2020年 ESG運用機関 アンケート調査:加速する取り組み

※以下は、2020年10月6日にラッセル・インベストメント(米国)のHPに掲載された英文記事を翻訳したものです。

ラッセル・インベストメントは、グローバルの株式、債券およびプライベート資産の運用機関を対象とする2020年ESG運用機関アンケートを実施し、責任投資への取り組みと投資プロセスにおけるESGファクターの考慮について調査を行った。調査は2020年5月26日から7月17日の期間に行われ、調査結果は2020年10月6日に発表された。

環境・社会・ガバナンス(ESG)ファクターの重要性は増したのか、低下したのか?

ラッセル・インベストメントが実施した2020年ESG運用機関アンケートの結果によると、資産運用業界における責任投資への取り組みは加速し、ESGインテグレーションは投資機会の分析における重要な考慮事項と広く認識されている。ますます多くの運用機関が投資プロセスにおいてより多くのESGファクターを考慮しており、責任投資のためのリソースを増やし、レポーティングを通じて透明性を高めている。ESGデータベンダーは投資対象となる企業や団体について幅広い視点を提供する不可欠な存在であり、エンゲージメント活動も運用機関がESG関連の情報を取得し活用する上で重要な役割を果たす。さらにアンケート結果からは、気候変動リスクへの注目度が上がっていることに加え、気候変動リスクに関する指標が改善し続けていることが分かった。

ESGファクターと気候変動リスクへの着目

ラッセル・インベストメントは、グローバルの株式、債券およびプライベート資産の運用機関を対象とする2020年ESG運用機関アンケートを実施し、責任投資への取り組みと投資プロセスにおけるESGファクターの考慮について調査を行った。本年のアンケートは、以下の事項を含む幅広いトピックを網羅している。

- 投資プロセスにおけるESG要素の考慮

- 使用するESGデータ

- ESG要素を考慮する資産クラス

- ESG評価の方法

- 気候変動リスクによる影響

- 責任投資のためのリソース

- エンゲージメント活動

- 提供する運用商品

- レポーティング

このアンケート調査は2015年の開始以降、ここ数年で内容に変更を加え、資産運用業界における責任投資に関するトレンドや運用機関の取り組みの変化について深く理解することができる。

ラッセル・インベストメントは投資プロセスにおいてESGファクターを考慮している。運用機関の調査プロセスの一要素として、運用機関調査アナリストは個々の投資戦略に対しESGランクを付与する。ESG運用機関アンケート調査には、各運用機関のESGへの取り組みに関する豊富な情報が含まれている。そのため、同調査結果は個別の投資戦略の評価において、非常に重要な参照情報となる。

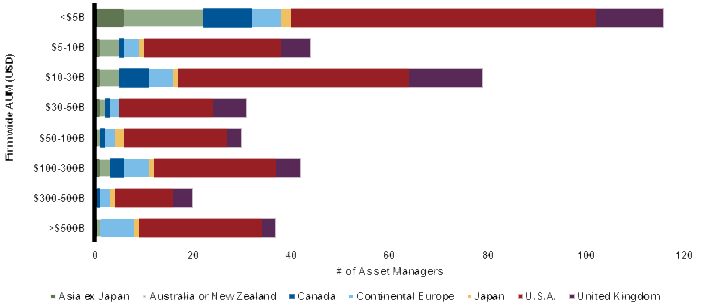

2020年のESG運用機関アンケート調査には、グローバルで400社の運用機関が参加し、これは前年比で33%の伸びとなった。同調査に参加した運用機関は、資産規模、地域、投資戦略において多様な運用機関で構成されており、内訳は以下のとおりである。400社のうち、300社が株式戦略、208社が債券戦略、127社がプライベート・エクイティ戦略、そして121社がリアルアセット戦略を提供している。また全体の60%が米国、14%が英国、8%が大陸欧州に本社を置き、残りは他の地域である。さらに、運用資産残高が100億ドル未満の運用機関が全体の40%を占めている一方、資産規模が1,000億ドルを超える運用機関は全体の25%であった。

Survey population

Click image to enlarge

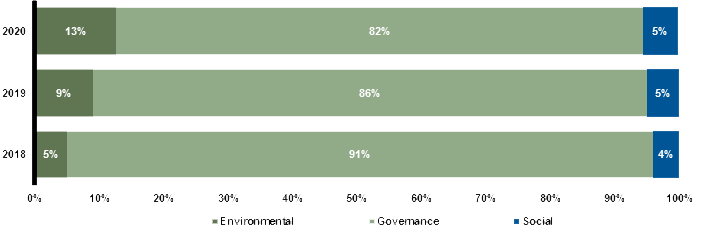

投資判断を左右するESGファクター

ESGファクターのマテリアリティへの注目は、ますます高まっている。入手できるESG関連の情報が広がる中、ESGインテグレーションの実践方法も進化してきている。ただし、ESG評価が実際の投資判断においてどの程度の役割を果たすかは、ESG評価が他の調査活動と複雑な関連性を持つことから、現時点では不明瞭である。この点を明らかにするため、今回の調査では投資判断に最も影響を与えるESGファクターについて尋ねた。ガバナンスが引き続き、最も重要なファクターとなっている。

