Real assets: Looking for income in all the right places?

Real assets, including real estate and infrastructure, have become an increasingly important component of a multi-asset portfolio. Commercial real estate was first introduced to institutional investment portfolios in the 1970s, and infrastructure earned a place across investor portfolios in the ‘90s, emerging as a stand-alone asset class. While diversification is one of the main drivers for including real assets in a portfolio, we believe there is also another key benefit to maintaining exposure to real assets: sustainable income.

The search for income grows harder

Investors looking for sustainable income sources face greater challenges in accessing them than ever before. These include historically low fixed income yields and extremely accommodative monetary policy undertaken by central banks. Moreover, this easy monetary policy environment will likely keep yields on government bonds in the zero (or close to it) range for years to come.

In August, the U.S. Federal Reserve (the Fed) announced an update to its approach on inflation. After generally falling short of its 2% inflation target set back in 2012, the Fed declared it would switch to an average inflation target of 2%. In a nutshell, this change means that the central bank is willing to allow inflation to run above 2% in the future, in order to make up for prior periods where it ran below 2%. To accomplish this, the Fed may be slower to hike rates than in the past—meaning borrowing costs could stay lower for longer.

What does this mean in the context of a portfolio? Simply put, lower interest rates suggest fixed income returns are likely to be less going forward. In addition, investors seeking sustainable income will also need their income stream to last longer, in order to offset longevity risk.

Amid this backdrop, we believe that real assets—specifically, infrastructure and real estate—deserve to be considered as integral components of portfolios for investors where income is the desired outcome.

Income generation in real assets

In both core real estate and infrastructure strategies, a significant proportion of the long-term total return is derived from current income generated by the underlying assets.

In the case of real estate, the income stream is derived from contractual rent payments associated with tenant leases. Over time, the income stream may increase by either natural organic growth or value-added improvements to individual properties, such as refurbishment and technological / environmental upgrades. For infrastructure, the income stream is associated with long-duration assets that exhibit predictable and resilient cash flows. The resiliency of cash flows attached to infrastructure assets can be attributed to the following: essential nature of the service provided, structural growth, high barriers to entry and strong pricing power. Similar to real estate, infrastructure asset income streams grow over time due to increasing volumes—i.e., increased traffic on a toll road—and operational improvements designed to enhance revenues—such as shopping and dining facilities within airports, etc.

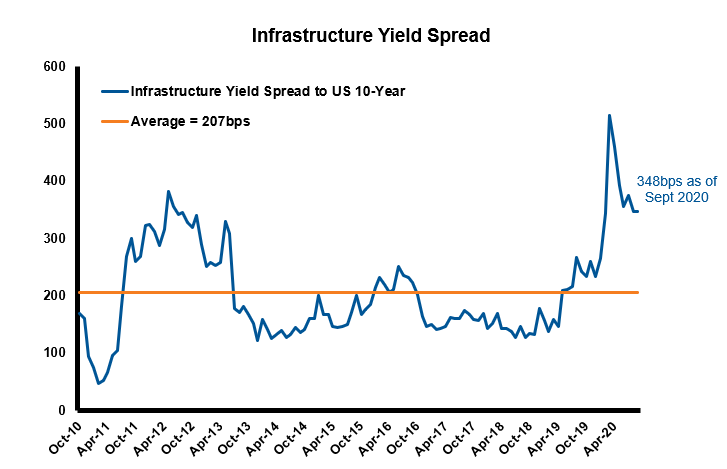

The enhanced income-generating characteristics of infrastructure and real estate investments over the past decade, relative to government bonds, is highlighted in the charts below. These charts show the spread of their respective dividend yields relative to U.S. 10-year Treasury bond yields over the 10-year period ending Sept. 30, 2020.

In the case of infrastructure, the average spread to U.S. 10-year bond yields over the 10-year period is 2.07%. As of Sept. 30, 2020, it is 3.48%.

