When it comes to fixed income, time is on your side. And so is the Fed.

As a professional bond manager glued to a screen watching prices every day, it's hard to fathom that just a few weeks ago when March began corporate bond spreads were below historical averages¹. Flash forward, through what seemed like an eternity at the desk (or home office!), and those spreads have rocketed higher than any levels we've seen, excluding the months immediately following the collapse of Lehman Brothers. The pace of the one-month rise in spreads was faster than any the market has ever seen, including the Global Financial Crisis. We've gone from ho-hum in the bond market to mayhem, in no time. Thankfully, the immutable power of time—with an assist from the U.S. Federal Reserve (the Fed)—is what investors can expect to restore order to the corporate bond markets and bring some compelling returns back to their portfolios.

Most of you probably know and expect that most of your bond returns come from yield or income rather than from price appreciation. And in most instances, this holds true. But yield is a return that is generated over time. Yields on corporate bonds have gone up and so prices have gone down. That price effect on returns was immediate. You will see it in quarter-end performance numbers. But rejoice. Yields have gone up². There was just no time to reap the benefits of this in the first quarter.

Looking forward, the combination of higher yields and more time provides a significant tailwind for corporate bonds. It is just math. With a higher-running yield, spreads now have to widen more and/or faster for price losses to overcome the large yield advantage that comes from holding credit. The everyday physics analogy is the rubber band on a slingshot. You can pull it back quickly and easily at first, but the farther away from center you go, the more force is required pull it farther. Eventually, the band overcomes your attempts at force and snaps back.

Of course, when it comes to bonds, we aren't dealing in physical forces, but the concept is similar. Only in the case of bonds, certainty is the force that ultimately causes that snap-back in spread and prices. And that certainty is brought about by time. Bonds have a maturity date and as those dates get closer and financial conditions become clearer, we learn who is going to default—breaking the rubber band as it were—and who likely isn't, resulting in that sharp snap-back.