企業のマネジメントが長期的な企業価値に対し最も重要な要素であることを考えると、この結果は理解できる。但し、昨年の回答と比較してみると、環境ファクターと社会ファクターも上昇する傾向が見てとれる。

投資判断に最も影響を与えるESGファクター

Click image to enlarge

Active ownership continues to rise in prominence

When asked to identify the primary source of ESG information, engagement activities are viewed as the most frequent primary source of ESG-related assessments. To support this trend, asset managers are increasing their engagement activities with underlying companies, or in some cases, governments, in order to influence entities' potential outcomes such as greater transparency, improved behaviours and reduced uncertainty and risk. Almost all of the firms with assets under management greater than US$100 billion always or occasionally included ESG discussions in meetings with senior management, compared to 74% of firms with asset size less than US$10 billion. 10% of the respondents cited that they don't engage in any way with companies, and those firms include systematic equity managers, fixed income, private markets and real assets managers.

The survey also indicates that engagement activities increased even among fixed income managers, where 92% of fixed income managers regularly engage with underlying companies they invest in. Bondholder engagement has become a crucial part of the responsible investment approach and process. A growing number of bond investors hold the view that engagement activities can provide greater insights into the underlying companies or entities, improve transparency and influence business practices. As the importance of active ownership continues to increase, so will the consensus among investors to incorporate active management across all asset classes.

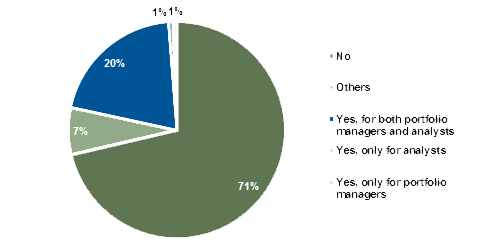

ESG accountability - client or financial driven?

While asset managers are broadening their perspective of ESG measures, the question remains whether such efforts are client-demand-driven or financial-result-driven. To gain a deeper understanding, we asked participants if they have portfolio performance measures that have direct ties to ESG profiles or climate-risk criteria for the strategies that are not labelled as responsible investing or ESG offerings. In other words, do they use ESG or climate-risk without marketing those efforts? Only 22% of the respondents have portfolio performance measures for portfolio managers and/or analysts with direct ties to ESG-profile or climate-risk criteria. This shows that ESG profile accountability is weak among key investment professionals, suggesting that ESG impacts alone have less weight to investment performance outcome than the hype of ESG integration suggests. Despite the weak accountability, we believe it is essential for asset managers to integrate ESG within the investment process. Regulations across the globe evolve. European regulators seek to support the Paris agreement via extensive regulations that quickly come into force over the next few years, starting 2021. Meanwhile New Zealand recently mandated support for the TCFD. And the U.S. Department of Labour has moved to steer Employee Retirement Income Security Act of 1974 (ERISA) governed plans away from investing in products with ESG-related themes. This increase in regulation will encourage further transparency amongst asset managers, providing investors with clarity and reducing the risk of green washing.

Do you use any portfolio performance measures that have direct ties to ESG profile or climate-risk criteria?

Click image to enlarge

The bottom line - ESG is amplified

Russell Investments ESG Manager Survey 2020 revealed a high level of ESG awareness and increasing ESG factor integration among the asset management community. The survey results conclude that ESG integration enables a more comprehensive ability to analyse underlying companies, beyond the traditional company analysis. An increased number of asset managers are gathering ESG-specific assessments into their investment process. However, despite the increase, the degree of ESG integration and the methodologies vary, especially by region, by firm asset size and by asset class. As local ESG and responsible investing regulations increase, this trend is also influencing how asset managers are incorporating ESG criteria into their investment processes, with greater transparency and reporting. We believe recognising those regional and AUM differences is important when evaluating peer-relative investment strategies.

ESG metrics expanded, along with ESG data providers, where more asset managers are using multiple data providers to broaden ESG-related awareness and perspective. More asset managers form their ESG insights with inhouse views supplemented by external ESG data providers. As engagement was cited as the most popular ESG information source, these activities increased even among fixed income managers.

Russell Investments integrates ESG in its manager research practice, and this ESG survey helps form our assessment of managers' ESG integrations as a part of manager strategy evaluation. The results of this survey point to a marketplace that has reached universal recognition of the importance of ESG integration. We believe that the industry is transitioning toward further embracing ESG integration, using broader inputs, ESG-specific data and dedicated resources. At the same time, measurements of actual impact on investment decisions remain vague. When financial materiality of ESG-specific consideration is high, investors take such information into consideration. But anecdotally, such instances appear rare. The link between ESG effort and a direct tie to portfolio performance directly to ESG factors is weak, suggesting that ESG criteria in isolation are rarely a strong driver in overall investment decisions.

Our research demonstrates that the investment community is seeking better information, deeper resources, broader consideration and clearer regulatory standards. However, the key question remains - 'to what degree'? The goal is to achieve the best-practice ESG integration. Agreement on how to reach that goal? The world is clearly not there yet.

To download the full report, click here.