Coronavirus update: Policymakers strike back

Concern over the acceleration of new coronavirus outbreaks outside of China caused global financial markets to sell off aggressively last week. We do not claim to have any edge or unique ability to forecast the progression of this outbreak. Furthermore, leading medical experts have told us that such an exercise is effectively impossible. What we do know is that the short-term impact to global supply chains, travel, tourism and global economic and earnings growth are likely to be large. But this area of analysis amongst economists and investment strategists is both very competitive and very often lacking in conviction—remember, no one has a good forecasting model for the underlying catalyst of this selloff, the virus.

There were two notable, positive developments over the weekend, however, that are worth discussing:

- Stronger signals from fiscal and monetary authorities that stimulus is in the pipeline.

- Evidence that market psychology entered a fearful state at the end of last week.

Will central banks take action?

Last Friday, U.S. Federal Reserve (the Fed) Chair Jerome Powell, published an emergency statement saying, “We will use our tools and act as appropriate to support the economy.” That language is about as direct as you can hope to get from the U.S. central bank that a rate cut is imminent. Our probabilities have been skewed towards the Fed cutting interest rates for about a week, and we now expect them to move by 50 basis points at or before their next meeting on March 18.

Respectfully, we don’t think the Fed can model the economic consequences of this outbreak better than anyone else. Inflation is below the Fed’s 2% objective. And not acting into current pricing would tighten financial conditions—a risk not worth taking.

Bank of Japan (BoJ) Governor Kuroda also made an emergency statement over the weekend that they “will strive to stabilize markets and offer sufficient liquidity via market operations and asset purchases.” While the BoJ has less room to ease than the Fed, the possibility of more exchange-traded fund (ETF) purchases could support asset prices in the region.

Finally, President Xi from China has stated that China will not lower its economic growth target for this year, that fiscal policy will become more “proactive” and that monetary policy would be “flexible.” The timely, material and global nature of these announcements are an important ballast against the spread to the virus.

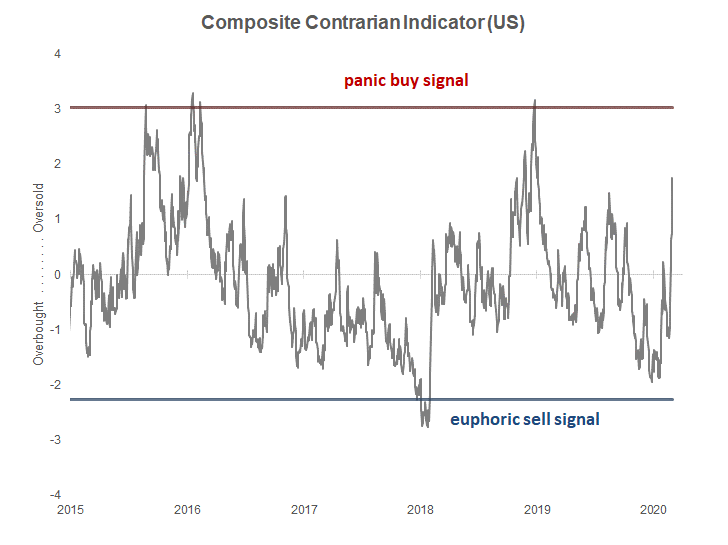

Click image to enlarge

Source: Russell Investments. Data as of Feb. 28, 2020.

Tactically, we have been tracking the market psychology around this selloff, looking for evidence that sentiment might crater into an extreme panicked state. Last Friday, our composite contrarian indicator—which aggregates roughly a dozen technical, positioning and survey indicators—flagged for the first time that global equity markets had entered a state of fear. However, this signal is not showing a full-blown investor panic, like what we saw in late 2018.