Are your clients worried about a market crash? A checklist for survival

It's the end of the world!

Well, it is if you believe what you read on some websites and some people on YouTube.

The other day I was sharing stories with an advisor on what was happening in the markets, what people are worried about, and the predictions made by various investment pundits on the internet.

The topics ranged from:

- The Bank of Canada and the U.S. Federal Reserve (Fed) are going to keep raising rates, and that will be painful for many investors.

- China's currency is going to take over from the U.S. dollar.

- The current volatility is the start of a massive crash.

- The global economy in going into a recession.

- The housing market is going to crash.

- There will be a continuous supply shortage.

The list of concerns could go on and on. Whether or not any of them come true, we all know that once investors let their emotions rule their investment strategy, all is lost. As we have noted time and time again, much of the value that an advisor provides their clients is preventing them from making the behavioral mistakes that can harm their portfolio.

Still, when markets are volatile, investors may not be soothed by the knowledge that markets go up 73% of the time1 or that they generally rebound – and rather quickly at that – from any downturn. They’re convinced that this time it’s different.

If this belief were actually true, then we should all begin to worry about other aspects of our life.

So, let's suppose we are on the brink of an apocalypse and the subsequent hardship that would bring. Here are three checklist items to prepare.

Water — There are three main methods of making water safe to drink:

- Boiling (water will need to be at a full, rolling boil for at least 5 minutes)

- Chemical purifiers

- Store-bought charcoal or ceramic filters

Food — You will have to find your own sources of sustenance:

- Trapping

- Hunting

- Foraging

Shelter — Crucial for keeping you warm and concealing you from predators. Here are a few tips to build your camp.

- Avoid anywhere the ground is damp

- Avoid mountaintops and open ridges where you are exposed to cold winds

- Avoid being in the bottom of narrow valleys which are colder at night

- Avoid ravines or washes where water runs when it rains.

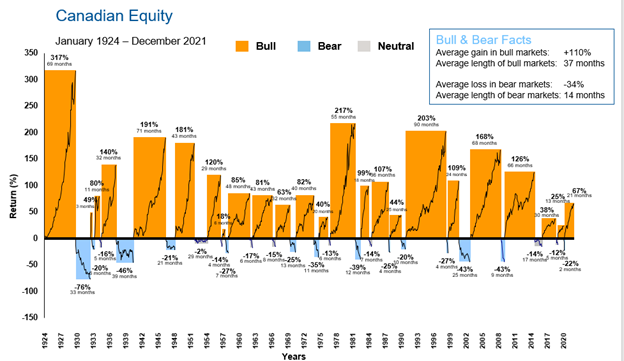

When you look at this list, a market crash seems a lot more survivable, doesn't it? That's because it is. Markets have had significant downturns in the past and as the chart below shows, they always bounce back eventually.

Click image to enlarge

Sources: Canadian Institute of Actuaries, BNY Mellon, Refinitiv DataStream, Russell Investments. Note: Returns prior to 1957 are based on the Report on Canadian Economic Statistics, June 2009, from the Canadian Institute of Actuaries. Returns 1957 to current are based on total return of the S&P/TSX Composite Index. Indexes and/or benchmarks are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. As of December 2021.

Just like you can prepare for an apocalypse, you can help your clients prepare for a potential market crash. When it comes to investing, there are three things that are in our control: Taxes, Asset Allocation, and the investment plan.

- Taxes

There is a common myth that if the markets are down, the tax bill on investments will be lower. That’s not necessarily the case. Distributions CAN happen in both up markets and down markets. For example, if a fund has faced selling pressure from other investors or the fund changed its investment approach – it may have to pay out realized gains to shareholders. As well, no matter what the broader market does, some securities will gain and some will lose.

Not many people like to pay more taxes than they have to. You, the advisor, can help your clients minimize the impact of taxes on their portfolios. One common strategy popular at the end of the year is tax-loss harvesting. We like to call it “tax asset creation.” That’s because those tax losses can be carried forward over three years to offset potential future capital gains. Productive tax-loss harvesting could make a big difference in maximizing after-tax returns for taxable investors.

- Asset Allocation

If realtors can say location, location, location, financial professionals should use diversify, diversify, diversify as our tag line.

We all know we should be doing it, but how many practice it? It’s probably fair to assume that most investors have a home country bias in their portfolios. After all, we all feel more comfortable with what is familiar to us. For example, Canada represents 3.5% of the MSCI World Index2, but our analysis of advisor books over the years has shown that between 60-75% of most investor portfolios are in Canadian securities. That makes them vulnerable to any news that specifically affects the country or its dominant industries.

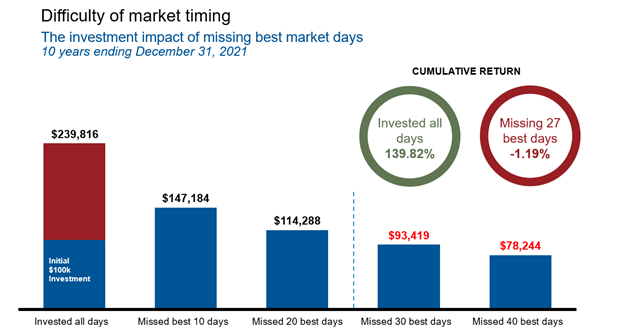

No matter what happens, diversification among asset classes and regions can help smooth out the ride. As we say, a smooth ride is an investable ride: clients are more likely to remain in the markets if their portfolios are less volatile. If they can't deal with the volatility, they might step back from the market. Then they might miss some of the best days, and as the next chart shows, you don’t want to miss the best days. The thing is – we never know when it will be a good day or a bad day in the markets. Diversification can help keep your clients invested so that they don’t miss any of the good days, while the bad days are potentially less bad.

Click image to enlarge

Source: Morningstar. In CAD. Returns based on S&P/TSX Composite Index, for 10-year period ending December 31, 2021. For illustrative purposes only. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

Let us help check your client’s diversification with a proposal or an analysis.

Contact us for more information.

- Build a Robust Investment Plan

A good investment plan requires a lot of work. It includes a robust discovery process and the selection of investments that align to your client's needs, goals and circumstances, then continues with regular reviews. And your services can encompass anything from succession planning to tax planning to the best way of leaving a legacy. But as you already know, the best investment plans can withstand the ebbs and flows of the market. That is the value you bring to your clients. Teach them about everything that you do for them, they might be unaware.

Let them know that their plan is about mapping outcomes for life.

They will have some bumps in the road and more bumps will come, but keep them focused on the outcome, and remember why they are invested. Remind your clients that the key to successful investing is to start as early as possible, be patient, and stick to their plan. As Warren Buffett says” someone’s sitting in the shade today, because someone planted a tree a long time ago.”

As always, let us know how we can help.

1 Source: Russell Investments. Represented by the S&P/TSX Composite Index from January 1, 1920 to December 31, 2021.

2 https://www.msci.com/documents/10199/178e6643-6ae6-47b9-82be-e1fc565ededb