Capital gain distributions in a down year? It’s happened before and will happen again.

However, things weren’t quite so positive for investment portfolios. In fact, in 2018 there was the confluence of two negative events: negative market returns first off, whose impact was further negatively compounded by the tax impact of large capital gains distributions. For investors, that added insult to injury, with many likely receiving a big tax bill on a portfolio that had lost ground.

As Mark Twain said, “history doesn’t repeat itself, but it often rhymes.” It appears that 2022 has an awful lot in common with 2018. Let’s look at the chart below.

Click image to enlarge

Source: Morningstar Direct. U.S. Stocks: Russell 3000® Index. U.S. equity funds: Morningstar broad category ‘U.S. Equity’ which includes mutual funds and ETFs (and multiple share classes). For years 2001 through 2020 % = calendar year cap gain distribution ÷ year-end NAV, 2021 & 2022 % = total cap gain distribution ÷ respective pre-distribution NAV. For years 2001 through 2013, used oldest share class. 2014 forward includes all share classes. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

Capital gain distributions happen in all environments

Many investors in a down market year, while not happy about it, might say something like: but at least I won’t have a big tax bill. That is a common thought: that if your portfolio isn’t making gains you also aren’t creating taxable events. Au contraire! The chart makes it pretty clear. It's pretty clear that market performance has no relationship to capital gain distributions. In fact, some of the biggest capital gain distributions (which are what generate many of the outsized tax bills that investors experience) happen in years where the market is down.

Investors may have to pay taxes on distributions in good market years, flat market years, and yes, even bad market years. While your clients may be accepting of a tax bill on their investments when their portfolio has risen in the previous year, they may be understandably confused and frustrated to about paying taxes on a portfolio that has declined. It’s important for investors to understand that this can happen, that taxes due to investments can occur any year. Education here is key to make sure that investors, even if not happy about it, understand it. It will make the conversation easier to be had when bad year tax bills happen.

2022 rhymes with 2018

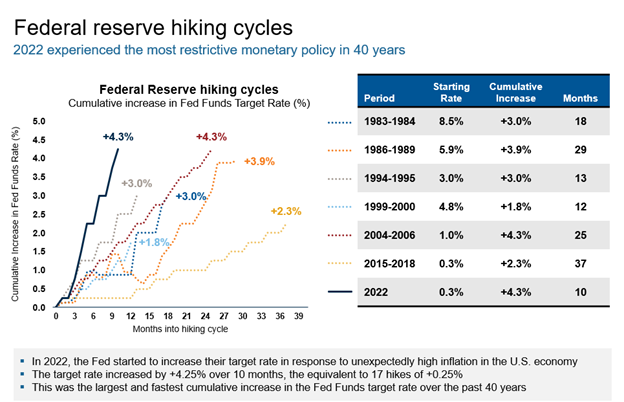

As a refresher, in 2018 markets ended on a sour note. The fourth quarter in particular is where the market took a dive as the Russell 3000 had a -14.3% return. What was the cause of the dramatic selloff in the back end of 2018? Ironically, one of the root causes was the U.S. Federal Reserve raising interest rates. While the 2022 experience is not identical, it sure does seem to be rhyming. There is a difference, however, as the rate hikes in 2018—from 1.5% to 2.5%—were significantly smaller than the rapid escalation in rates throughout 2022. We have seen interest rates rise from a mere 0.25% (upper bound) at the start of the year to 4.5% to close out 2022.This is a dramatic rise, one of the largest and fastest we have seen in a long time, as demonstrated in the chart below. Another key difference is in the overall returns for the year, with the Russell 3000 Index only falling 5% in 2018 compared to a 19% fall in 2022.

Click image to enlarge

What else do the two years have in common? Other than how hard it was and still is to buy Taylor Swift tickets, I mean.

The answer in short is … sizable capital gain distributions. In 2018 U.S. equity funds paid on average a 11% capital gain distribution. Let’s put some numbers behind that. If a client had $500,000 in a non-qualified account and received an 11% capital gain distribution, that is $55,000 in capital gains that will be noted in the Form 1099-DIV. Apply a 20% tax rate and that’s an $11,000 tax bill on a portfolio that received a negative return. Not the outcome most investors expect in a down market year.

