Six tax planning strategies for a good start to 2023

With 2022 in the books, the question I want to pose right now is: how many of your clients are upset about their portfolio’s performance last year… and the fact they may have to pay taxes on capital gains anyway?

My next question is: do you want to avoid having those kinds of uncomfortable conversations going forward?

Now is the time to not just consider those questions but to take action to align your clients’ portfolios for a better after-tax outcome. Implementing tax-smart strategies as early as possible in the new year will help set your clients on an improved tax-management path for the rest of 2023, and better align their investments to meet their retirement goals. Moreover, by doing so, you can show your clients the value of working with a tax-smart advisor: they are likely to have more money remain in their portfolio to continue to grow and compound.

Being a tax-smart advisor isn’t just about reducing the tax drag on your clients’ taxable accounts, it’s about aligning their total investment plan for a more optimal outcome. It’s about both saving and investing, and the strategies that can help them on to a smoother path for their future. With everything that we have going on in our lives and daily workloads, it’s easy to take some or even all of these things for granted. As their advisor, much of the value you can bring to your relationship with your clients is to guide them along their path to a financially healthy retirement.

Here are some ideas to get the conversation started:

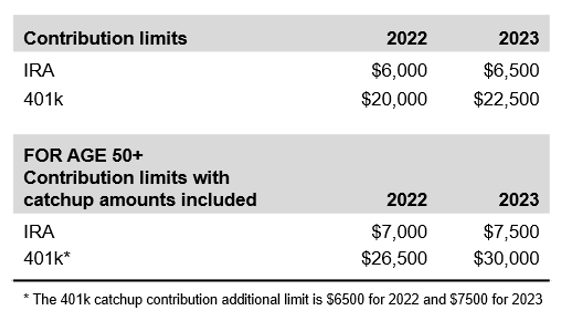

1. 2022 and 2023 IRA contributions

Investors should take advantage of these tax-advantaged accounts to grow their retirement assets. Traditional IRAs allow investors to contribute pre-tax dollars, which lowers their current year tax liabilities. And the assets in the IRA grow tax-free, which is a big benefit of these accounts. While the annual contribution limit is not large, these accounts are a good complement to other components of an investor’s total savings and investment picture.

For 2022, the IRA contribution limit was $6,000, and individuals over the age of 50 could make catch-up contributions of $1,000, bringing their allowable amount to $7,000.

For 2023, those contribution limits are increasing: to $7,000 for individuals under age 50 and $7,500 for those over the age of 50.

Check to make sure your eligible clients have made their 2022 contributions. There’s still time—until April 15 – to make those contributions!

Click image to enlarge

Source: Internal Revenue Service, Russell Investments

2. 2023 401k contributions

For 2023, the 401k contribution limits have been increased from $20,500 to $22,500. As a tax-smart advisor, you’ll want to make sure your clients are taking full advantage of this. 401k plans (and 403b’s) are a primary form of retirement savings in the U.S. in lieu of the defined benefit pensions of years past. In addition, most employers will contribute to an individual’s 401k plan in the form of a match. This is, in essence, “free money” that not everybody takes advantage of. Make sure your clients don’t miss out.

Here’s a good analogy for those who may hesitate: If you wouldn’t ignore a $100 bill sitting on a sidewalk, then you shouldn’t ignore the thousands of dollars of this free money either. It might be worthwhile for you to look at the elections your clients have made with their employers and ensure they are taking full advantage of their 401k plan and maximizing their pre-tax retirement savings.

If you are looking for an easy way to broach the subject with your clients, here’s an idea. One of the most important numbers with respect to 401k plans is the number 50? Why? Once your client hits the age of 50, they can make catch-up contributions. The limit in 2023 for catch-up contributions is an additional $7,500. This allows an eligible individual to save up to $30,000 a year in pre-tax dollars for retirement in 2023. This is a handy benefit for investors who maybe didn’t give enough thought to retirement earlier in their career and now realize they might be a little short.

Work with your clients who have contribution room in their 401k: they will benefit both from immediate tax savings by lowering their taxable income, and benefit from the potential growth of their portfolio not being taxed until they start taking distributions. This is a good way to build a tax-deferred nest egg and a good way for you to introduce your clients to the double-barreled benefit of reducing the tax drag on their portfolios. Then you could look at moving their non-qualified accounts to tax-managed investing solutions so those funds also reap the same benefits.