Click image to enlarge

Source: S&P Global Infrastructure Index, U.S. generic government 10-year bond yield index. Basis points (bps) are a measure of interest rates or percentages. 1 basis point is 1/100 of 1% or 0.01%. 10 years as of September 30, 2020.

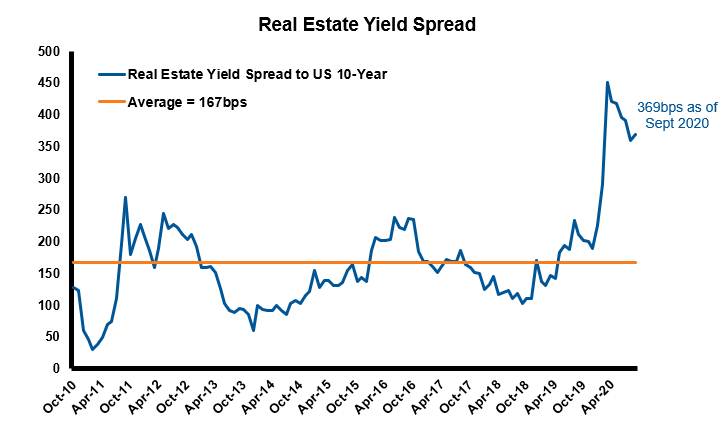

In the case of real estate, the average spread to U.S. 10-year bond yields over this same period is 1.67%. As of Sept. 30, 2020, it is 3.69%.

As the charts clearly demonstrate, both infrastructure and real estate provided a superior level of income relative to government bonds in the past 10 years—a performance which we believe is likely to continue this decade.

Click image to enlarge

Source: FTSE EPRA/Nareit Global Real Estate Index, U.S. generic government 10-year bond yield index. Basis points (bps) are a measure of interest rates or percentages. 1 basis point is 1/100 of 1% or 0.01%. 10 years as of September 30, 2020.

Maintaining purchasing power

There is also another key benefit that we believe real assets provide, relative to government bonds: protection against inflation. Why?

This is because inflation negatively impacts the real level of income (bond yield minus inflation) associated with bonds. In contrast, real assets, due to their unique characteristics, provide investors with an income stream that is generally protected from the impacts of rising inflation—good news due to the importance of income sustainability. We believe this trait will serve investors well in the coming years, given the potential for inflationary forces, primarily due to the massive amounts of fiscal and monetary stimulus that governments and central banks have injected into the global economy in light of the COVID-19-driven recession.

Infrastructure

Most infrastructure assets have an explicit link to inflation through regulation, concession agreements or contracts. This is also a reflection of the fact that, as previously noted, many infrastructure assets operate in monopoly-like competitive positions and enjoy inelastic demand patterns. Namely, they can increase prices without destroying demand.

Real estate

Real estate has been identified as having a long-term relationship with inflation. Over the long term, real estate may provide some protection against inflation, because real estate revenue—which is derived from periodically resetting contractual rental payments—will adjust to changing external market conditions, such as rising price levels. Furthermore, in an inflationary environment, the replacement cost of real estate increases, therefore boosting the value of existing buildings. Replacement cost is the final cost to re-build at current market prices, and incorporates such factors as land value, labor and materials—i.e., lumber and steel.

The bottom line

In the current economic and financial market environment, we believe increased allocations toward real estate and infrastructure may be potentially beneficial. Aside from their attractive income characteristics and their ability to provide a degree of inflation protection, we also see many other potential ancillary benefits, including:

- Portfolio diversification

- Attractive valuations, relative to global equities

- Excess return generation (alpha) through active management

- Exposure to structural themes that will likely play an increasingly important role in the 21st century economy—i.e., growth in infrastructure spending, increased data usage, e-commerce, logistics and renewable energy sources

Many investors are increasingly seeking investments that have the potential to provide superior and sustainable levels of income relative to traditional fixed income investments. In an environment characterized by both low-to-negative government bond yields and unprecedented monetary and fiscal stimulus, we expect the cash flows associated with real asset income streams to become even more sought-after.