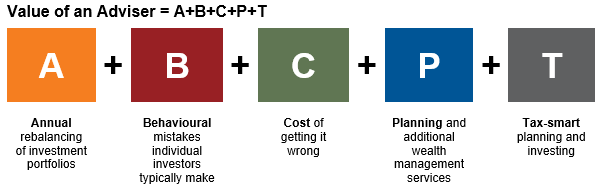

Five key ways advisers deliver value in 2019

Our annual report holistically analyses the real value advisers deliver to their clients.

Following a number of regulatory reviews, fees and trust are top-of-mind for many investors, and for advisers it can be difficult to explain what goes on behind the scenes to prepare, deliver and implement advice. That’s why it’s so important to provide a simple, easy-to-follow equation that shows the full value of an adviser’s services. It’s as easy as ABC, and then some:

A is for Annual rebalancing

When markets are rising, it can be easy to underestimate the importance of disciplined rebalancing. We believe rebalancing is vital, because it is designed to help investors avoid unnecessary risk exposure. Imagine you have a hypothetical balanced index portfolio that has not been rebalanced. In certain market conditions, it could end up looking more like a growth portfolio and expose the investor to risk they didn’t agree to. The annual rebalancing an adviser provides can help keep that from happening.

We believe there are two reasons that many investors don’t rebalance if left to their own devices:

- Because it’s an easy thing to forget to do. Investors know they’re supposed to do it. We also know we’re supposed to change the batteries on our smoke alarms once a year. But do we really do it?

- Because, in many cases, rebalancing may be the equivalent of buying more of what’s been hurting a portfolio and selling what’s been doing well. It may run counter to what an investor’s gut feelings are telling them they need. Rebalancing takes discipline. Advisers can help deliver that discipline and help position investors for long-term success.

When balanced becomes the new growth

The potential result of an un-balanced portfolio

Source: Hypothetical analysis provided in the chart for illustrative purposes only. Source for the chart: Australian Equities: S&P/ASX 300 TR Index AUD; International Equities: MSCI World NR Index AUD; Property: FTSE EPRA/NAREIT Developed NR Index AUD; Alternatives: Barclay CTA Index (AUD Hedged); Australian Fixed Income: Bloomberg AusBond Composite 0 Year Index AUD; International Fixed Income: Bloomberg Global Aggregate TR Index AUD; Cash: RBA Bank Accepted Bills 90 Days.

B is for Behavioural mistakes

Behaviour coaching is one of the most vital parts of the service an adviser provides. While there is strong evidence that portfolio value increases over time, investors can still feel compelled to react to short-term market volatility, which can undermine their long-term objectives.

Left to their own devices, many investors buy high and sell low. From December 2007 to December 2018, investors withdrew more money from U.S. stock mutual funds than they put in. All the while, $100 constantly invested in the Russell 3000® Index more than doubled in value. And those who chose to stay in cash during that period missed a cumulative return of more than 114%, based on the Russell 3000® Index. Helping your clients avoid pulling out of markets at the wrong time and sticking to their long-term plan is one-way advisers provide substantial value.

Investors don’t always do what they should. Recent proof of a ‘buy high and sell low’ mentality

U.S. open ended mutual fund and passive ETF flows vs market flows

Data shown is historical and not an indicator of future results. Sources: Monthly mutual fund, passive ETF flows and Russell 3000 Index, Morningstar, Direct. Data as of 28 February, 2019. Index performance is not indicated of the performance of any specific investments. Indexes are not managed and may not be invested in directly.

C is for Cost of getting it wrong

Investing without professional advice is often viewed as an effective way to lower the costs of investing, but there are also many things that can go wrong. The investor may not set the right investment strategy for their needs, they may lack the skills or time to filter through the many investment options available or they may be tempted to chase performance and over-react to market events.

The role of an adviser in helping clients to determine the best possible investment strategy and risk profile to meet their objectives cannot be overstated. Whether the client’s goal is to achieve long-term growth or preserve capital, this cannot be achieved without the right investment strategy and approach to risk.

In addition to investment strategy, professional advisers also bring the necessary skills to construct well-diversified portfolios, which is one of the most important contributors to long-term returns.

Advisers also provide important access to funds and strategies a client may not be aware of or able to access themselves. These include the right active strategies to build growth, complemented with passive strategies to keep portfolio costs in check, all while ensuring market timing and opportunities are not being missed.

Of course, portfolio construction and implementation are just part of an adviser’s value-add. Advisers continue to monitor the strategy set for their client and ensure all aspects of their personal finances are considered, helping the client to stay on track to achieving their financial goals.

For investors who elect to proceed without advice, there can be a big price to pay for getting a decision wrong.

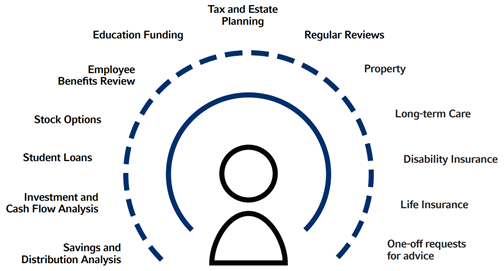

P is for Planning and additional wealth management services

Advisers build and regularly update custom financial plans, conduct regular portfolio reviews, and also offer additional wealth management services such as tax and estate planning, investment and cashflow analysis, retirement income planning, assistance with annual tax return preparation and one-off custom requests from clients.

Are your clients aware of your value?

These additional services can quickly consume 20, 50 or 100 hours each year. Make sure your clients consider what those professional hours are worth.

Planning is complex and varied

T is for tax-smart investing

When it comes to investing, it’s not what you make. It’s what you get to keep. We believe wise advisers don’t just focus on returns. They focus on after-tax returns. Providing a more tax-smart approach may have substantial impact on the size of those after-tax returns.

Good financial advisers not only have the technical expertise to help clients make the most of their tax circumstances, but can also help clients to avoid any unexpected surprises at tax time.

We believe that the value of an adviser for tax-smart investing is at least the sum of:

- tax effective investment strategies; and

- salary sacrifice pre and post superannuation contributions (depending on account balances).

The bottom line

Advisers charge for their service. The focus on fees is a daily conversation in our industry. Your clients hear that conversation. Do they also hear about the value you provide? We believe adviser value far surpasses the typical amount charged in fees. Your clients should believe the same. Remember, your satisfied clients—those who believe in your value—are your most persuasive advocates. Helping them understand the value you deliver is key. This formula offers a memorable and repeatable framework for you to have that conversation with confidence.

Access the full Value of an Adviser Report

Important information and disclosures

-

1. As background, Russell Investments has been producing the value of an adviser report in the US since 2013. Over the past 20 years, we’ve worked with top advisers around the world including the US, Canada, UK, and Australia. The study is based on our 20 years of experience coaching advisers to make their practices more sustainable and to help build deeper relationships with their clients. Over time the study has evolved to reflect the changes in the industry, new competitive forces such as robo-advice and the capital market environment.

We make reference to the study in this report and discuss some of the key assumptions it makes. -

2. "Average” US equity investor is based on general cash-flow trends as measured by the Investment Company Institute (ICI) compared to the market’s overall performance.US mutual fund data was used as robust global or Australian historical data is not currently available.