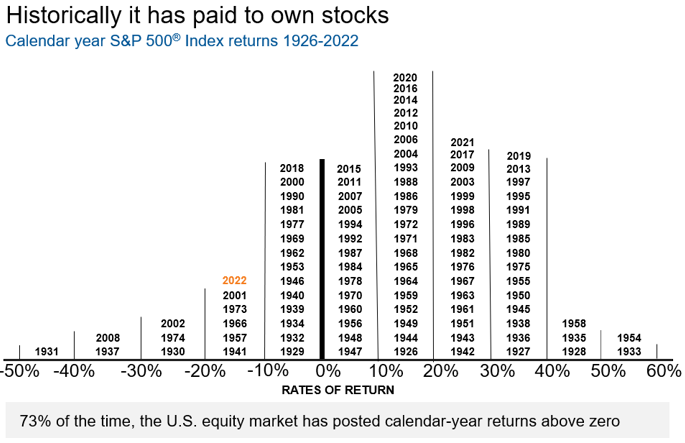

3. Tax-loss harvesting – It’s not too late

With 2022 in the books, it’s easy to throw in the towel on the previous year. It’s too late to harvest tax losses, isn’t it? While it’s easy to think that, and understandable that many investors assume that’s the case, it’s actually not too late to take advantage of tax-loss harvesting. While the harvested losses can’t be used to offset 2022 tax liabilities, they can be used for the 2023 calendar year.

The key is to take advantage of this opportunity while it still exists. Markets usually end the year higher: over the last 104 years, markets have had a positive annual return 73% of the time.

Click image to enlarge

Represented by the S&P 500® Index from 1926-2022. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

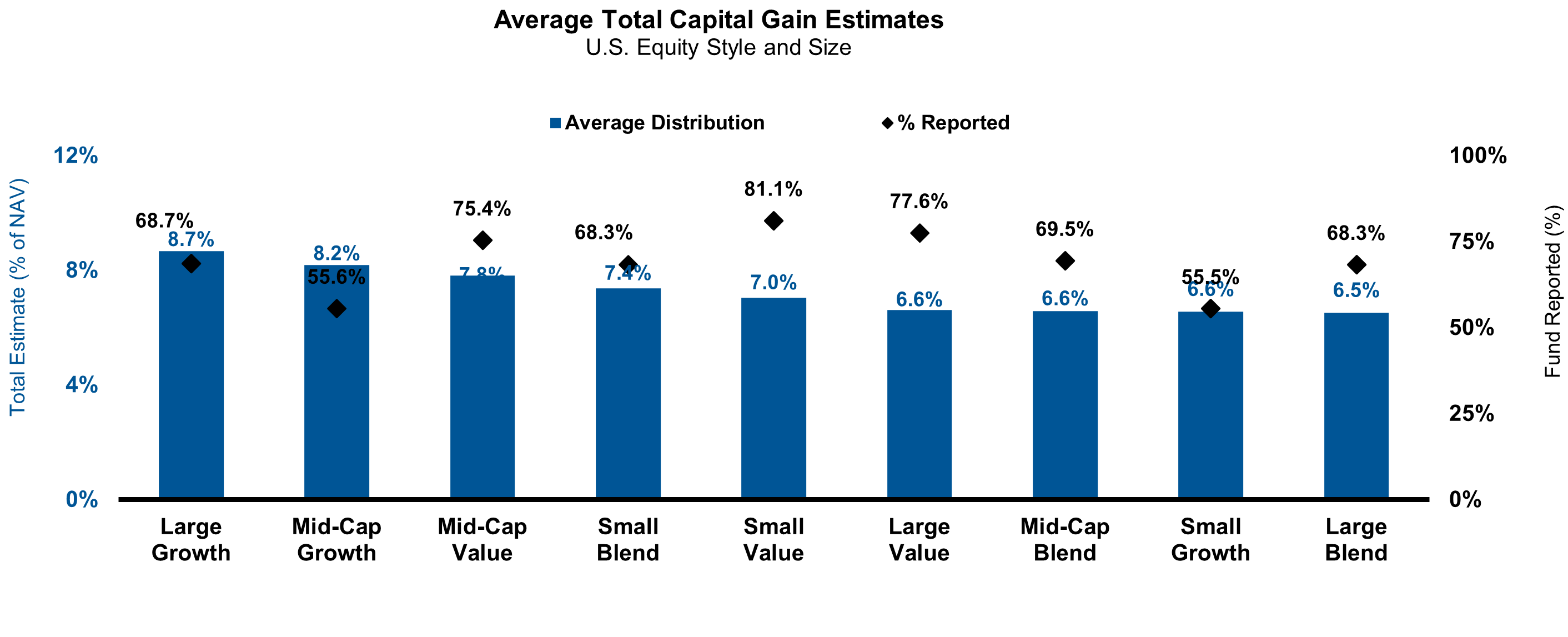

The current tax-loss harvesting opportunity for advisors and investors is not going to last forever, or maybe even not much longer. With US Large Cap stocks down 19.1% in 2022, US Small Cap down 20.4% and international stocks down 14.5% in 20221, there is some but not much runway before those valuable harvestable tax assets evaporate. International markets have already started a moderately strong recovery, so don’t hesitate if tax management is something you want to take advantage of for your clients.

