What should you look for in a direct indexing provider? 10 things to consider

Executive summary:

- A direct indexing solution can help make an investment portfolio as personalized as a home

- The provider of the direct indexing solution should be as key to finding the right product as the real estate agent is to finding the right home

- There are specific criteria that may help you select a direct indexing provider that is suitable for your clients

We've all heard the maxim about what to look for when buying a house: location, location, location!

But that's not all that's important, as you will realize if you have ever purchased a home or even watched an episode of House Hunters. When you start to peel back the layers of what you need in a home, it's far more than simply location. It's all about what you need (such as the number of bedrooms), what you want (garden? pool? two-car garage?), and must have (updated kitchen and bathroom, perhaps) when buying a home. Your home should be exactly what you want and need.

It's the same when investing for your client. Their portfolio should be as right for them as their house: what they're looking to achieve, how much risk they can take on, and the length of their time horizon. And for a lot of your clients, a traditional investment vehicle will be just fine.

However, some of your clients may need something more personal. Their situations often come with complexity and uniqueness that differ from the typical client. Or maybe their portfolio has been refined to a certain set of criteria they have to abide by because of their strong beliefs or corporate mandates. Whatever the reason, a common solution to these issues is direct indexing.

In the simplest terms, direct indexing involves directly investing in a subset of the actual securities that make up an index. As my colleague Brad Jung recently wrote, this innovative investment strategy allows you to choose individual stocks, diversify your clients' portfolios, and potentially reduce their tax liabilities. It can be built for investors who want their portfolio to reflect their environmental stance, religious beliefs, or values.

When buying a house, your real estate agent is key. They need to know your preferences and budget and other considerations so they can show you targeted properties that meet your requirements. You would choose your agent carefully because you are going to trust them to have your best interests at heart and ensure you are happy with the home you buy. The provider of your direct indexing solution should be selected with similar criteria in mind. What should you look for when comparing one direct indexing provider to another?

Here are 10 criteria we believe advisors should consider when shopping for a provider.

- Tax Management experience.

One of the primary benefits of direct indexing is the potential for tax optimization through strategies such as tax-loss harvesting and capital gains management. In the same way you wouldn't hire a plumber to fix an electrical issue or vice versa, we believe you should assess the provider's expertise in tax-managed investing and their ability to implement strategies that can help minimize tax liabilities. - Track record and expertise.

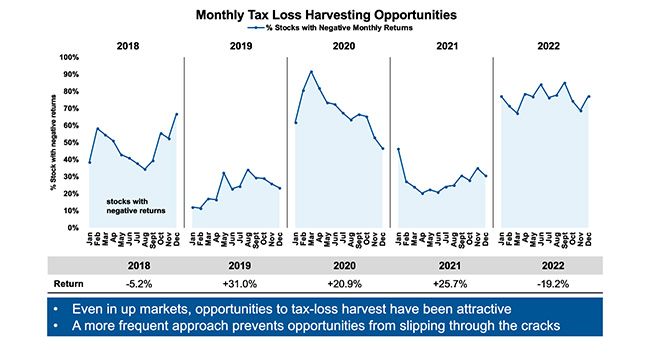

Consider the provider's experience in managing indexed portfolios, the performance of their strategies over time, and their understanding of tax-management techniques. For example, many providers only do tax-loss harvesting quarterly. While that's better than not doing it at all, providers who only tax-loss harvest four times a year may be missing out on numerous opportunities.

Click image to enlarge

Source: Morningstar Direct. Stocks: Russell 3000 Index constituents based on beginning of the year weights. Returns are year-to-date using year end index weights.

- Flexibility.

If your client has other investment accounts or holdings, consider whether the provider can integrate with them effectively. For example, how much of a concentrated stock position can the provider take on? Some providers only have the ability to manage a small portion of a concentrated stock position. What is the benefit of leveraging an investment if the provider can only use it for portion of what your client needs it to do? Working with a provider to take on any concentrated stock position, regardless of size or percentage of the overall portfolio, creates simplicity for you. - Transition management.

Consider the level of support provided to efficiently transition your client's portfolio to the new direct indexing solution. Does the provider run a transition analysis that gives your clients a structured and well-developed plan to reposition a portfolio? This can be a powerful tool to help clients understand how to migrate a concentrated or unmanaged portfolio while managing the related tax burden. - Account minimums.

When you look at direct indexing offerings today, consider the account minimums. Although direct indexing was built for the high net worth (HNW) client, it can also be attractive to a larger group of investors. Many providers using a purely passive approach require higher minimums. An active manager typically has fewer holdings than passive managers, meaning their minimums are often lower, which makes them more accessible to a larger portion of your clientele. - Research and investment methodology.

Understand the provider's research and investment approach and look for transparency regarding their investment methodology, the factors they consider when constructing portfolios and their approach to risk management. A sound investment philosophy and disciplined approach to portfolio construction are essential. - Customization options.

Direct indexing allows for more customization options compared to traditional mutual funds or ETFs. Look for a provider that offers a wide range of customization options such as the ability to exclude specific stocks or sectors, implement tax optimization strategies and align the portfolio with a client's values, preferences, or beliefs. - Passive? Active? Or both?

Whether you're a diehard believer in purely passive management or an advocate for active management, most likely your clients won't be all one or the other—they'll probably see value in offering them choice. They may want a blend of the two approaches. Limiting yourself to one approach over another is almost like flipping a coin to see which one will do better this year! Finding a provider that offers you a selection of completely passive, completely active or the ability to combine benchmarks, is critical in providing the appropriate choices to your clients. Active management and direct indexing each have their own benefits and can complement each other. Having both also gives you optionality for different client needs. - Cost structure.

Direct indexing typically involves separately managed accounts, and the fees associated with these services can vary. Understand the provider's fee structure, including management fees, overlay costs, and any additional charges. Compare the costs across different providers to ensure they align with your client's goals and budget. - Industry recognition.

When you hire a writer to help you write a book, you may select an individual that has ghostwritten for a best-selling book. You may look for name recognition and you may prefer one who has been in the business for a while. All of those factors could help provide a sense of comfort that the writer has been successful in helping other individuals write a book.

You should have the same level of comfort with your direct indexing provider. One that has longer tenure is likely to have more experience with the intricacies of the product than a new entrant. A provider that is an established firm with name recognition will likely have more staying power than a smaller, independent firm, at least regarding this innovative and complex solution.

You may also find a greater level of comfort with a writer who has gained recognition from their peers in the industry. In turn you may also prefer a direct indexing provider that has received peer recognition for their program.

The bottom line

In summary, no two houses are the same and your forever home should be personalized to your liking. In that regard, many direct indexing offerings today are fairly similar. It's not until you begin to look under the hood that you start to uncover the small differences in their process that ultimately lead to a very personalized experience for your client. The best place to start is by simply understanding each asset manager's background in tax management to truly assess if they have a tried-and-true process in place.