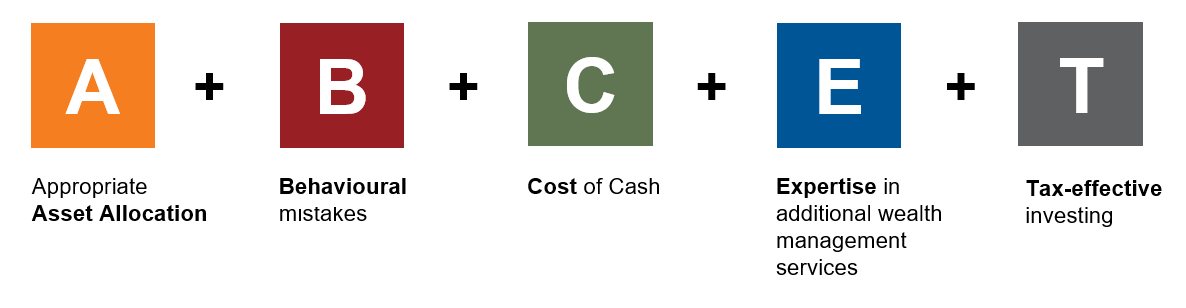

E is for expertise in additional wealth management services. See why it's so valuable to investors

Russell Investments believes in the value of advisers, based on this simple formula:

When you position your expertise and additional services to your clients, be intentional. First of all, you, the adviser, need to recognise how important these additional services can be for a clients overall financial goals and how much it is worth. Then, you need to position your planning process appropriately to your clients so that they, too, see the value. After all, expertise in bringing a plan together and done correctly, is not a one-time step. It’s an ongoing process that keeps investors on track. How much is that worth?

Let’s look at the expertise you bring in building a plan for your clients.

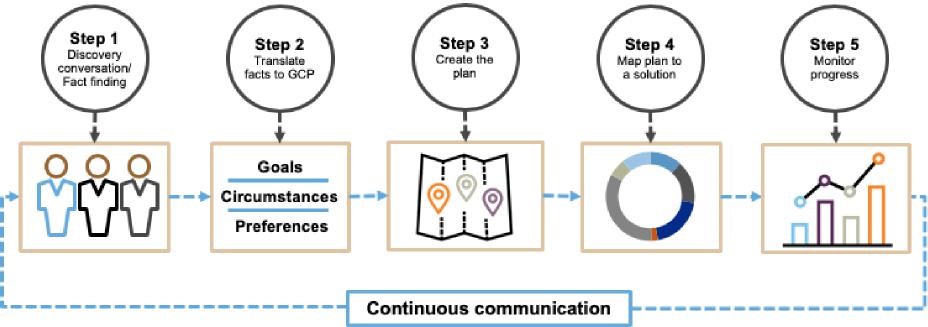

The planning cycle in five steps

- Delivering wealth management begins with a deep client discovery conversation. This should be a conversation led by open-ended questions, where the adviser does more listening than talking. In some instances, for existing clients, this means going back and having a rediscovery conversation. Take the time to reflect with your clients by re¬igniting a fact-finding process to ensure that all the activities and solutions are still driving toward the right outcomes.

- The next step is to translate that discovery conversation into goals, circumstances and preferences.

- Goals are the fundamental problems involving money and time that clients are trying to solve. The importance of goals must be defined by the client. Then it’s the adviser’s job to convert the stated goals into accumulation and spending milestones.

- Circumstances are the unavoidable facts that define a client’s current situation. Under the heading of circumstances, we might include a clients’ investment-account balances and their tax status, along with their stage of financial life, marital status and ability to save more or spend less.

- Preferences are a bit more flexible. These are the things that clients desire in their investment solution rather than need. Oftentimes, advisers have simplified preferences down to a risk profile, to see what risk level an investor prefers. But clients also care about their portfolio drawdown potential, cash flow consistency, and illiquidity. These days, more and more investors also approach investing from a values point of view, with preferences on portfolio holdings such as carbon, tobacco, munitions and other socially responsible issues. Advisers must always first meet goals. But the best approach is still to try to align the goals with preferences. That will lead to happier clients

- The third step is to create the plan. In order to do so, we believe you must know where ALL of the money is located, including views into insurance, wills, trusts, mortgages, etc. We believe this holistic approach is in the best interest of investors. Without it, your plan could be operating at crossed purposes with other hidden aspects of your investor’s financial picture. We’ve seen this happen many times over the years with the advisers and investors we’ve worked this. It pays to get the complete picture so you can build the right plan the first time.

- Step four requires you to map the plan to a solution. Many of the top advisers I have coached look for scale for the majority of their investors, when appropriate to do so such as managed portfolios. They often use the same portfolios as a core to build customised solutions for their suitable clients, households and families.

- And finally, the framework should be wrapped in a process to monitor progress, with ongoing communication between the adviser and investor, as goals, circumstances and preferences evolve over time. As I said earlier, planning is an ongoing process, not a one-time thing. Make sure your clients know this. And then make sure you do it.

The value of listening

You’ve heard me say this before, but listening is truly a competitive advantage for advisers who do it well. Not everybody does it well. The most brilliant conversationalists are great listeners. Especially in this day and age of media talking at us, being truly heard is a rarity. Listening is the quiet key to human connection, and leads to deeper relationships with your clients. A client’s financial message, both verbal and non-verbal, is only as good as you listening to it, retaining it, and then building it into their plan. Listening done well is truly a gift to clients – and a potential opportunity for further planning. Clients can’t always articulate their financial needs, so great listening can lead to uncovering additional opportunities.

Reminding them of the value of your Expertise

Don’t let your clients forget the value that you have already delivered, and the opportunity of the value you can continue to deliver into the future. Too often we hear from Advisers that assume that their clients remember all the great things that have been achieved so far and the value that has been delivered from this expertise. You can remind your clients of your technical expertise through the monitoring of progress of the plan and how they are tracking to their goals. But consider how you can also remind them of the types of intangible value you are also delivering.

For your time poor clients, remind them of the hours saves or the efficiency you have created for them by outsourcing their financial matters to you in such an effective way.

For your worried clients, remind them of how your ongoing engagement model help provide ongoing communication of important information that hopefully provides peace of mind and confidence that they are on the right track.

For your confused clients, remind them of how your years of experience can help them navigate the complexities of super, tax, investment and all the other facets of a financial plan and bring them confidence and conviction.

For your reactive clients, remind them how the plan helps provide the roadmap and the opportunity to discuss through their thoughts and ideas as they share them, and how you can make rational and sensible decisions together on when to take or not take action.

Remember the rule of 7: an audience needs to hear a message 7 times for the impact to truly sink in. Engaging repetition is the key!

The bottom line

Don’t make the mistake, as we’ve seen with plenty of advisers, and give planning away for free during the prospecting phase. Creating full plans, then handing them to prospects who then walk out the door without implementing, is a waste of your precious time. And it doesn’t do your clients any favours either. Having a robust plan might feel reassuring, but it’s only as good as its implementation. As all good advisers know, a plan is out of date as soon as it is finalised, because life happens. The value comes from the experience of an adviser who can continuously adjust the plan to align with the client’s changing needs.

Experience in understanding a clients’ complete financial needs and the ability to tap into those additional wealth management services to complete their overall plan is incredibly important. A client’s plan is the heart of their financial lives, and related life topics will continuously come your way to be incorporated. Issues like career changes, non-essential healthcare procedures and bucket-list trips will emerge for an adviser’s valued opinion and experience. So own the value of the experience you offer your clients’. Don’t give it away.