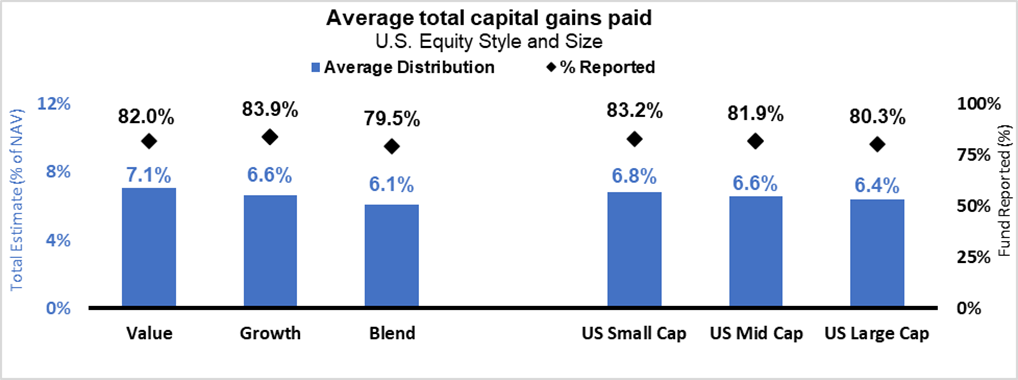

In 2022, the average capital gain distribution from a U.S. equity fund was 7%, so the tax bill is likely to be slightly smaller. Using the same example of a client with $500,000 as above, with a 7% capital gain distribution and a 20% tax rate, that comes out to about a $7,000 tax bill. This in a year where the market was down nearly 20%! This is fortunately (or unfortunately?) now water under the bridge. The questions to ask going forward are: should your clients pay taxes on their distributions at all? And what can be done to minimize their tax bill going forward?

Click image to enlarge

Source: Russell Investments and Morningstar Direct, as of 12/31/2022. Categories based on Morningstar Category Group which includes mutual funds and ETFs (and multiple share classes). The average capital gain distribution % is calculated using the total capital gain distribution and respective pre distribution NAV as reported by Morningstar. % of NAV is calculated as (total capital gain distributions ÷ respective pre distribution NAV).

The power and value of tax management

Some financial advisors look at doing Roth conversions in IRAs when accounts are down in value. But there are many tax-smart moves you can make for your clients with non-qualified accounts when markets are falling.

Negative markets provide plenty of opportunities to harvest capital losses—losses that can then be used to offset gains today and in the future. You may also be able to use some of the generated capital loss to offset up to $3,000 of income a year. The benefit of harvesting losses within a portfolio is that taxes are only paid on the net profit—the difference between the gains and the losses. This can significantly reduce an investor's tax bill.

There is more that can be done beyond just harvesting a few losses and saving them for the future. You can actually help the investor take a big step forward into tax-managed investing. With account values down, unrealized gains are also down. That could provide the opportunity to make lemons into lemonade by transitioning out of tax-inefficient products and strategies into more tax-smart strategies. The time is right to transition from a tax- inefficient portfolio into one that is managed to reduce the impact of taxes and aligned with long-term after-tax wealth creation.

It's fair to say that no one wants to pay more taxes than they have to. This is especially true after a year of negative market returns, like 2022. And we know that reducing investment-related taxes can have a significant impact on an investor’s wealth. Fewer taxes going to the taxman could mean more money left in your client's account to invest and grow. And that means an increased likelihood of a more comfortable retirement nest egg.

The bottom line

In many other ways, 2022 was similar to 2018. Apple’s market capitalization was a hot topic once again as it briefly touched above $3 trillion (but then it lost nearly $1 trillion). Prince Harry and Meghan Markle were in the news again, although for less happy reasons. And Saudi Arabia was also in the news with another big surprise—posting the biggest upset in World Cup history when its team beat Argentina … even though Argentina won the whole thing at the end.

You can also ensure that any future negative market years aren’t a repeat of either 2022 or 2018 for your taxable clients. You can take steps to ensure that 2022 is the last year in which they will receive the double-whammy of investment losses and a tax bill on their distributions. But if there is such a thing as a positive double-whammy then moving to tax-managed investing provides it: not only will you help your clients save money, you can reinforce the value that you provide as an advisor.