The UK won’t Brexit on Oct. 31, but no-deal risks have collapsed

What happened in Brexit this month?

While the Brexit process seemed to have arrived at a dead-end in early October, a meeting between the UK and Irish prime ministers, Boris Johnson and Leo Varadkar, on Oct. 10 gave it new momentum and paved the way to an agreement that was acceptable to both sides.

At the European Council summit on Oct. 17-18, the UK settled on a modified withdrawal agreement with the European Union (EU). The new agreement removes the controversial backstop that could have retained the entire UK in a customs union with the EU after the end of the transition period. However, to ensure there is no physical border infrastructure and no customs checks between the Republic of Ireland and Northern Ireland, the new agreement keeps Northern Ireland in a de-facto customs union and in regulatory alignment with the EU on goods.

On Oct. 19, the UK House of Commons passed the second reading of Withdrawal Agreement Bill (WAB) with a majority of 329 to 299 votes, which shows support for Brexit in principle and allows the bill to proceed to parliamentary debate and a decisive third reading vote.

Shortly afterwards, however, Parliament rejected the timetable set by the government (the so-called programme motion) to complete the debate in three days. The Democratic Unionist Party (DUP), who currently prop up the Conservative government, voted against the WAB and the programme motion because they believe the new deal could create divergences between Northern Ireland and the other nations of the UK.

The failure of the business motion to pass made it virtually impossible for the legislation to complete all necessary stages before the Oct. 31 Brexit deadline. Also, the “Benn Act” compelled the prime minister to request a Brexit extension from the EU if no withdrawal bill had passed by Oct. 19. Boris Johnson (reluctantly) sent an extension request letter that same evening.

On Oct. 28, the EU signed off on a Brexit flextension, an extension to Jan. 31, 2020 with an option for the UK to leave earlier if a deal is ratified.

With a Halloween no-deal now off the table, the House of Commons passed a bill to hold general elections on Dec. 12.

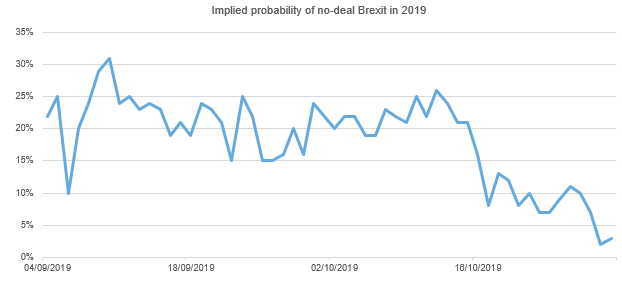

We agree with the political betting markets that the political gyrations have significantly lowered the risk of a no-deal Brexit in 2019 (see Figure 1).

Figure 1: Political betting markets think that the risk of disorderly Brexit has collapsed…

Source: predictit.org, as of 29 October 2019.

What could happen now? Short-term political paths to the end-state

- Conservative majority: Brexit by Jan. 31, 2020 (40%)

- Hung parliament: Deal, no-deal and referendum all in play again (40%)

- General election with a shift towards remain parties, a second referendum (10%)

- Other scenarios (10%)

- Sterling: Significantly up (10-15%) as UK’s currently favorable trade terms are secured for the future.

- Large-cap UK equities: Slighty positive, with the unwinding of the Brexit discount offset by heavy reliance on foreign earnings, which will be depressing by currency appreciation.

- Domestically focused equities: Should outperform large-cap UK equities and the FTSE 100.

- Gilts (10-year): Meaningfully down as yields rise (30-40 basis points) to accommodate a higher expected short rate path and a higher neutral rate.

- Sterling: Up (~5%) on relief that a Brexit deal that includes a transition has been reached. However, the gains are tempered by the fact that another cliff-edge still exists down the road.

- Large-cap UK equities: Flat or down slightly due to the negative correlation between sterling and large-cap equities.

- Domestically focused equities: A positive response as the UK’s economic outlook brightens somewhat.

- Gilts (10y): Down as yields rise (20-30 basis points) as some negative risk premia is removed from the curve.

- Sterling: Down (15-20%) as the UK is economically locked out of all of its main trading partners as it falls back to WTO terms.

- Large-cap UK equities: Up due to the negative correlation between sterling and large=cap equities, although this will be partly offset by no-deal Brexit induced recession fears and uncertainty about medium term economic growth prospects.

- Domestically focused equities: Negative response as the domestic UK economic outlook materially darkens.

- Gilts (10-year): Significantly up as yields fall (20-30 basis points) to new lows on safe-haven demand and much reduced short-rate expectations.

As has been the case with the Brexit process all along, the three major outcomes are Brexit with deal, no-deal Brexit and remain. However, there are many potential short-term political paths to these three outcomes. We outline these below with our subjective probabilities in brackets.

If the general election delivers a stable majority for the Conservative party, it is likely that the WAB passes as it is and the UK leaves by 31 January 2020.

A hung parliament is a quite likely outcome, in which case we are back in the same situation as today. However, the EU could be more reluctant to agree on an extension, increasing the pressure to pass the deal, but a second referendum and even a no-deal could also come back into play. A further extension cannot be ruled out.

If the remain-leaning parties win more seats than the Brexit-supporting parties, a second referendum is likely (possibly attached to passage of the WAB).

Although we try our best, it is not possible to exhaustively cover all possible scenarios.

End-state Brexit outcomes and market implications

As a result of the short-term political paths outlined above, we also refreshed our end-state Brexit probabilities (previous probabilities are from end-August 2019) and calibrated the associated market movements*:

Remain (down from 25% to 20%)

Deal Brexit (up from 40% to 70%)

No-deal Brexit (down from 35% to 10%)

Bottom line

A modified withdrawal agreement between the UK and the EU was thrashed out this month. However, the ratification of the agreement has hit severe roadblocks in UK parliament, delaying Brexit beyond Halloween. To break the logjam in the House of Commons, an election has been called for Dec. 12 Although the Conservative Party holds a lead in polls of voting intentions, the outcome of the election and its implications for Brexit are still highly uncertain. Stay tuned.* Direction and magnitude of expected market reaction is based on experience from the post-referendum (after June 23, 2016) period. The anticipated market reactions will not necessarily occur on the exit date (whether Jan. 31, 2020, earlier or later). They may occur suddenly in the run-up to the exit, if unexpected but clear political outcomes materialize. Alternatively, market moves may play out gradually over an extended period of time, if the political process evolves towards the outcome slowly. Market moves calibrated using Oct. 23, 2019, closing prices.