From black to blue: Moving the ESG conversation beyond carbon and onto water

When it comes to ESG, a great deal of research has focused on carbon—how it can be measured, managed and invested in for tomorrow’s green economy. But there is more to the E in ESG than carbon. What’s next in the environmental investing space? For us, it’s water.

Water risks are regional, multi-dimensional and very distinct from carbon. Understanding water-related risks is a vital component of evaluating the long-term sustainability risks and opportunities of an investment portfolio. However, the tools for properly assessing water-related issues systematically are still developing. The existing frameworks and data sets for water are, in our view, insufficient and inhibit investors from converting insights into meaningful action.

Four key considerations for investors seeking to incorporate water into their portfolio

When it comes to ESG investing, the current state of water data is a bit shallow, in terms of both quality and quantity. Therefore, we’ve identified four key considerations for investors seeking to incorporate water into an investment portfolio:

Consideration #1: Data reporting is low

- Water withdrawal is the total amount of water withdrawn from a surface water or groundwater source. For companies in the global large-cap universe, water withdrawal coverage is at only 43%. In industries where water is a material issue, such as chemicals, metal & mining and semiconductors, water withdrawal coverage tends to be higher—as high as 80%.1

- Water consumptionis the portion of the withdrawn water permanently lost from its source. This water is no longer available because it evaporated, got transpired or used by plants, or was consumed by people or livestock. Water consumption is a material issue for only a few industries, so data on water consumption is lower than data on water withdrawal, at roughly 16% for the MSCI ACWI Index.

- Water is not necessarily a material issue for all companies. And coverage at the universe level is low. So the reasonableness of producing a portfolio-wide water metric is less clear than in the case of carbon footprint.

- We have found that there are many industries where water is a financially material issue, but companies are still not disclosing. This suggests ample opportunities to engage with companies about improving water-related disclosures.

Consideration #2: Water usage is highly concentrated

- Water usage, both in terms of withdrawal and consumption, is highly concentrated in a handful of companies. This is similar to what is observed in carbon data, where a small number of companies make up a significant share of a portfolio’s aggregate carbon emissions.

- In the case of water withdrawal, this feature is even more extreme, with 10% of companies contributing 91% of the portfolio’s aggregate water withdrawal.2

- The highest water usage is found in the utilities, materials and energy sectors.

Consideration #3: The market is highly exposed to water-stressed regions

- When it comes to understanding water risks, a regional lens is critical. In the case of carbon, if one country dramatically reduces emissions while another dramatically increases emissions, these two actions roughly offset. The aggregate amount of carbon emitted globally is unchanged, because carbon emissions are a global issue. Water, on the other hand, is a regional issue. One unit of water withdrawn in a drought-ridden Morocco is not the same as a unit of water withdrawn in a water-rich corner of Russia.

- Ideally, available data would tell us not just how much water was consumed, but also what percent was in high-stress regions. Unfortunately, the data is not this granular yet. Instead, we proxy for exposure to high-risk regions by looking at companies with more than 20% of operations in high water-risk regions. We find that 71% of the companies in the portfolio meet this criterion, suggesting exposure to regional water risk is significant.3

- There are a lot of companies in high-risk regions, but these are not necessarily high water-users. That’s the relatively good news. The bad news is that there are significant unknown risks in the high-risk regions, because 32% of companies have exposure to high-risk regions and do not disclose water use.4

Consideration #4: Identify forward-looking information and proactive companies

- One piece of forward-looking data that can be considered is a company’s water-related target. Do they have a water-reduction goal they are targeting? Increasingly, these targets are being reported in corporate disclosures where water is a material part of a company’s business.

- Where water is a material issue, approximately 29% of companies by name count have set water-use targets.5 We believe companies going to the effort to set a water-reduction target are making a higher commitment to manage water use than peers with comparable water use who have not.

