Managing frozen pensions: 3 considerations for plan sponsors

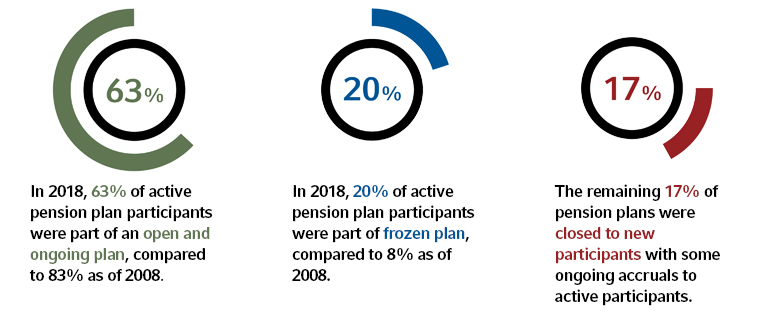

The trend toward frozen defined-benefit (DB) plans continues across corporate America, with approximately 25% of pension plans now having completely halted—or frozen—benefit accruals for participants. The latest data shows that this trend has accelerated in recent years, as shown by the graphic below, with only 63% of DB plan participants in 2018 enrolled in an open and ongoing plan—compared to 83% in 2008. In addition, several large companies have recently announced that they will be freezing their plans in the upcoming years, including General Electric, the United Parcel Service and General Mills.

The trend toward plan closure

For plan sponsors considering whether or not to partake in this trend, it’s important to understand the management of a frozen plan differs considerably from the management of an open plan. This is because a plan that is frozen is on a path to eventual termination. As such, there are major implications to consider when it comes to funding policy, investment policy and risk transfer—all of which can be exacerbated by the current low-rate environment. Here are some key insights on each, which our recently updated frozen plan handbook explores in greater detail.

1. Funding policy

Funding policy concerns the choice of how much money to put into a pension plan today to cover the benefits that will be due to participants in the future. For an open pension plan, there is likely to be an ongoing stream of new contributions to accompany new benefit accruals, so those contributions can be adjusted up or down in response to the investment experience. In a frozen plan, however, there are no new accruals, meaning that there's no incentive to contribute (beyond meeting minimum required contributions).

In the event of a better-than-expected investment experience, a frozen plan may find itself with what's known as trapped capital—assets that are not needed to meet the obligations of a full plan termination. Conversely, in the event of a worse-than-expected experience, there is less scope for a frozen plan to smooth additional contribution requirements. This makes the impact of variations in costs more visible to the sponsor—and the sponsor will generally need to respond more quickly than with an ongoing plan, due to the frozen plan's shorter time horizon. For these reasons, funding decisions are normally less flexible for frozen plans.

2. Investment policy

Frozen plans are special in that they are working toward a specific endgame, represent a marked-to-market challenge, have an evolving liability profile and are characterized by an asymmetry in the payoff for investment returns. Each of these features has implications for the plan's investment strategy.

The case for liability-driven investing is particularly strong for frozen plans—and for liability hedging in particular. Because a frozen plan's future cash flows are better known than an open plan (since there are no benefit accruals), and the duration of the liabilities is generally shorter, a more precise liability hedge is possible.

It is common for frozen plans to adopt glide path policies. These policies are based on the rationale that investment risk is worth taking for an underfunded plan, but less so as the plan approaches a fully funded position. A glide path policy works in conjunction with a typical funding policy to define a clear path from an underfunded starting point to eventual full funding, at which time investment policy will be substantially different.

3. Risk transfer

It is also possible to transfer risk out of a frozen plan altogether by transferring a liability (and an asset associated with that liability) to another party. One party that risk can be transferred to is the plan participant. The most common form of risk transfer is through offering to cash out the accrued benefits of terminated vested plan participants (i.e., those who have left the company but have not yet started to draw their pension benefits) by paying them a lump sum.

The other main party that risk can be transferred to is an insurance company. This is most commonly done through the purchase of annuity contracts, sometimes referred to as a buy-out. In this case, the liability of the plan is removed through the purchase of the contract, with the plan participants receiving their pension payments from the insurance company.

Other key considerations

Since the original edition of our frozen plan handbook was first published in 2013, Congress has passed additional funding relief, with the most recent version coming with ARPA earlier this year. The effects of funding relief have been substantial, with the drastic reduction in contribution requirements incentivizing sponsors to delay full funding. However, sponsors of frozen plans must also contend with significant PBGC premiums, which penalize underfunded plans and continue to increase each year.

Our updated edition addresses the latest trends in PBGC premiums, delves into the growth of the annuity market and unpacks the concept of plan hibernation—all while maintaining the core material from previous versions. To request a copy of this simple, illustrative guide to the investment and management of frozen pension plans, just click here.