Click image to enlarge

Source: Russell Investments and Morningstar Direct, as of 12/31/2022. Categories based on Morningstar Category Group which includes mutual funds and ETFs (and multiple share classes). The average capital gain distribution % is calculated using the total capital gain distribution and respective pre distribution NAV as reported by Morningstar. % of NAV is calculated as (total capital gain distributions ÷ respective pre distribution NAV).

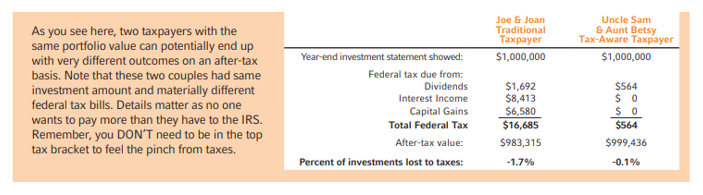

4. 1099 analysis – The cost of those distributions

It’s easy to take for granted the distributions of interest, dividends, and capital gains of the prior year – or any year in most cases. To get right to the point, the tax cost from these distributions can be sizable. The cost impact comes from 1) the size of the overall distributions and 2) the actual tax classification of these distributions.

Let’s start with size, especially since 2022 was a down market year. The average US Equity fund distributed 7% of Net Asset Value (NAV) in capital gains. The kicker, though, is that both dividends and interest income increased in 2022. Dividend yields increased on average by 0.5% and taxable bond interest increased a whopping 3.2%2. As you can see from the table below, this resulted in a pretty hefty overall 2022 tax bill for the average investor.

A comparison of two hypothetical taxpayers:

Click image to enlarge

Source: Russell Investments

The second thing to consider is the tax classifications of the distributions themselves. Only Long-Term Capital Gains and Qualified Dividends receive preferential investment tax treatment. Short-term gains, non-qualified dividends and taxable bond interest are taxed at the ordinary income tax rate. Too often, investors don’t fully understand the tax implications of their investment choices. This results in higher-than-expected and higher-than-necessary tax bills.

You can help your clients and other investors by doing some relatively simple analysis using the Russell Investments 1099 Guide. This guide makes the Form 1099-DIV easier to understand and provides good guidance on how to estimate the tax bills your clients might receive. Contact your Russell Investments representative to request a copy or check out the link below.

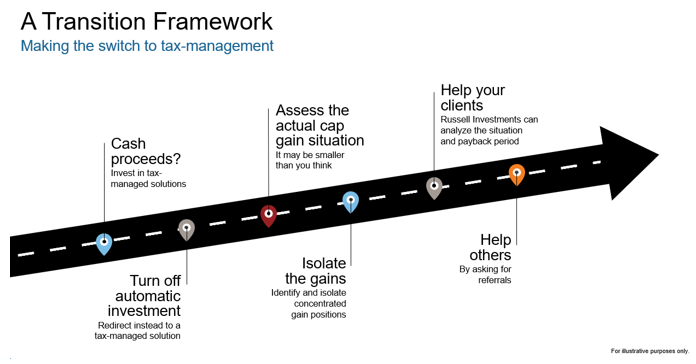

5. Tax transition planning

Get a head start on helping your clients position their portfolios for a better after-tax outcome. What better time than when taxes are freshly on their mind? You have the tax facts and figures for your clients and if you run a 1099 analysis you will also have a good picture of the investor’s tax cost. Why not use this information and this period to steer your clients’ portfolios into a more optimal tax-managed direction?

Start by thinking about the loss harvesting potential if that hasn’t happened yet (or using accumulated losses if loss harvesting was done). The tax liability of making a switch is most likely less than perceived. In addition, doing it now has the immediate benefit of lowering the expected distribution rate of the individual investor’s portfolio for this tax year.

Click image to enlarge

6. Procrastination is not your friend

For most individual investors there are a multitude of ways to save for retirement. Combined, they create a more complete picture of a potential retirement nest egg. Several of these accounts allow investors to save for retirement by providing tax advantages such as long-term tax deferrals or tax-free growth with tax-free withdrawals. But for many investors, as they approach retirement or once they are in it, most assets can be taxable. It’s important to consider the many techniques tax management offers to have these assets grow while limiting the impact of taxes.

Russell Investments offers many tools, calculators, and resources that can help you and your clients grow their retirement savings. This applies to both tax-deferred and taxable assets. We believe a diversified approach to investing, using a consistent philosophy and process, combined with strong planning advice, are the keys to long-term investing success. The many business and investment solutions Russell Investments offers can help you and your clients build a stronger framework for retirement asset growth and increase the probability of the investor reaching their goals.

1U.S. Large Cap represented by Russell 1000 Index, U.S. small cap represented by Russell 2000 Index, international stocks represented by MSCI EAFE Net Index.

2 Source: Bloomberg, S&P