Taxman: There's one for you, nineteen for me ...

George Harrison of the Beatles clearly understood the role that taxes had on his wealth. In his 1969 anti-tax song (Taxman), Harrison was facing a marginal tax rate of 95%! In disbelief, he and fellow Beatles penned one of the greatest anti-tax songs. For those too young or unfamiliar with the song, I encourage you to check it out on iTunes, Pandora, Spotify or wherever you stream or rent your music.

Although the marginal rate for U.S. investors is well below the 95% rate, taxes still play a huge role in determining one’s residual wealth. Taxable investors often ask: When should I care about taxes? Aren’t they only the concerns of the super wealthy like Paul McCartney, Ringo Starr and others in the top brackets? Here’s how you can help your client understand when to be concerned.

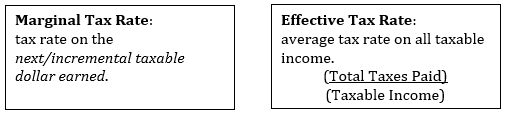

Marginal, average, effective tax rate? Know the differences.

You must know both to make informed investment decisions about tax-smart investing. And don’t forget to include state and/or local taxes when looking at both in any calculation.

Tax-smart investing provides the opportunity to lower the effective tax rates and may help lower one’s marginal tax rate.

Who cares about taxes?

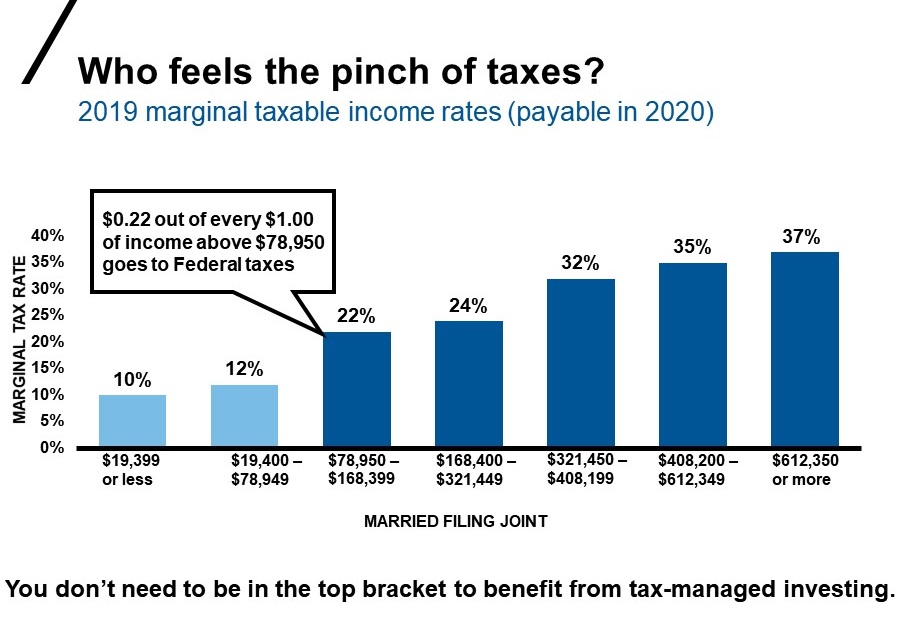

The short answer: It depends. You don’t have to be in the top tax brackets to feel the pinch of the taxman. Consider the marginal tax rates below on taxable income. This rate applies to income such as wages, interest income, short-term capital gains and non-qualified dividends. This includes things like interest income from CDs, savings accounts, earned income, a stock sold with less than a year holding period, etc.

Click image to enlarge

Source: Internal Revenue Service

Your clients (married filing joint status) that have taxable income north of $78,950 are facing a marginal tax headwind of $0.22 out of each incremental $1.00 earned.Their federal marginal tax rate would be 22%.They would keep this federal marginal rate until taxable income crosses $168,400, at which point their marginal rate would increase to 24%. This is the progressive nature of U.S. individual tax rates. Generally, the more you make, the more you pay.

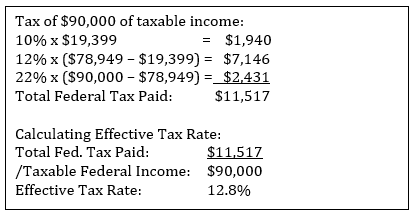

If this couple had federal taxable income of $90,000 that included wages, interest income, short-term capital gains and non-qualified dividends, their effective tax rate would be:

For this couple with $90,000 of taxable income, their marginal tax rate of 22% is materially different than their effective rate of 12.8%.Not knowing the difference or being clear in client discovery can lead to materially different decisions around investment choices, asset location and withdrawal strategies.

The bottom line

When focusing on taxes for your client, remember it’s not necessarily about tax avoidance, but higher ending wealth. Too many investors get hung up on trying to reduce their tax bill that they lose sight of the bigger picture—their long-term financial goal.Working with your client on being tax-smart about their marginal and effective tax rates can make a meaningful difference on achieving successful long-term outcomes.

And if nothing else, be glad that our marginal tax rate is not 95%—as of yet!

If you drive a car - I’ll tax the street;

If you try to sit - I’ll tax your seat;

If you get too cold - I’ll tax the heat;

If you take a walk - I'll tax your feet.

Taxman (George Harrison)