$20 billion club report: Members slow to commit to 2021 contributions

For the largest U.S. listed DB plan sponsors – $20 billion club members – the year 2020 ended much as it began. On average, funded ratio increased slightly from 84.9% to 86.2%, the highest level in eight years. We document this in detail here. Unseen in these figures is the wild ride that was 2020. We saw the most volatile period in recent memory in equity values, interest rates and spread levels. Discount rates dropped, but equities compensated. And some sponsors even made large discretionary contributions.

In fact, employer contributions in 2020 exceeded expectations by about 60%. Asset returns were impressive, as these sponsors' equity and long duration fixed income allocations both performed well. But what is the outlook for 2021 and beyond? While we don't know with certainty, we do have a few clues as to what sponsors plan for 2021. Listed companies are required to disclose their estimated contributions for the upcoming year. Even though they are not bound to this estimate, over the last several years this has proved to be a reasonable approximation for contributions to come.

So, what do 2021 contributions look like? Historically small.

While many sponsors within this group have chosen to take contribution holidays in the U.S. at times due to favorable funding relief, in a given year we always see a few sponsors commit to make some form of discretionary contributions. In 2020, GE, Boeing and UPS all made multi-billion-dollar contributions, far beyond requirements. In 2018, Lockheed Martin, FedEx and Raytheon all made large payments to their U.S. DB plans. The year 2021 is different. Not even one of these 19 companies has explicitly committed to discretionary contributions. This has not happened in recent memory, certainly not since MAP-21 funding relief was passed in 2012. See Figure 1 below:

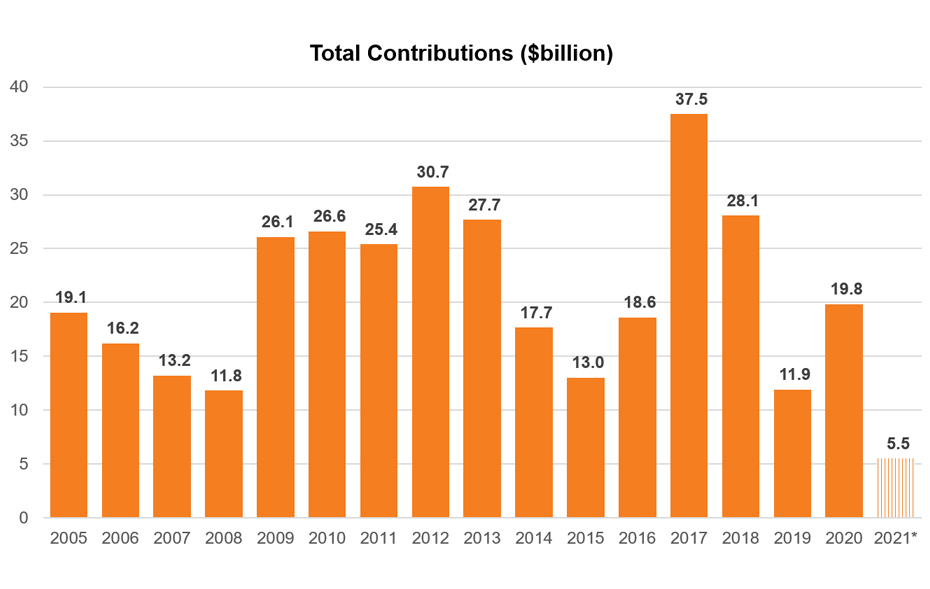

Figure 1

(Click image to enlarge)

Figure 1: Total $20 billion club contributions.

2021 is estimated as disclosed in 10-k filings.

The $5.5 billion in expected contributions in 2021 would be less than half the lowest we have seen in the last 16 years.

What exactly is driving these low expectations? A few key factors come into play.

Ongoing pension funding relief

As we have blogged before, the effects of funding relief first passed in 2012 have been far-reaching, dramatically reducing requirements and providing sponsors little incentive to immediately fund their plans (aside from a massive increase in PBGC premiums that were analyzed here). A funding policy of just paying the requirements hasn't proven to be an effective strategy for becoming fully funded, and most sponsors within the $20 billion club have voluntarily chosen to make periodic discretionary contributions to boost their funded position.

In 2021, a further extension and expansion of funding relief is possible, which would push funding requirements even further down the road.

Economic uncertainty

The COVID-19 pandemic has affected every company to some degree, and these large corporate sponsors have been no exception. A few of these sponsors (e.g., Pfizer, Johnson & Johnson) will be instrumental in ending the pandemic. Some (e.g., Boeing, Lockheed Martin) were hurt by decreased demand for their products. Others (e.g., UPS, FedEx) benefitted from increased consumer use of their services. But no one knows what 2021 will bring with varying degrees of government lockdowns, unpredictable consumer spending habits and emerging virus variants.

With this uncertainty, sponsoring companies recognize holding back on pension contributions is a lever they want to be able to pull.

Corporate tax rates on the rise?

The tax deduction available to sponsors for their pension contribution took a hit a few years ago when tax reform lowered the corporate tax rate down to 21%. Many companies within this group took advantage of the upcoming drop in tax rates by contributing massive amounts in 2017 and 2018 (see Figure 1 above).

President Biden intends to increase the corporate tax rate, not quite to former levels, but up to 28%. The prospect of this occurring could give sponsors an incentive to delay discretionary contributions until legislation is passed, thus offsetting part of the additional tax burden.

Final thoughts

Circumstances can change, and it would be reasonable to assume at least a few of these sponsors will still choose to make large contributions in 2021, particularly as we see how the economy looks post-pandemic. Sponsors of underfunded plans still face significant PBGC premiums, with rates increasing every year. Discretionary contributions promote progress on de-risking glidepaths and help sponsors avoid a funded ratio drop after risk transfer transactions.

2021 still carries much of the uncertainty we felt in 2020, and we will continue tracking the actions of the $20 billion club members to understand the broader corporate DB universe.