Governor Lowe finishes his term on a pause

The Reserve Bank of Australia kept the cash rate unchanged at 4.1% at the September meeting, marking the last meeting for outgoing Governor Lowe. The RBA has noted that the recent trends align with their forecasts and are consistent with a return to the inflation target in 2025. We maintain our view that the RBA has likely finished their interest rate hikes now, and we are likely to see the cash rate stay steady for some time. The labour market and consumer spending are the big uncertainties for the economy right now – a rise in wage growth and a rebound in consumer spending could be the catalyst for another rate hike but is not our base case. That said, we believe it would likely require a much more serious slowdown in the economy and growing concerns of recession for the RBA to begin cutting rates.

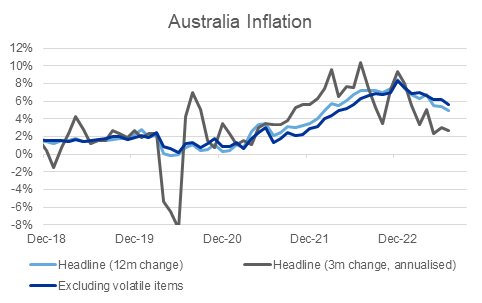

Inflation is on a path back to target

Australian inflation has continued to come down. Core inflation remains higher than headline and is coming down at a slower rate – but a lot of this is being driven by electricity and rent prices, both of which the RBA have highlighted are challenging for them to impact without causing undue pain on households. Even with those factors, as the RBA has noted, there is still a very plausible path where inflation returns to target by 2025.

Source: LSEG Datastream, 5 September 2023

One of the key concerns for the RBA has been the risk of a wage-price spiral – where a tight labour market leads to higher wages, which leads to businesses passing on those costs, which leads to a renewed bout of wage pressure. The news on that front continues to be encouraging in that those dynamics are not playing out.

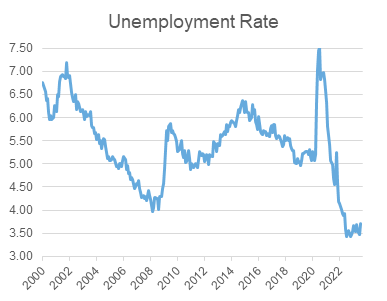

More labour market easing should come

The most recent data has shown that the labour market is cooling. The unemployment rate rose to 3.7% in July, as the economy lost 15,000 jobs. Some caution is needed when looking at job growth in July, as more people are now taking school holidays off compared to pre-COVID, potentially distorting the Australian Bureau of Statistics seasonal adjustment process.

Source: LSEG Datastream, 5 September 2023

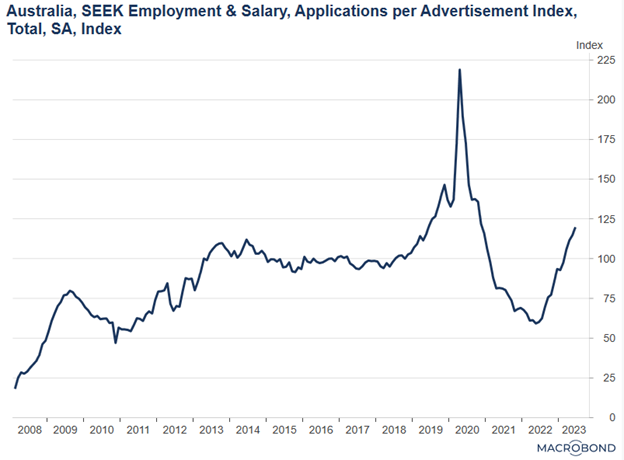

We can see the softening in the labour market through data from the job board Seek. The chart below shows that the number of applicants per job advertisement has continued to rise since the middle of 2022 and is now above the levels that we saw between 2013 and 2019. This dynamic should lead to a slowing in wage pressure – it is worth noting that wage growth disappointed economist’s expectations for a third quarter in a row, with annualized growth still below 4%.

Source: Macrobond, 5 September 2023

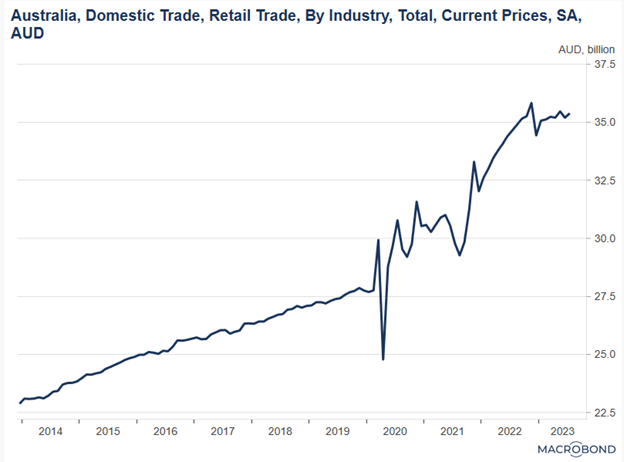

Households are reducing their discretionary spending

Consumer spending is likely to continue to slow as the last of the RBA’s rate hikes flow through to households. Based on CBA’s recent earnings result, about two-thirds of the increase in the cash rate has flowed through to mortgage payments – so there is still a third to go. Retail sales have seen minimal growth over the last three or four months, as shown in the chart below. Some of the spikes in recent months have been driven by the weather being colder than normal and pulling forward spending on warmer clothes.

Source: Macrobond, 5 September 2023

Portfolio Implications

We maintain our view that economic growth in Australia is going to slow, but we will likely avoid recession. In that environment, we think the RBA has likely finished raising rates, but it will be some time before they look to cut rates. Globally, we believe that recession risks are more elevated as the US Federal Reserve has been more aggressive in its rate-hiking campaign. Term deposit rates in Australia have likely peaked or are close to peaking; however, Australian government bonds have become much more attractive given the RBA have likely finished raising rates, and growth is set to slow. We have added to our government bond position over recent months to take advantage of the attractive valuations and cyclical support.