Does overlay make sense for your investment program? The answer likely depends on several factors: your type of plan, size and frequency of cash flows, funded ratio relative to liabilities, and any other challenges that might be unique to your situation. By large pension plans, we mean those that are of large enough scale to hire investment managers via separate account implementation. With such a custody relationship in place, an overlay can be added at a very small incremental cost which can be readily recouped via several key benefits.

Overlay means many things in the investment industry. In this case, we're talking about the use of futures, such that cash exposure—wherever it sits—can be covered by other risk premia—generally equity index or Treasury exposure.

Here are a few common overlay uses, in greater detail:

Rebalancing or maintaining asset allocation

With an overlay in place, funding of benefit payments and other cash outflows do not require a just-in-time sale—or purchase in case of inflows—of sub-advised assets. In such an arrangement, greater cash balances can be maintained in a liquidity reserve account in custody, but they do not need to result in cash drag relative to the investment policy. The example below shows a case where both long and short futures are allowed to make rebalancing more efficient. This is particularly attractive for plans that have higher allocation to illiquid or private assets, which are less able to absorb rebalancing flows and generate more cash flows due to capital calls and distributions. Less liquid asset classes—or in some cases even private asset classes—can be proxied with more liquid futures contracts on a public asset class.

In addition to correcting for ongoing allocation drift, the overlay is a great tool in coordinating transient events like manager changes or asset allocation shifts. Transition management and overlay activities can be coordinated by the same provider to make coordinated shifts that do not allow periods of problematic exposures to develop over critical hours and days. A risk-controlled project minimizes the chance of a large negative opportunity cost from detracting from plan performance.

REBALANCING OVERLAY

Uses long and short futures positions to specific asset classes to also implement rebalancing policy

Hedging or accessing interest-rate risk

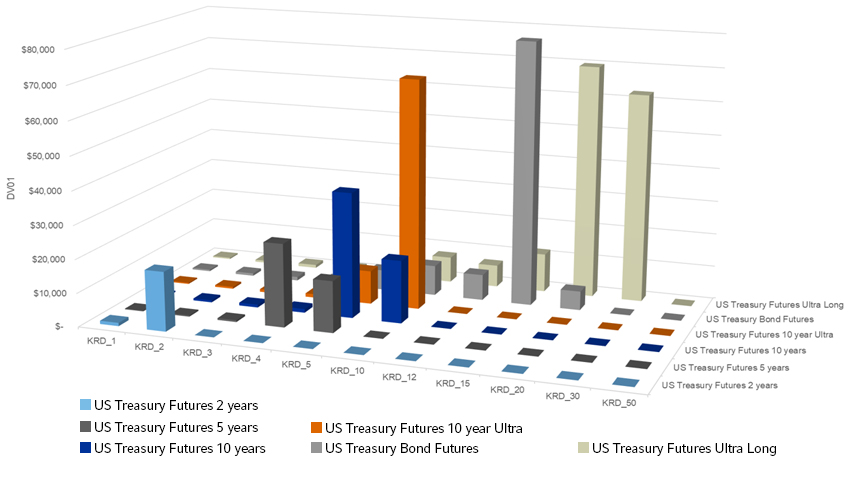

The US Treasury futures complex provides numerous points of exposure to the US yield curve. As a result, listed Treasury futures are a versatile tool for interest rate hedging needs of pension plans of all types. The graph below shows the Key Rate Duration (KRD) contributions from the available US Treasury futures:

KEY RATE DURATION EXPOSURE $100mm NOTIONAL VALUE PER CONTRACT

Click image to enlarge

Below, you will find two specific use cases: the first for corporate defined benefit and the second for public defined benefit.

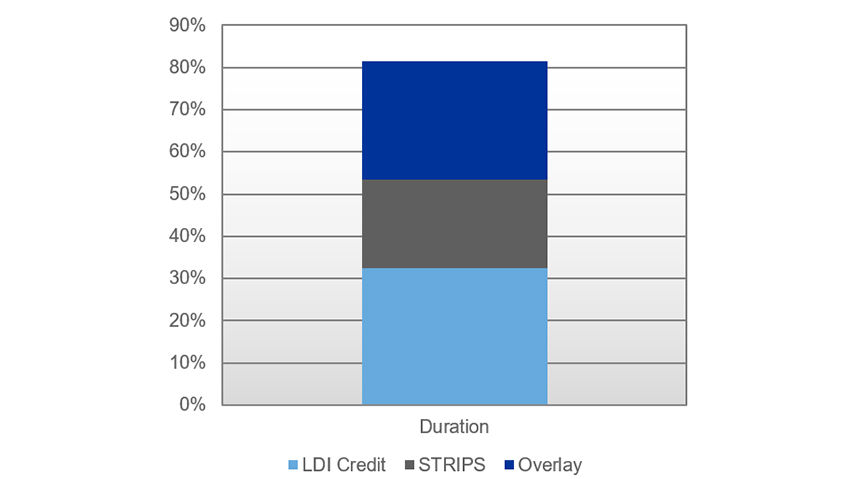

The corporate DB case – Long duration Treasury exposure to manage surplus risk relative to the liability with a Liability Driven Investment (LDI) program. An LDI completion overlay can achieve additional duration extension via Treasury futures or interest rate swaps, as well as fine-tuning yield curve exposure of fixed income managers typically managing to broad benchmarks. Duration extension via overlay comes into play when the existing LDI components need a bit more capital efficiency to reach the desired LDI Hedge Ratio. This generally occurs in cases where the value of the liability is greater than the value of the Fund's assets. In this case, the fund can maintain its desired growth asset exposure to close the funding gap while more effectively managing the downside risk to funded status in falling interest rate environments. Precision in LDI hedges becomes more important as closed or frozen plans become increasingly better funded. The most challenging KRD buckets to hedge with futures are 12 and 30+ years, where interest rate swaps could be utilized where greater precision is required.

