Preventive medicine for downside risk

In today's low-return environment, reducing a portfolio's strategic equity allocation can work like preventive medicine, helping lead to better downside risk control.

Okay, I get it. You’re tired of hearing about the low-return environment. It’s persisted for years. And yet, we continue to eke out acceptable returns in spite of recurring forecasts that there’s little juice left to squeeze out of many risk premia.

Right now, investors face a choice between a moderate expected return and exposure to a punishing potential downside outcome. We believe many investors too often tilt toward returns, hoping to achieve higher expected return targets. Meanwhile, that harsh critic called hindsight sits ready to sting those who should have known that markets were due for a fall. That said, positive returns from equity markets and, for that matter, any other exposures that come with considerable downside risk, come in spurts. Capturing those risk premia means not missing out on lumpy gains when they do occur.

For public and corporate pension funds, there’s a general acknowledgement that bad things occur when drawdowns yield negative portfolio returns well below expectations. So let’s focus on a foundational first step—preventive medicine, if you will. Let’s focus here on reducing risk exposure.

|

Preventive medicine – reducing reliance on equity and replacing with less–correlated exposures |

Reducing strategic commitment to equity (Preventive Medicine)

One way to deter oversight risk is to simply outperform a policy benchmark. This may deter oversight risk and help investors avoid undue focus on short–term results. But it does not help the impairment in wealth accumulation that can jeopardize the ability to meet obligations, at least not without subsequent increases in contributions or reductions in benefits to participants. The importance of absolute return is creating an increasing role for dynamic portfolio management at the expense of benchmark–centric allocations to traditionally defined sub–advisor allocations.

We believe the simplest and cheapest way to reduce downside risk from equity exposure is to reduce strategic exposure to equity. For most, aggressive return targets make this a difficult change to enact. The loss of returns that may come from reduced strategic equity allocation must be made up somewhere else.

Here are five places we believe institutional investors should look:

- Conditional exposure to lower–risk, higher Sharpe ratio assets — This can be implemented within an isolated risk–parity mandate such that leverage can create a similar expected return with less risk. Easing of the leverage constraint can allow for financing opportunistic allocation to positive–carry fixed–income positions. With low yields relative to history, entry and exit points are critical and exposures can be managed dynamically.

- Using derivative overlay for capital–efficient alpha generation.

- Conditional exposure to equity risk — Intentional movements into or out of equity—with opposing direction to fixed income—can be managed to generate incremental return, by using the allowable policy range in an opportunistic and loss–aware fashion. Leverage is not required and this approach can generally fit within existing investment policies.

- Dynamic, non–directional exposure to currency or other markets with a long/short portfolio structure.

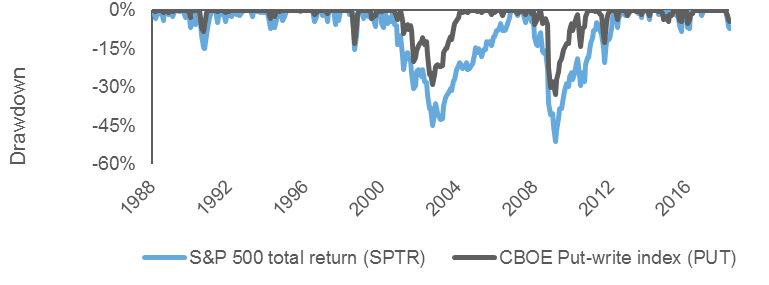

- Diversifying equity exposure to offset a portion of downside with recurring option–writing income. An ongoing strategy is recommended for harvesting the volatility risk premium with a smoother, more diversified return pattern. This is generally accommodated via a fully funded mandate using listed options. At Russell Investments, we focus on U.S. equity markets in this area, due to the liquidity in listed derivatives, but also due to our strong view that the risk–reward trade–off is currently the weakest here, with U.S. equity being more overvalued than its overseas counterparts.PUT (the Cboe S&P 500® PutWrite Index) and BXM (the Cboe S&P 500® BuyWrite Index) are examples of benchmarks useful in gauging performance of a put–write or overwriting mandate. These mandates may deliver an equity–like return pattern over the long–term, with 70% of the volatility and a potential reduction in depth and duration of drawdowns relative to equity, as reflected in S&P 500® Total Return Index.

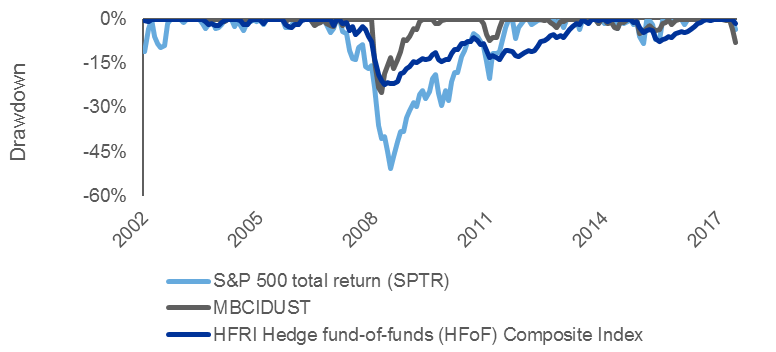

Return patterns can be further modified by hedging residual exposure to the equity market to isolate a pure volatility risk premium. The result here is an attractive return pattern that functions well as a liquid proxy for hedge fund–of–funds (based on the Hedge Fund Research, Inc. Fund–of–Funds Composite Index). MBCIDUST (UBS US Delta Hedged Strangle Index) is a good example of a benchmark useful in gauging performance of a volatility–premium–based alternative beta mandate.

Concluding thoughts

Altering an investment portfolio for better downside risk control is ultimately a joint project, with roles for your board, your investment staff, strategic advisors and niche mandate managers. There are challenges in making investment decisions that trade expected return maximization for the promise of a better outcome in troubled times. Those challenges do not become easier with time, and continued reminders of why we have chosen this route are required along the way. Ultimately, we believe the portfolio outcome is likely to be superior, with a cohesive and integrated approach to mitigating drawdowns, rather than allowing for the emotional comfort that comes with over–reliance on more costly insurance.