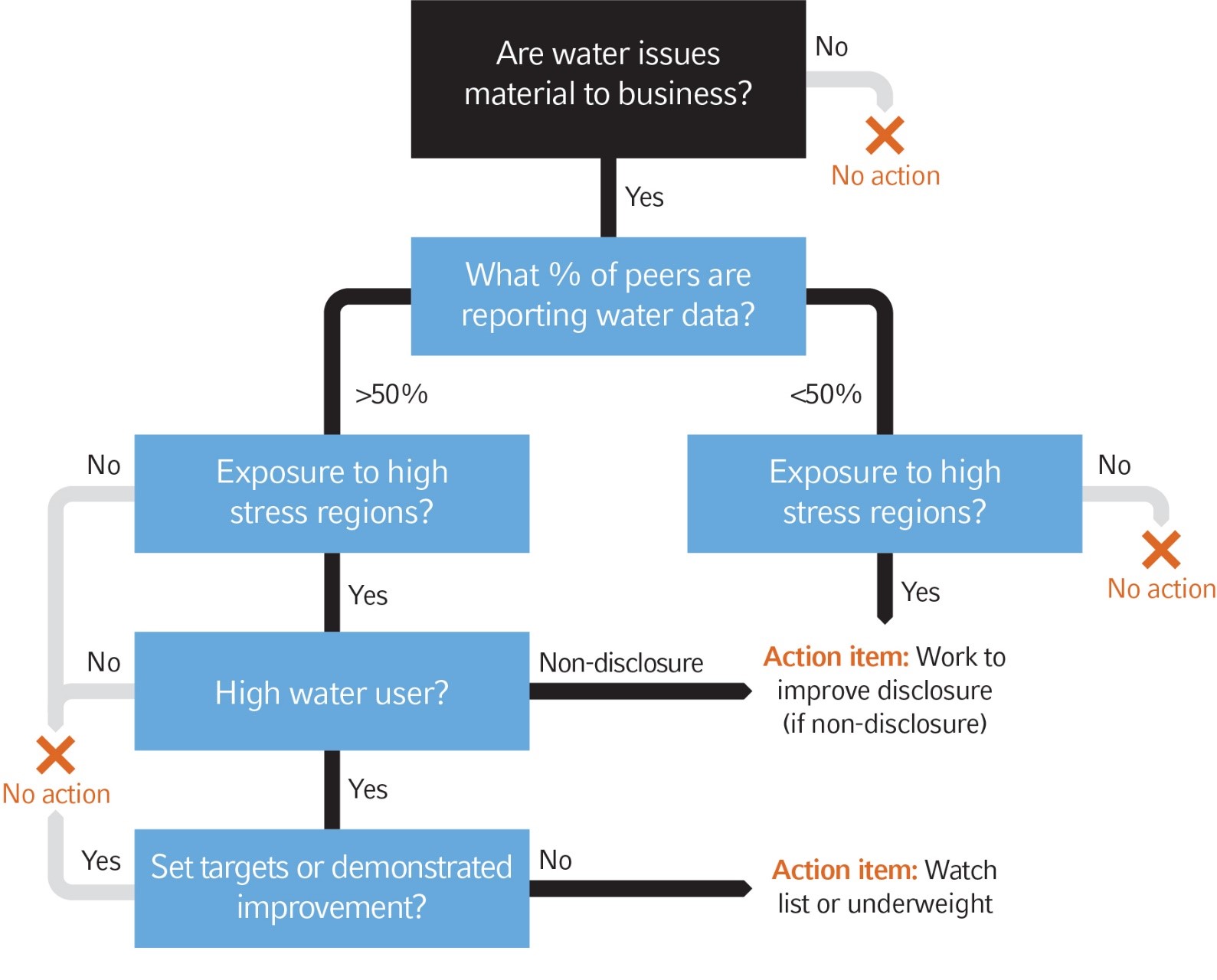

Turning research into action: A decision-tree approach

The most useful tool we have found for combining the myriad of considerations into a simple actionable framework is a decision-tree approach. This decision tree can be used to sort companies into three buckets: those targeted for improved water disclosure, those added to a water watchlist or underweighted and finally, those where no water-related action is necessary.

Decision-tree approach to sorting companies in the portfolio

Click image to enlarge

Source: Russell Investments, for illustrative purposes only.

Armed with this framework as a starting point, we have identified the following:

Better disclosure is the first step

Getting better disclosure for at least the high-stakes companies is going to be the first step to accurately assessing water-related risks in a portfolio. We propose a simple rule for identifying high-stakes non-disclosers: Look at materiality by industry and exposure to high-stress regions.

Avoid penalizing companies who are industry leaders

During this early phase of water data incorporation, it is critically important to avoid penalizing companies who are industry leaders and have started disclosing, even though their peers have not. For example, if we underweight a company who is a large water user even though they are one of only a handful of companies that is reporting, we have effectively punished a company for taking the proactive step of disclosing water data.

Identify the sources of highest known risk in the portfolio

The sources of highest known risk in the portfolio can be identified by looking at the intersection of material industries and high water-users. For investors looking to minimize exposure to water-related risks, these are potential companies for underweighting or adding to a watch list to monitor more closely.

Incorporate positive attributes and forward-looking metrics

The goal is to recognize companies that are taking proactive steps to manage water issues and improve water security. Admittedly, poor data makes this a challenging step, but one critical to incorporating opportunities and a forward-looking perspective.

The bottom line

As noted in the World Economic Forum’s annual Global Risks Report for 2019, a water crisis has been included in the top five global risks in terms of impact for the past four consecutive years. And when it comes to investing, water is a nuanced topic that requires a thoughtful line of attack. Current data limitations will inhibit investors from converting the insights from these frameworks into action, as many of the methods that have been developed for carbon don’t always work here. A decision-tree approach can help. And finally, as the focus on responsible investing best practices evolves over time, we remain committed to looking forward, anticipating trends and researching new ideas.

1 Source: Russell Investments research, MSCI All-Country World Index. Data as of Sept. 30, 2018.

2 Source: Russell Investments research, MSCI All-Country World Index. Data as of Sept. 30, 2018.

3 Source: Russell Investments research, The Aqueduct Global Maps 2.1 database, 2019. https://www.wri.org/data/aqueduct-global-maps-21-data Retrieved 14 May 2019.

4 Source: Russell Investments and MSCI All-Country World Index. Data as of Sept. 30, 2018.

5 Source: Russell investments, MSCI All-Country World, Index, The Task force on Climate-related Financial Disclosures