RBA skips in July, leaves door open for August hike

At the July meeting, the Reserve Bank of Australia (RBA) kept rates unchanged at 4.1%. Economists had been split on whether the RBA would hike rates again, and the market had priced a 20% chance that they would hike. The RBA’s language is similar to the April ‘pause’, with the RBA highlighting that a lot of tightening has now occurred, and they would like some time to see how the data evolves. Whilst we are near the end of the hiking cycle, we believe the RBA might return for one more hike if the labour market or inflation data come in stronger than expected. We believe that recession risk is not as elevated as in other regions but expect economic growth to slow meaningfully through the rest of this year and into the first half of 2024.

Key takeaways

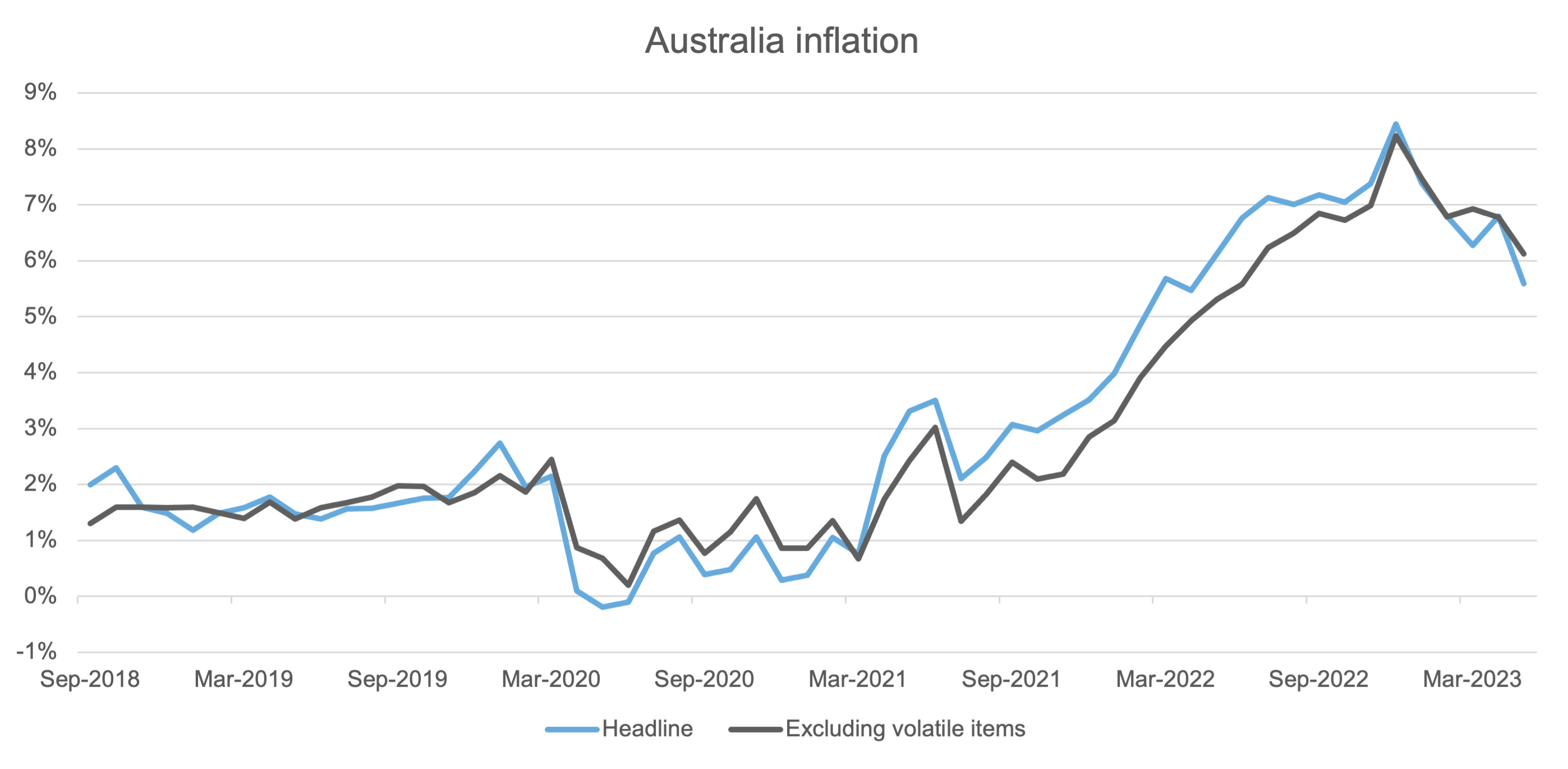

RBA still focused on returning inflation to target

Starting with inflation, it doesn’t seem that the RBA has changed its thinking about the forward path. They continue to note that inflation has passed the peak and that the monthly CPI print for May showed a further decline (as shown in the chart below). At the same time, inflation is still too high, and the RBA have reiterated their resolution to return inflation to target within a reasonable timeframe. The RBA will release their updated forecasts next month, and we will be looking to see if their forecasted path to target has sped up. We also get the Q2 inflation print at the end of July, influencing the August decision.

