Are Separately Managed Accounts the "fan favorite" when it comes to personalized investing?

We all have our fan favorites. We root for our favorite football teams, favorite players, favorite mascots and even prefer a certain type of tailgate food, beverage, and activity.

Tailgates are an example of something you can easily cater to. You can BBQ, bring sandwiches, enjoy some pizza or wings. Simply put: You have choices.

When it comes to investing in commingled products, however, investors don't always have that level of control. Yes, they can tilt their asset allocation towards funds that hold emerging market stocks, or small cap, or infrastructure-related names if they want. And they can choose the provider of those funds.

But if one of your clients wanted to avoid a specific company or sector or type of stock, then what do you do? For high net-worth clients, you could build an individualized portfolio based on their preferences. However, that might not be feasible for some of your clients. Unless, of course, you utilize a Separately Managed Account (SMA).

As my colleague Kevin Knowles wrote recently, SMAs allow the investor to directly own the portfolio's securities, which in turn allows for client-level customization. This is different from a mutual fund or Exchange-Traded Fund (ETF), which offer investors what I call "the same experience." That is, all investors in the commingled fund hold the same stocks, receive the same performance and receive the same distributions. There are a lot of benefits to a “pooled" structure like a mutual fund or ETF, but some investors need a more specific experience and additional customization.

What is the benefit of client-level customization?

Let's look at a real-life example.

Say one of your clients purchased ABC Fund 15 years ago while another of your clients purchased the same fund last year. Now let's say the fund has held Netflix for 10 years and bought in at $7 a share. The managers of ABC Fund decided to sell Netflix last year at $250 a share. Since Client A already held the fund, they benefited from the stock's rise. But Client B bought in to the mutual fund when Netflix was trading at $500 a share, so they didn't.

Still, since ABC Fund is a commingled fund, both of your clients would receive the same capital gains distribution. And both would be taxed on that distribution. Client A has at least received the benefit of the increase in the fund's Net Asset Value (NAV). But Client B? They didn't get any of the good experience, just the bad. How fair is that?

Now let's look at the same scenario but have your clients invest through a SMA instead of a mutual fund. Like ABC Fund, they hold large-cap names that are members of the S&P 500 Index. And let's say both your clients hold Netflix and purchased it at the same prices noted above. Now they can individually decide when to sell Netflix and at what price. For the purposes of this argument, both sell at $250 a share. Because they hold SMAs instead of mutual funds, they can decide how to use the capital gain or loss that ensues. Client A has capital losses elsewhere in their portfolio that they can use to offset the capital gain they receive from selling their Netflix shares. Meanwhile, Client B takes the capital loss from selling their Netflix shares and uses it to offset capital gains elsewhere in their portfolio. In the end, both clients minimize the capital gains distributions they receive and in turn minimize the associated taxes.

Of course, either of your clients could have decided not to sell at $250 a share, or only sell a portion of their Netflix stock, or even buy more.

How do SMAs help personalize a portfolio?

Let's continue with the tailgate example. Say you have a client who wants to avoid a certain stock or sector for whatever reason, in the way I might want to avoid mayonnaise on my sandwiches when I tailgate (or at any time!). To make sure there is no mayonnaise on my sandwiches, I make them myself. This is essentially how an SMA works. The investor can personalize their portfolio to fit their needs and preferences.

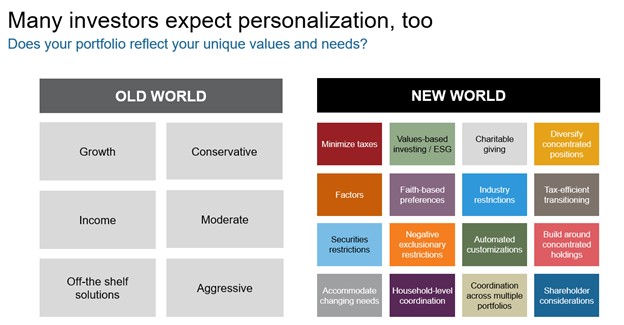

Here's a list of some of the different ways you can use a Separately Managed Account to meet your clients' customization requirements.

Values-based exclusions

Maybe you have a client who wants to embrace a “preference screen" such as environmental, social and governance (ESG) criteria or socially responsible investing (SRI). Or they may want to restrict a single security. As Kevin noted in his blog, one advisor used a SMA for a client who wanted no exposure to oil and gas companies because of her commitment to environmental causes. Other clients may want to avoid names associated with warfare or human rights violations or extractive mining.

Restricting a whole industry

Some of your clients may want to restrict their exposure to a specific industry for other reasons. Let's imagine one of your clients is an executive at a large insurance company. Since a lot of their personal wealth is already tied up with the insurance industry (their employment income, stock options, pension and so on), they may want to reduce their exposure to other insurance companies. Or they may be required to do so to avoid a conflict of interest.

Diversifying a concentrated stock position

Many executives or long-term employees are granted stock positions from their employers, either received as stock options or grants over the course of multiple years. Often these positions will have a low cost-basis and represent a fairly large percentage of their overall portfolio. A SMA that incorporates Direct Indexing can be an efficient and tax-smart way of reducing that concentrated stock position, which can reduce the single-stock risk those clients have.

Tax Management

No one wants to pay more taxes than they have to, right? As described earlier, this may be the biggest advantage of an SMA. SMAs can help investors manage their capital gain distributions and reduce taxes on their portfolios. Since the investor owns the actual securities, the manager of the SMA can tactically use tax-loss harvesting techniques to offset gains elsewhere in the account or in another part of the household's portfolio. Additionally, the timing of any tax-loss or tax-gain harvesting would be done when it's most beneficial for the investor.

Click image to enlarge

What is an example of client-level customization?

Our team recently worked with an advisor in Texas, whose client is retiring from a long career in the aerospace and defense industry. This investor had a variety of accounts, including a Roth and an Employee Stock Ownership Plan. More than $600,000 of his $1 million portfolio was invested in his company's stock. At this stage of his life, he and his advisor agreed that single-stock risk was too high. Yet, selling the shares he had accumulated over his 40-year career would create substantial capital gains. What to do?

A SMA solved the problem: the investor would sell most of his company holdings over five years. That would not only spread out the capital gains and the accompanying taxes over the specified period but would also allow the investor to use any tax losses to offset the gains, which could potentially reduce the tax bill to zero. This investor could have chosen another approach to transition his portfolio: rather than select to sell his company holdings over a specific number of years, he could have determined the amount of taxes he was willing to pay annually and then sell off the holdings at whatever rate would meet that budget.

A side benefit of using a SMA for this problem? The advisor is now working with several other former employees at the same company – talk about the power of referrals!

The bottom line

Separately Managed Accounts allow investors to have choices. Are they a fan of a company brand, or want to support manufacturers of plant-based products? They can select those names for their portfolio. Do they want to avoid companies that manufacture tobacco? That's easy with a SMA. Do they only want to pay a certain amount of capital gains taxes a year? Done. Do they want to defer capital gains taxes to a later date when their other sources of income may be lower? Done.

In short, a SMA allows investors to choose a portfolio that aligns to their values or specific needs. This is like designing your perfect sandwich for your tailgate party. Investors can select the individual securities they want to hold and exclude those they don't want to hold. They can manage their personal tax liabilities. They get full transparency into their holdings. They can adjust their portfolio if their requirements change. In short, they can have a portfolio that speaks directly to their goals, circumstances and preferences.