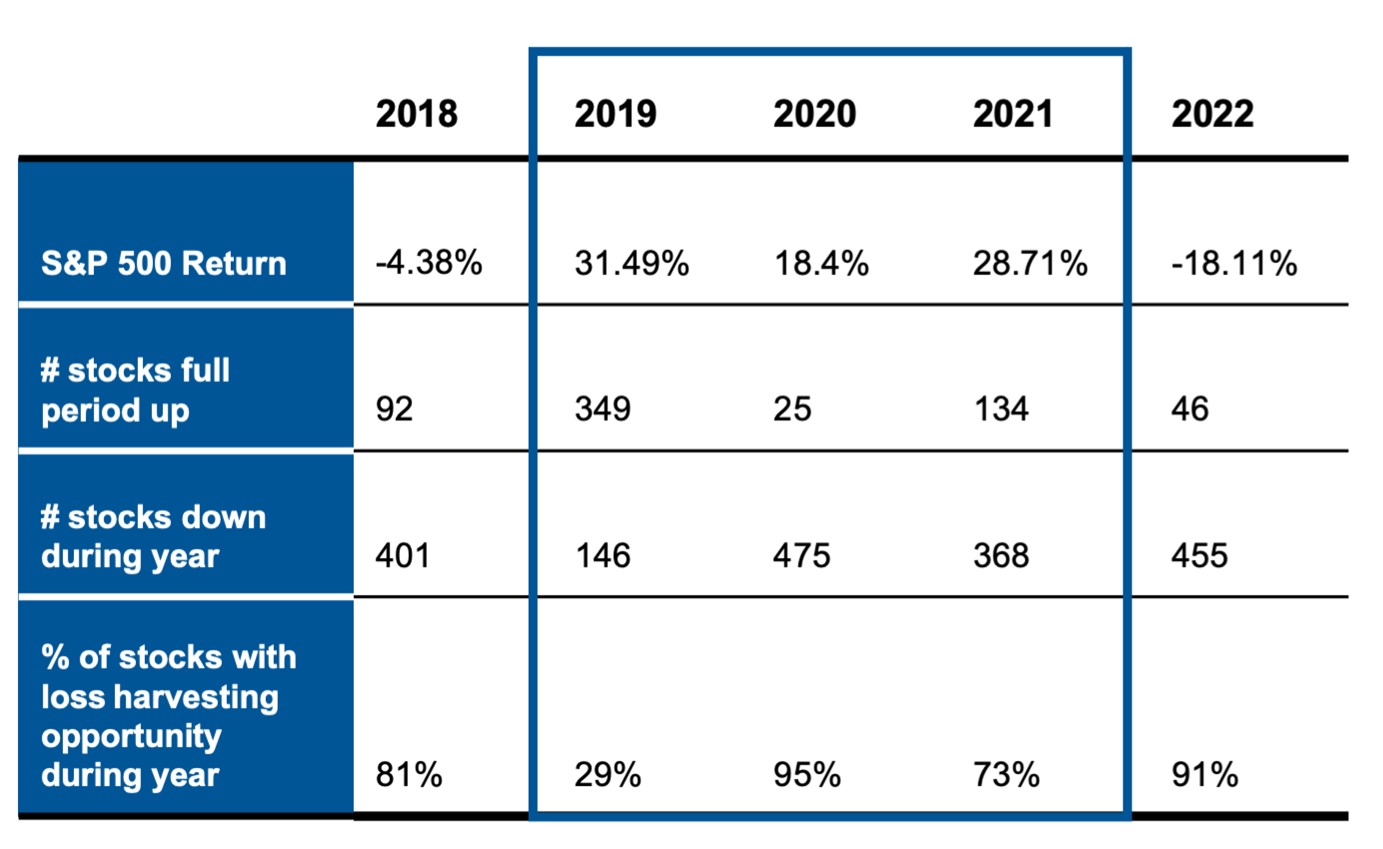

Look at the last five years as an example:

Analysis is based on S&P 500 as of 12/31/2022. "Full period up" indicates stocks that were never down YTD at the end of any month during the year. "Down during year" means stock was down YTD for at least one month during the year. Stocks that do not have full year returns were excluded. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

If you owned a commingled fund—and therefore, the entire S&P 500 Index—you would have been unable to tax-loss harvest in 2019, 2020 and 2021.But look at the number of individual securities within the entire index that were down at some point during those years: 146, 475 and 368 respectively. Those are tax-loss harvesting opportunities! If you owned the individual securities, as you do in a Direct Index SMA, you would have had numerous opportunities to tax-loss harvest. As the saying goes, this is like having your cake and eating it too. With a Direct Index SMA, an investor can potentially experience the return of the market while generating tax assets.

"To plan, or NOT to plan, that is the question"

Let's say you've been working with a client and their family for many years, and you know they will have a taxable financial windfall in the future.

Wouldn't it be nice to put a plan in place which allows that client to participate in the market for the five to 10 years in advance of the windfall and help the client simultaneously generate tax losses over time to offset that future windfall?

For instance, imagine a fully taxable event of $3 million dollars with nothing to offset that windfall from a tax perspective. That would result in a big check to Uncle Sam. And a frustrated client. And a missed business growth opportunity for you, too.

Imagine instead that same $3 million windfall but you planned for it and your client now has hundreds of thousands (or maybe millions) of dollars in realized losses to offset that windfall and the Direct Index SMA is delivering the market performance of the index it's designed to replicate.

That would be a massively different outcome for some of your best clients.

As we continue to innovate at Russell Investments, we believe our SMA portfolios help automate and systematize this process by addressing three challenges advisors and clients face:

- Markets go up more often than they go down (as of December 2022, 73% of the time since 1926 if you're looking at the S&P500 Index)

- If you wait to tax-loss harvest until November and December, you're likely to miss many opportunities

- Investors don't like paying taxes to Uncle Sam

Maybe William Shakespeare wasn't specifically writing about taxes when he wrote Hamlet 400+ years ago, but the sentiment is the same—it is better to plan than not to plan. Applying this to financial advising today, we believe thoughtful planning along with next-generation SMA portfolios can go a long way to help advisors and investors deliver better outcomes.