Source: Australian Bureau of Statistics, 28 June 2023

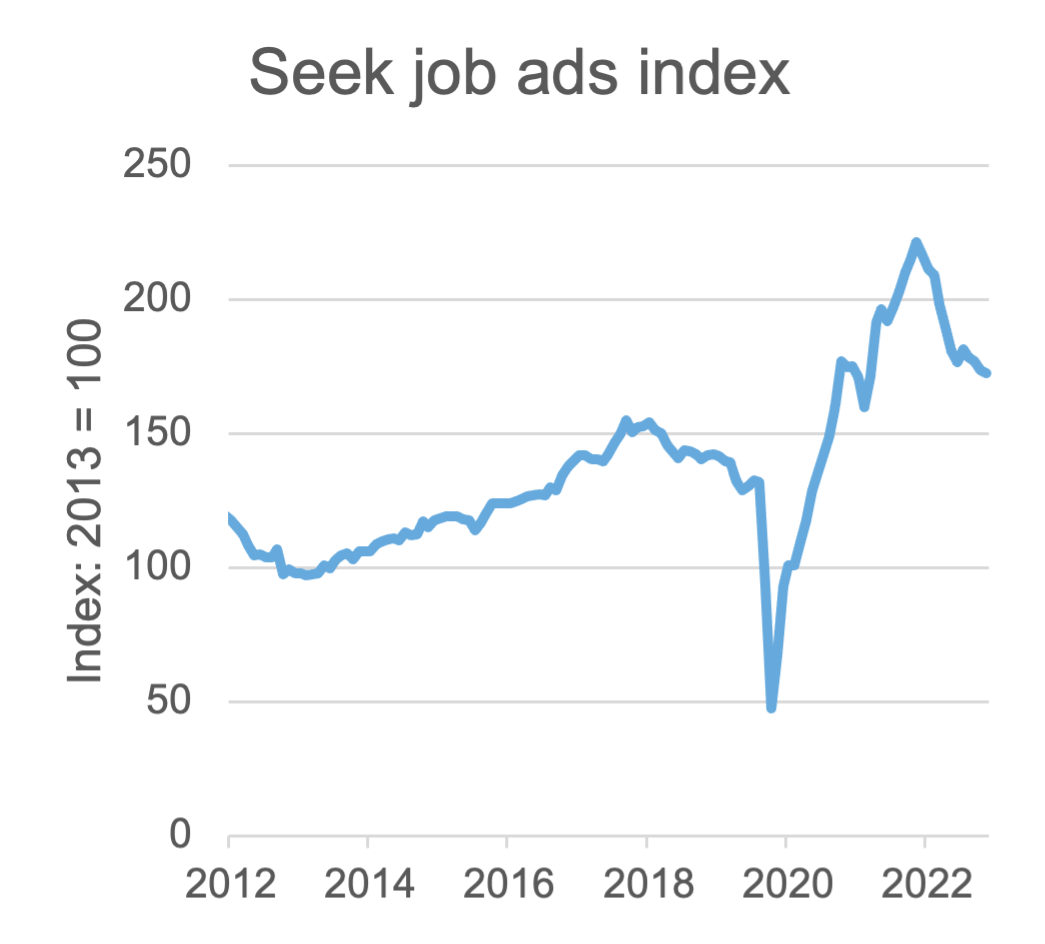

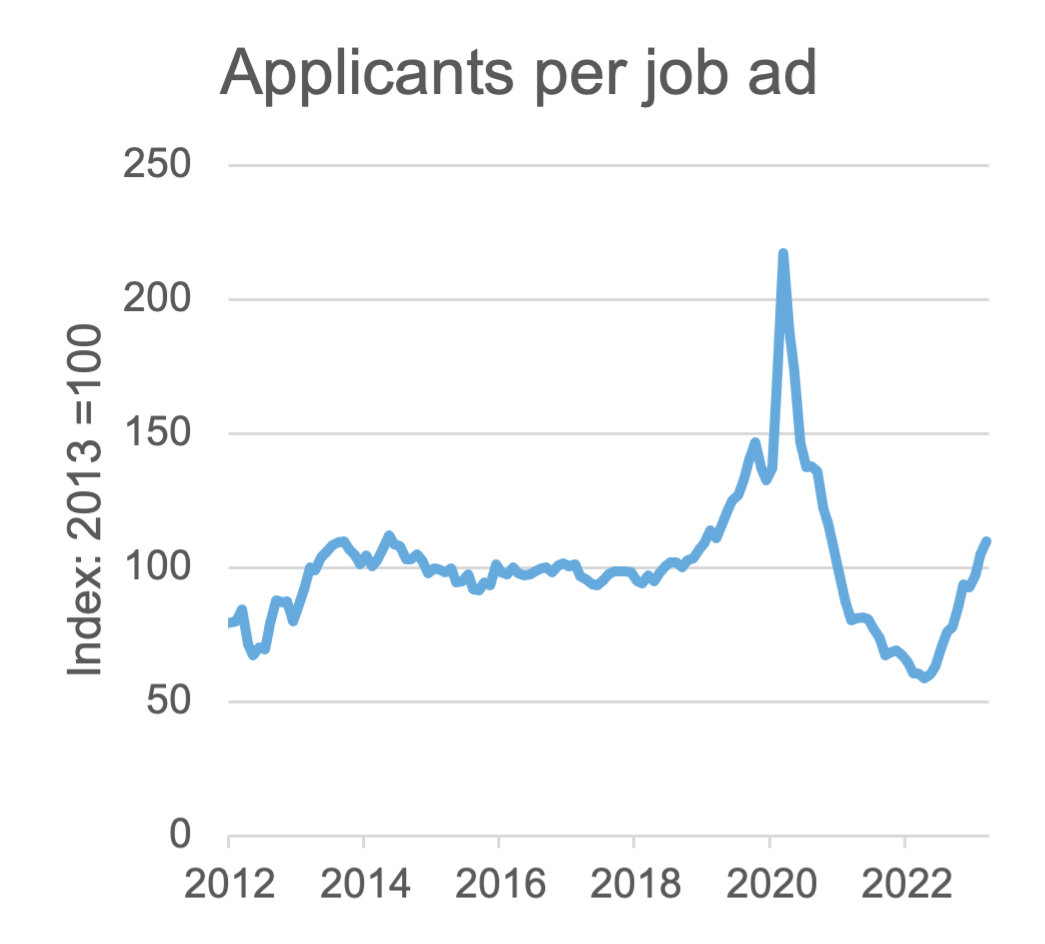

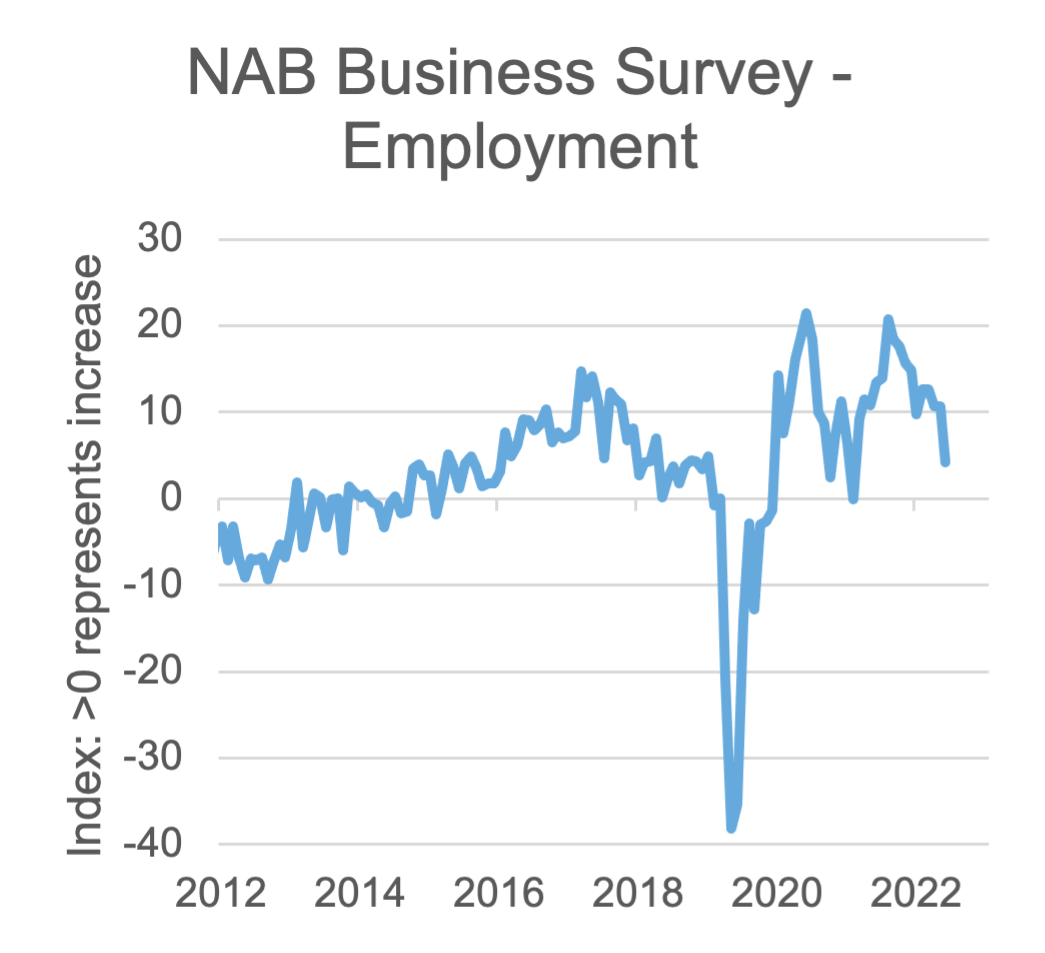

Labour market looking to slow

The labour market saw a very strong May print (following a soft April release), and the unemployment rate is now back down towards the recent lows of 3.5%. We continue to think that the labour market will slow through the rest of the year, with the NAB business survey showing a further cooling in hiring intentions and Seek data showing a further pick up in job applicants per job advertisement (suggesting that there is more supply of labour than demand).

