Investments for DC plans

Defined contribution investment solutions designed to improve participant outcomes.

A well-designed defined contribution (DC) plan will typically offer a combination of default investments for participants who wish to leave the oversight of their portfolios to a professional, along with other core investment options for those participants who prefer to be more personally involved.

Target date strategies have become the centerpiece of many DC plans in their role as a qualified default investment option (QDIA). In addition to our LifePoints® Institutional Target Date Strategies, we offer several default investment options to meet the unique needs of your plan, including custom Target Date strategies. We also offer a large selection of individual, institutionally priced multi-asset strategies in traditional asset classes and real asset solutions for an efficient core investment menu.

Recognizing the characteristics of your employee investors

We believe retirement plan participants often fall into three tiers, each of which has a corresponding investment solution that may satisfy their needs and help make their investment decisions easier and more relevant.

TIER 1 "Do it for me"

Typically 60%-80% of total participants

Participants who would like a professional to design, construct, and manage their investment portfolios and asset allocations. For these participants, target date or asset allocation strategies offer the right characteristics. The LifePoints Institutional Target Date Strategies qualify as QDIA investments (see below) and can be a good fit for these "Do it for me" investors.

TIER 2 "Do it with me"

Typically 20%-30% of total participants

Participants who like to design, construct, and manage their own portfolios, but want someone to provide them with well-built investment options they can use. For these participants, a well-designed core menu is key. We offer a range of multi-asset strategies that can be used to create an efficient core menu.

TIER 3 "Do it myself"

Typically 2%-10% of total participants

Participants who want full flexibility to design, manage, and construct their portfolios. For these participants, a brokerage window (self-directed brokerage account) provides access to the range of investments they want.

When selecting investment options, plan sponsors should consider the characteristics of their employee base. All participant needs are not created equal. While many plan participants could be well-served by having access to professionally managed, asset allocated portfolios, others may prefer to be involved at some level in building and maintaining their own portfolios.

Know your qualified default investment alternative (QDIA) choices

Balanced strategy

A product with a mix of investments that takes into account the characteristics of the group of employees as a whole, rather than those of each individual participant.

Capital preservation product

Allowed only for the first 120 days of participation for sponsors wishing to simplify administration if workers opt-out of participation before incurring an additional tax.*

Target date strategy

A product with a mix of investments that takes into account the individual's age or retirement date.

* Source: "Regulation Relating to Qualified Default Investing Alternatives in Participant-Directed Individual Account Plans," a DOL fact sheet available at: https://www.dol.gov/sites/dolgov/files/ebsa/about-ebsa/our-activities/resource-center/fact-sheets/final-rule-qdia-in-participant-directed-account-plans.pdf

What is a hybrid QDIA?

A hybrid QDIA combines an asset allocation QDIA solution, such as a target date or balanced strategy, with the features of a managed account. Participants can be defaulted into different types of QDIAs depending on their age and financial circumstances.

Retirement plan solutions

¹ These are collective trust funds that are bank-maintained collective investment funds managed by Russell Investments Trust Company, a Washington state non-depository trust company, and are not registered mutual funds. The funds are only available to certain qualified employee benefit and government plans and are not offered to the general public.

Incorporating a multi-asset investment approach

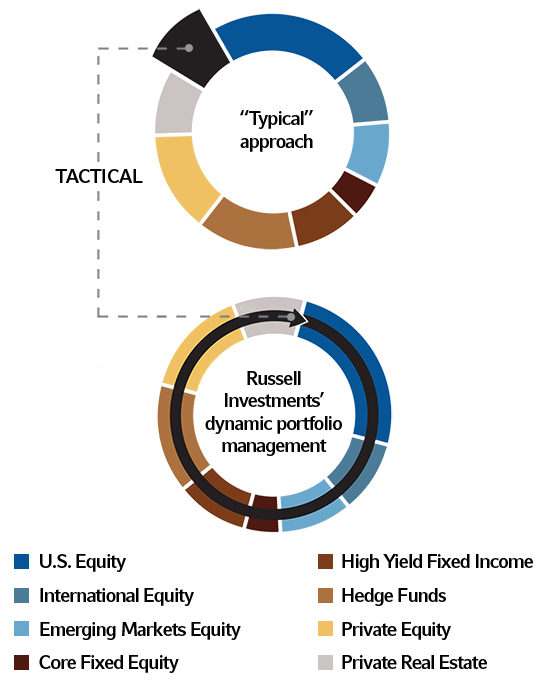

Multi-asset investing is the process of incorporating exposures to a globally diverse mix of asset classes and dynamically managing those exposures to capture short-term return market opportunities and to mitigate risks. While in most portfolios, tactical shifts are a separate sleeve of the portfolio, our multi-asset approach is designed to make tactical shifts throughout the portfolio that are informed by the underlying holdings of the managers and strategies. This allows the portfolio managers greater flexibility to adapt the portfolio for short-term market shifts and retain long-term return potential.

This strategic, multi-asset approach is designed to enhance returns and mitigate risks and it requires the skills of a team of full-time, dedicated, experienced investment professionals. This capability is built into every OCIO solution we offer to our clients.

Multi-asset investing is an integral part of our DC solutions.

This portfolio is constructed using single asset class sleeves combined with an additional tactical sleeve bolted onto the portfolio. In this type of portfolio construction, each sleeve is managed separately, and the tactical sleeve is applied without taking into account the current position and risk budget of the managers in each individual asset class sleeve.

In this approach, the decision about what tactical shifts to make are informed by the underlying holdings of the managers and strategies, plus the risk budget of the total portfolio and the shifts taking place in the market. This approach gives our portfolio managers greater flexibility to adapt the portfolio to short-term market shifts to help retain long-term return potential.

The financial well-being of your defined contribution plan is critical to ensuring that you're able to provide high quality results to your participants. That's why it's so important to work with a provider who has experience holistically managing distinct asset pools and aligning them with the financial outcomes desired by your organization.

We'd love to put our team to work helping you achieve your goals.

Related research, articles, and insights

DC retirement handbook

We geared this handbook for DC investment committees, CFOs, and HR employee benefits professionals. It can help you better understand today's DC market and prevailing best practices as you build and manage a plan to help participants meet their retirement income needs while fulfilling your fiduciary obligations.

Our experts work hard to solve the complex issues our clients encounter.

Our collection of research shows our dedication to solving complex investment problems.

Partner with us

Get in touch with us through this form, and we'll reach out to you.

Kerry D. Bandow, CFA

Senior Director, Defined Contribution Solutions, North America Institutional