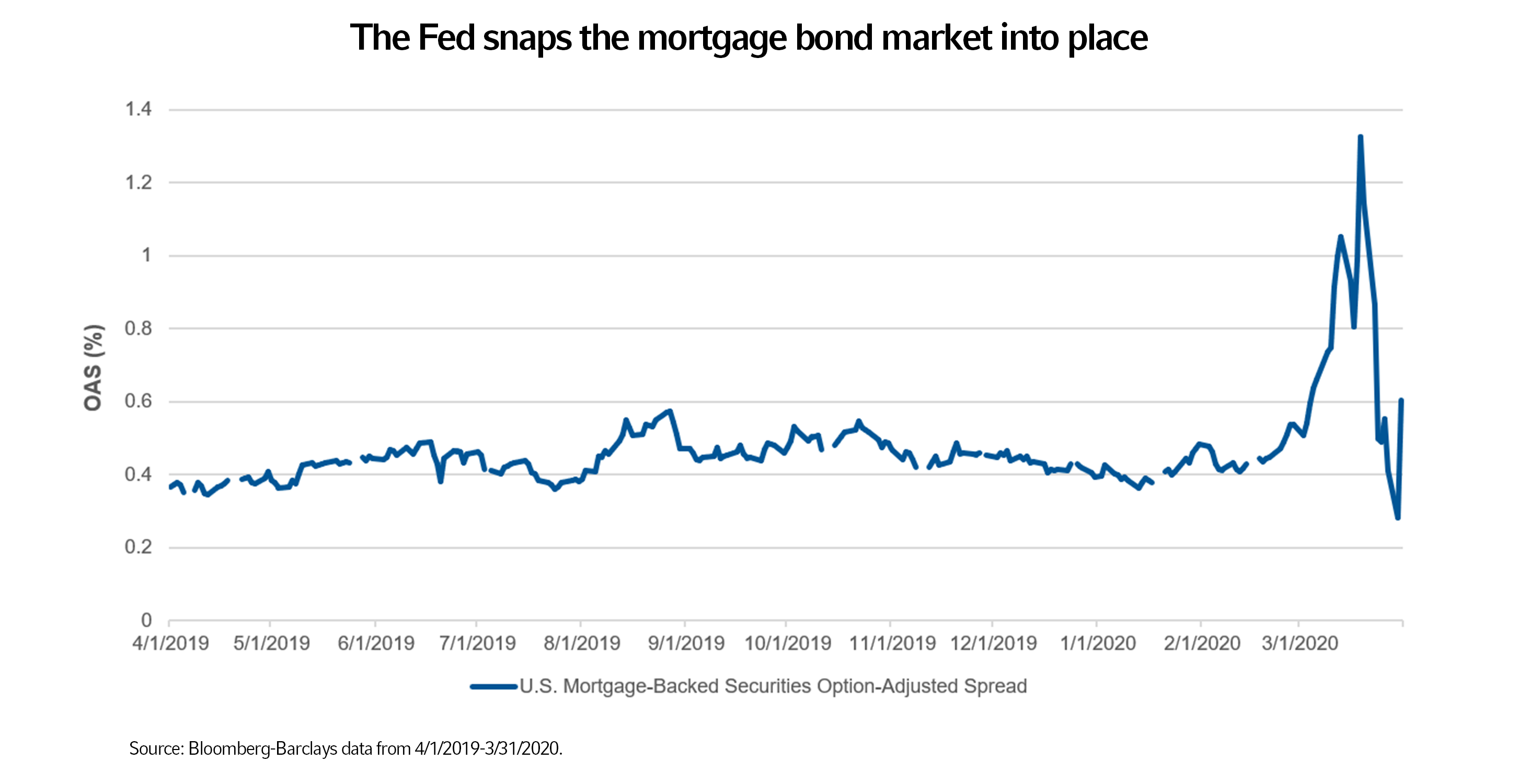

Now, you're all probably wondering just how many rubber bands are going to break. So am I. So is the rest of the market. That's a big part of why nearly half the high yield market is trading at distressed levels³. Here we can take comfort in two things: the Fed and history. The Fed, in concert with the Treasury department, has been given some powerful new tools to both stabilize trading and improve companies' ability to pay. While not yet live, the Fed has been given the capital to buy investment-grade corporate debt outright, which is perhaps the most credit-positive tool in their arsenal right now. For a picture of just how powerful a force that can be, take a look at what the broad policy announcement and implementation did for spreads in mortgage-backed securities, where the Fed was able to act more quickly and with fewer limitations.

The Fed snaps the mortgage bond market into place

Source: Bloomberg data from 4/1/2019-3/31/2020.

Source: Bloomberg data from 4/1/2019-3/31/2020.

Importantly, lending is not limited to just the investment-grade market. Through a variety of programs at both the Fed and the Treasury, below-investment-grade companies will be able to access loans at rates well below what the current market might charge, allowing many, if not most, to continue to rollover debts and survive, even with the sudden stop in revenue. In addition, investment-grade banks will now possess the flexibility to borrow from the Fed and lend on at market-driven rates. There are conditions in some instances, and more domestic business are strongly favored in the legislation that passed, but, like the small-cap equity market, U.S. high-yield companies have a greater tendency to be domestic businesses than the larger investment-grade portion of the market.

There will, however, be companies that fall through the cracks. Markets may not be perfectly rational, but we don't get to spreads this high without legitimate fundamental issues. Spreads this high have always been followed by a jump in defaults. But that’s okay. With spreads this wide, defaults have never been so bad as to eat through all the yield and price appreciation that come with the combination of greater certainty and a little time holding all those bonds that aren't going to default. Unless, of course, you wish to utter the oft-regrettable phrase, “This time is different.”

This leads us to the brass-tax math of it all, and perhaps I've buried the lede long enough. After the late March rally, U.S. high-yield corporate spreads closed the month just back under 9%. According to J.P Morgan data for the last 25 years, we have seen spreads at-or-above 9% a total of 25 times⁴. In all 25 of those 25 instances, the high-yield corporate market produced a positive return over the following year with an average return of 34.7%—a high of 61.4% and low of 0.5%. If the low number is too frighteningly close to just breaking even, consider that the lowest two-year cumulative return was 10.0%. Oh, and the average two-year cumulative return… 55.3%! Such is the power of time and the math of bonds.

It’s been a while since we’ve been able to get off the desk and pound the table about the investment opportunity in credit. But now is finally one of those times.