Money down the drain?

De-risking at work

The de-risking model is not novel. It has been a key consideration, ever since the Global Financial Crisis, as regulations-and the views on pension risk-have changed. But many plans are reluctant to move out of their growth assets-regardless of what valuation models may say. Or they're reluctant to move to long-duration fixed income assets, when they have strong beliefs that interest rates will rise and potentially devalue fixed income investments. Defined benefit plans that have decided to de-risk are generally implementing some style of de-risking glide path. In most cases this means implementing the conversion of assets to long-duration fixed income over an extended period of time. This includes converting to long-duration fixed income at pre-determined trigger points, based on funded status or market interest rates.Money left on the table

Regardless of the de-risking strategy, we believe many investor and asset managers have historically been nonchalant in the transition of assets to fixed income mandates. This attitude has most often taken the form of lost market exposure: The investor leaves assets uninvested in cash until the new manager invests the cash into a complete fixed income portfolio. But this can often take weeks. This uninvested cash can lose out on investment income relative to yield-rich long-duration credit. As such, plan performance suffers. This yield give-up investors may incur during the transition process will only increase if the yield curve steepens. Indeed, the yield curve is expected to do just that in the near future. This income loss is even greater for riskier assets like high-yield and emerging-market debt. We believe that in a suboptimal approach of giving uninvested cash to a fixed income manager, you should assume that your plan loses about one basis point (bp) of investment income per day. Could be more, could be less, but on average your assets are losing precious income. Most managers take weeks to complete their portfolio and income loss can grow to 15 bps or even higher during the transition period. Apply this income loss to the $1 trillion expected to move to fixed income in the coming years and this lost income could easily be in the billions of dollars.The avoidable loss

The most unfortunate aspect is that nearly all this income loss can be avoided with proper implementation. The apathetic approach - i.e., of giving the current portfolio or cash to the incoming investment manager - does not, in our view, align the interests of the manager with the goals of the investor. Managers are generally afforded performance holidays during the funding process and are not measured or held accountable for the performance outcome during that period. With no emphasis on performance, operational convenience dominates the decision process. Investors will likely experience two primary flaws in a process driven by convenience: We believe the best way to avoid this performance slippage is to employ a specialist to manage the transition of assets from current mandates to new long-duration mandates.- Large cash exposures or investment exposures that do not align with the target portfolio.

- A slower trade velocity, with a potential increase in overall implementation costs. This slower velocity extends the time the investor is uninvested. These flaws may leave valuable basis points on the table and make investment goals harder to reach.

What's the solution?

Experienced investors take steps to ensure that overlay programs are employed to equitize cash balances. However, this strategy often lacks appropriate credit exposure, which is where much of the income is lost.We believe the best way to avoid this performance slippage is to employ a specialist to manage the transition of assets from current mandates to new long-duration mandates. Transition managers function as implementation partners for investors, creating and executing an implementation strategy to minimize the performance impact and to save valuable investment income.

A sea change in defined benefit plan management is currently underway. Corporate treasury departments are focusing more on managing their defined benefit plan costs and risks. And the de-risking process should be a priority. The marketplace will be watching pension managers to see if they continue to let convenience drive the de-risking process. Or will a new era of pension investors-focused on costs and performance outcomes-give birth to a higher standard for implementation?

The numbers

For illustration purposes, here are the hypothetical savings from skilled implementation vs. a suboptimal implementation with an incoming manager:

Exhibit 1: Savings from skilled implementation vs. a suboptimal implementation

Source: Russell Investments. Reflects market conditions in 4th quarter 2018. For illustrative purposes only.

This chart shows the hypothetical savings while transitioning a value of $500 million, but keep in mind that Bloomberg reported $1 trillion of assets would be in motion and that's a lot money down the drain. This begs a final question: How much are plans losing by ignoring fixed income transition management? When the answer is a number this large, the situation demands attention.

Why fixed income transition management makes sense

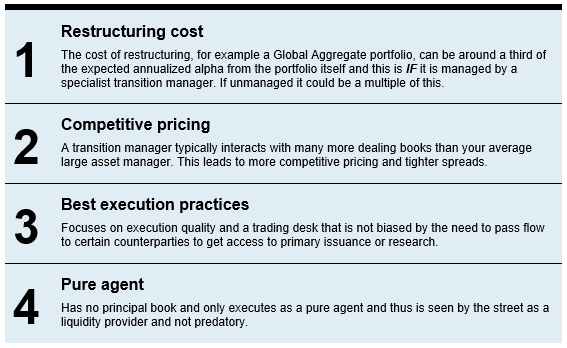

Fixed income lends itself to a specialist approach when making portfolio changes. Here are four reasons to use a transition manager:

To learn more about fixed income transitions, read our paper.2

1 Basak, S., & Chiglinksy, K. (2017). "Pensions May Yank Up to $1 Trillion From Stocks to Trim Risk" Bloomberg. Retrieved from: https://www.bloomberg.com/news/articles/2017-08-28/pensions-seen-yanking-up-to-1-trillion-from-stocks-to-de-risk and Mercer (2018) "European Asset Allocation Survey Report 2018" Retrieved from: https://www.mercer.com/content/dam/mercer/attachments/private/uk-2018-european-asset-allocation-survey-report.pdf

2 Houchin, J. (2017, May). "Fixed income transitions: A specialist approach." Russell Investments. Requestable at: https://russellinvestments.com/us/insights/articles/fixed-income-transitions-a-specialist-approach