Considerations when changing a fund manager

How do you know when to fire your fund manager? This publication outlines Russell Investments’ process when changing fund managers.

Imagine that three months ago you invested $50,000 of your retirement savings in the Fabulous Returns fund offered by Fantastic Asset Management1. The returns from the fund over the last two years had indeed been fabulous, and a lot of your friends have now also invested.

Sitting on the commute to work one morning, you notice an article when scrolling through the news on your phone. The article discusses the recent departure of the Chief Investment Officer from Fantastic Asset Management, who has left to form her own boutique fund management firm.

The Managing Director of Fantastic is quoted saying “we have a strong team here at Fantastic and are confident the remaining staff will do a terrific job going forward.” He adds, “we have also already begun the process of hiring a new Chief Investment Officer. We hope to have the position filled within the next three months.”

“Three months!” you think - “what will happen to my money in the meantime?” Two weeks later, you read another article about Fantastic Asset Management. This time you read that three of the senior portfolio managers have also resigned. They are leaving to join their old boss at her new firm.

By now you are getting a little worried. What do these departures mean for the future performance of the Fabulous Returns fund? Should you pull the plug now and move your money? Or should you sit tight? Fantastic has been in the business for over 50 years and the recent returns have been pretty good, but should you rely solely on past performance?

Then there are the costs to think about. If you pull your money from Fantastic, there may be a cost to exit. Is it possible that buying and selling funds like this might compromise your tax position?

What about finding a new fund manager? You took six months of research to get enough information about Fantastic to hire them. There might also be some entry fees to buy into a new fund. These would make the transaction even more expensive.

Finally, if you pull your money out now, what will you do with it while you figure out what to do next? What happens if the markets move upwards while you are sitting on the side-lines?

You could leave your money where it is while you think about it. But then you run the risk that Fantastic’s new team will mess up.

So, just how much will it cost to switch managers? Even if the new manager is better, how long will it take to recoup those costs?

There are costs to consider!

Your thinking so far has been pretty good. When thinking about switching fund managers, you do need to consider:

- The costs of terminating

- The search costs of finding a new manager

- The costs of switching

- The potential for missing market movements

Are the potential benefits of the switch likely to outweigh the costs?

Data to inform the prior considerations can be hard to come by. In most cases you won’t even know it is time to consider the issues listed above. Fund managers are unlikely to contact you with news about key staff departures, after the fact you were just lucky that you noticed that article. Maybe you don’t normally even read the finance section!

Russell Investments answer

Russell Investments continually monitor the managers and are immediately aware of problems like key staff leaving. We then consider the costs and benefits of changing managers and make the appropriate judgements on whether a change is justified. We are also up to date on potential replacement managers, so the change can be made quickly if necessary.

The product structures used in Russell Investments Funds’ mean that the managers do not actually have the money – they merely advise what to buy and sell. The money is actually looked after by an independent custodian. This provides a good safety mechanism for the Funds, because it means that terminating a manager is as simple as telling them they are no longer needed – and a new manager is hired to advise. Because money is not redeemed, there are no capital gains tax implications. Transition costs are minimised.

In short, firing a manager can be a complex and costly exercise. There is a lot to consider and the information needed is not always easily available. Fortunately, there are solutions – Russell Investments can remove most of this complexity and give you, the investor, a peace of mind that your money is well managed.

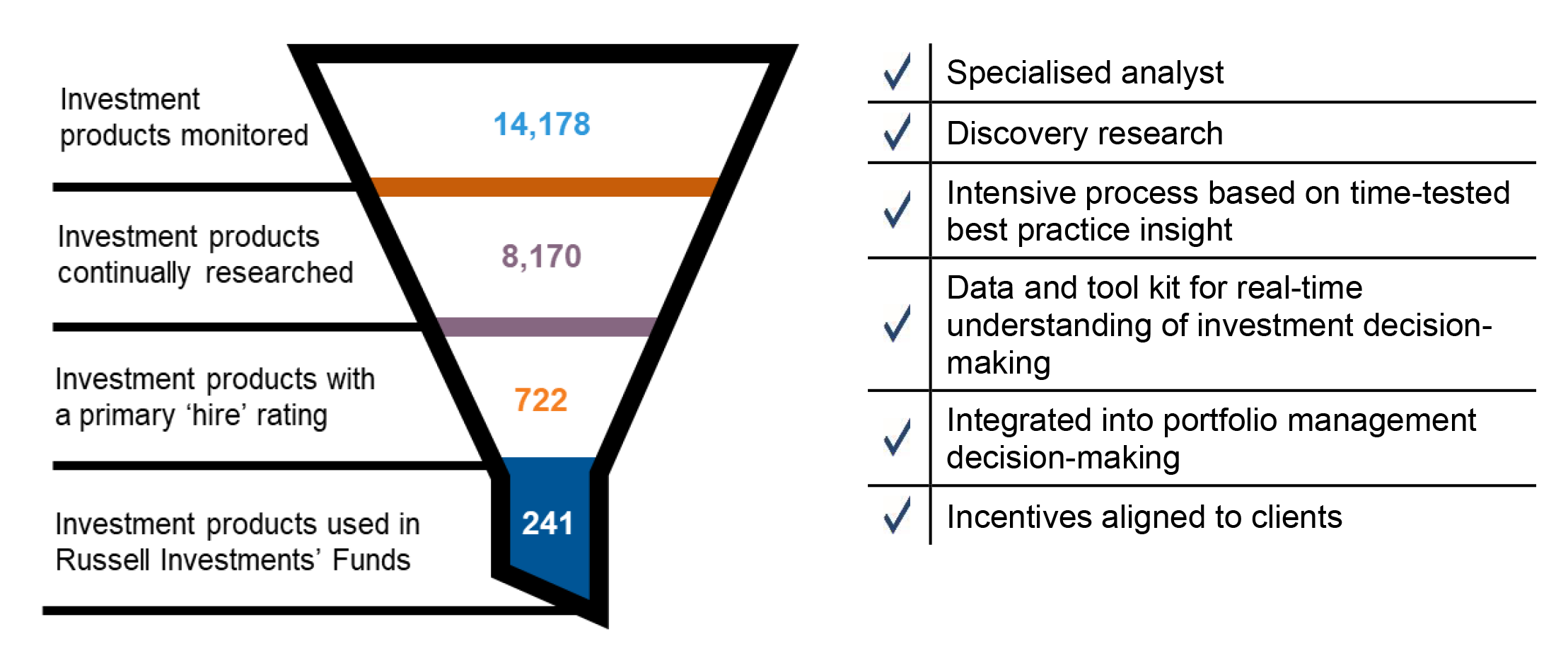

Manager research in Russell Investments2

For more information on Russell Investments manager research process please visit: https://russellinvestments.com/nz/about-us/our-investment-approach

1 Fantastic Asset Management is a fictional entity and the Fabulous Returns Fund is a hypothetical example.

2 Data as of 31 March 2020