Source: Seek, Refinitiv Datastream, 4 July 2023

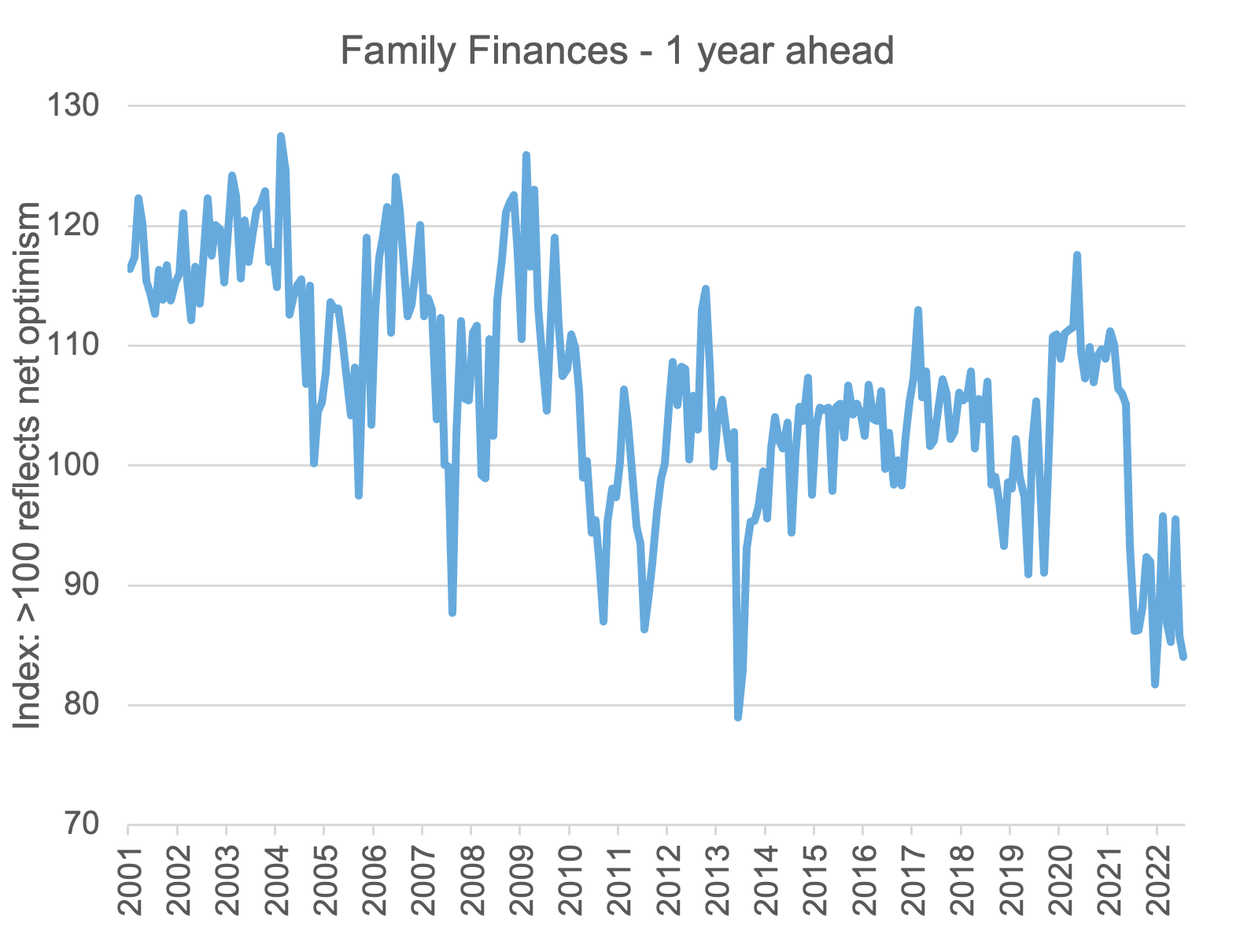

Retail sales better than expected, but family finances remain downbeat

The data around the consumer remains murky. Retail sales came in better than expected in the last two months, but it appears to be driven by colder-than-usual weather leading to earlier purchases of winter clothing and large sales driving spending. Several consumer-facing corporates (including Lovisa, David Jones and Australia Post) noted a slowdown in spending through June. We will look to the June retail sales to confirm those comments. Consumer sentiment surveys continue to show expectations on family finances remain downbeat.

Source: Refinitiv Datastream, 4 July 2023

The bottom line

Putting it all together, the RBA may feel the need to raise rates once more if inflation or the labour market comes in stronger than expected or if there are notable changes to their inflation forecasts next month. We think the economy will cool further from here, and the labour market will ease. This should lay the conditions for the RBA to be able to finish their hiking cycle sometime soon. Whilst we think that recession risks have risen given the further increase in interest rates over the last couple of months, our base case remains that Australia scrapes through with very soft growth rather than a recession. Given this dynamic, we have been adding to longer-dated government bonds across our fixed income and multi-asset funds – they are attractively valued and should provide solid returns if a bigger slowdown occurs.