LDI COMPLETION OVERLAY

Various long Treasury futures used to manage LDI hedge and improve capital efficiency

LDI HEDGE RATIO

The public DB case – In some instances, we have seen these clients seek a very liquid diversifying exposure to risk assets in the form of Treasury futures. Longer duration Treasuries have traditionally been the diversifier of choice with a tendency offset equity market risk in the event of a deeper economic slowdown. As the market currently stands in Fall 2022, 2-year through 7-year exposures currently carry higher yields and less duration risk to rising rates than longer exposures as we get further into the Fed hiking cycle. From a return-only consideration, these may be preferred by some public DB funds that do not engage in surplus risk views on interest rate exposures. An overlay gives the flexibility to hedge duration from physical fixed income mandates or otherwise adjust it with available Treasury futures.

Liquidity management

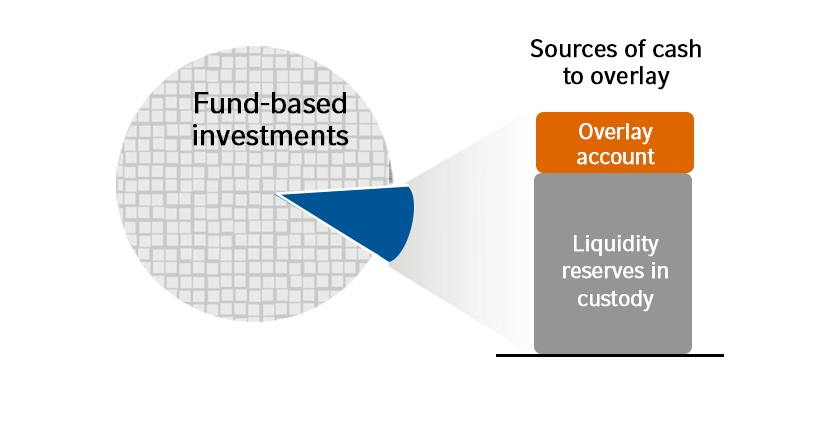

Maintaining larger cash balances in the payment account is then possible without having the cash drag of being uninvested. Periodic coordination to liquidate physical manager holdings with overlay positions can allow for recharging plan cash levels. This can reduce liquidation costs required to fund benefit payments (or other cash outflows) by using futures. In today's volatile environment with dramatic USD strength and a general shortage of quality collateral, an overlay allows for holding a larger liquidity reserve without having to bear investment exposure to cash. In many cases, the economics of a separate account for Treasury Bills or other collateral pool managed by Russell Investments Fixed Income team can be compelling and allow for improved pledge coordination to back overlay activity.

Tactical flexibility

While most pension portfolios track a policy portfolio with varying degrees of range tolerance from a target, it's often the result of relative market returns, causing exposures to drift from target levels. A tactical overlay can make exposures more deliberate and target additional return generation from top-down. Russell Investments offers a service called Enhanced Asset Allocation (EAA), such that the discretion to make risk-controlled asset allocation tilts resides with us. This means the tilt does not require the client's governing-body approval to open or close positions. From our experience, traditional governance approval takes too long to allow for efficient return capture, which means most plans do not tactically tilt on their own. For those that do, the overlay platform is a great way to implement such tilts in an effective manner, as well as isolating and measuring the impact of those decisions.

Not every DB pension fund needs an overlay

While larger institutional clients that are already administered via separate accounts have a lower cost/benefit hurdle for adding an overlay program, it may be challenging for some DB clients to make a compelling business case for such a move. Here are some examples where the decision may not pencil:

- Desire for momentum from drift relative to policy. While we occasionally talk to investors with such a view, it is generally case that loose rebalancing ranges are better than no disciplined rebalancing. Russell Investments overlay team can have standing orders to automatically rebalance back into range, or in other cases the client retains the authorization to trigger a rebalance with futures.

- No need for LDI program to manage surplus volatility. Since this is the most obvious case where an overlay can offer benefits, client-types that don’t manage risk in this way may be less prone to add the complexity of an overlay, especially if their fund-based program is already functioning well.

- Clients with low-risk allocations already may have little need for increased capital efficiency an overlay can deliver. We sometimes refer to these as hibernating plans that are gradually increasing funded status with small residual risks until they can offload some portion of obligations via an insurance transaction. It should be noted that Russell Investments has all the capabilities to transition a fixed income portfolio in advance of an insurance event such that tax-exempt status of pension assets can improve the negotiated terms.

Final thoughts

If an overlay is suited to your situation, it's important to seek out an implementation provider with a long history in this space as well as other complementary capabilities that are not on your list of capabilities to build in-house. Identify a shortlist of suitable candidates and manage a vigorous search process that best fits your particular needs. While many providers might be able to run such a program, one that does it every day for large clients around the world is more likely to run it better. An overlay shouldn't create additional work or confusion. Russell Investments’ Overlay Services team is well versed at reporting overlay results. And complementing existing performance reporting on your plan is a top priority.