Are your clients keeping cash on the sidelines?

We’ve all heard the clichés: The best time to invest is when you have the money to put to work! and It’s not about time-ING the market, it’s about time IN the market! They may seem a bit cheesy, yet they are frequently used. The reason clichés work is that they tend to be true.

All of these phrases can be boiled down to the oldest investing principle in the book: buy low and sell high. Pretty much any graph on behavioural finance can tell you, investors clearly don’t always have a firm grasp of that concept.

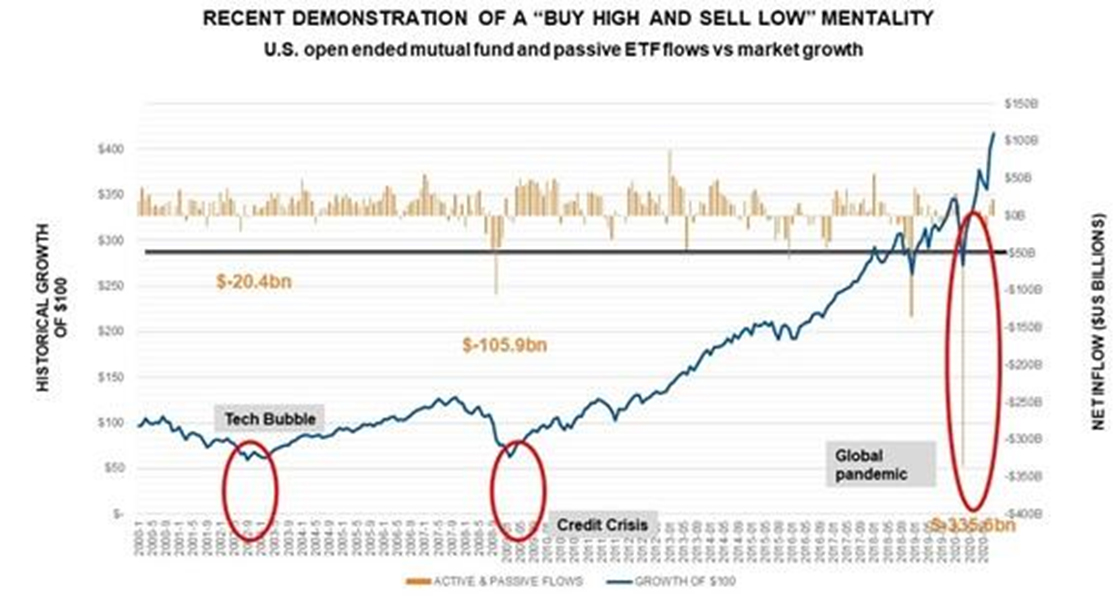

Indeed, our basic human instinct to follow the herd often leads us to buy high and sell low. This was clearly evident at this time last year when financial markets were jolted by the global spread of the COVID-19 pandemic and authorities imposed lockdowns that effectively shuttered large portions of the global economy. As the graph below shows, investors in the US took $335.6 billion out of equities in just a few short weeks. Unfortunately, as markets recovered these cash holdings weren’t re-invested. And worse, many may feel that they have missed the boat and retain their cash holdings – when there are better ways to put your capital to work.

Click image to enlarge

Seeing the flight to cash

Data shown is historical and not an indicator of future results. Sources: Monthly mutual fund, passive ETF flows and Russell 3000® Index, Morningstar, Direct. Blue line shows growth of $100 invested in Russell 3000 Index.

Orange bars indicate monthly

inflows into mutual funds and passive Exchange Traded Funds (ETFs). Data as of December 2020. Index performance is not indicative of the performance of any specific investment. Indexes are not managed and may not be invested in directly.

We also saw many Australian Superannuation Funds with members making switches to cash options after the markets had fallen in March 2020. The Reserve Bank of Australia (RBA) noting that the size of the flows to cash in this time were higher than previous market dislocations – including the global financial crisis1. It was also noted that the switching to cash was driven by members who were generally closer to retirement with larger average balances. Selling to cash after the market had dropped, locking in losses and not participating in the rebound – had material impacts on their retirement savings.

COVID-19 and cash at banks

Outside of investing behaviour, we have also seen some interesting behaviour with Australians and cash.

In addition to switching to cash within super, Australia had experienced a significant increase in bank deposits. From March 2020 to March 2021, Australians increased their cash in the bank by 12%, accounting for an additional $124 billion in additional cash in banks over a one-year period2.

While this is partly attributed to some of the government’s stimulus packages, including early access to super–we believe there are also some behavioural biases at play. The flight to cash, in times of panic, and the sense of security in staying there.

There is some functional use of this cash at banks. For example, roughly half of these cash deposits relate to holdings in mortgage offset accounts, reducing the overall interest payable on a home loan. This has been a good strategy for some, to reduce household debt over time. However, if the fixed interest rate on a mortgage is 2.5%3 and inflation rises to and over 2.5% in the coming years, a homeowner’s offset account may no longer have an effective impact on a home loan in real terms. Advisers can play an important role in helping clients navigate this based on their circumstances.

Is there cash under the mattress?

The interesting story is not just the cash at banks building up, but the physical cash that is accumulating. While tap and go payment methods increased in the early days of the pandemic, the RBA also reported a sharp rise in the demand for banknotes in mid March 2020. The value of banknotes in circulation was up by 17.1% over the year to February 2021, reaching $97.3 billion compared to 5% growth of banknotes in circulation over the previous decade.

The RBA conducted a survey and over 40% of respondents had been using fewer physical cash transactions since the start of the pandemic, while a significant portion of them were also holding more physical cash for precautionary reasons. Which may lead many advisers to check in with their clients to make sure they weren’t doing the same4.

Cash on the sidelines

We expect some of these cash holdings to be used as the economy opens, lockdowns end, employment stabilises and people spend some of these savings on well-earned holidays when we can travel confidently.

But even taking this into consideration, individuals may be holding excess cash in their super, bank accounts, or even at home. There could be a substantial amount of cash on the sidelines that is at risk.

This spells OPPORTUNITY for financial advisers to help their clients make informed decisions about their financial future. Advisers can help clients balance the impacts of investment returns, risks, taxes and inflation, and find a better way to put their capital to work.

How to talk to clients with cash on the sidelines

When it comes to talking to clients with too much cash on the sidelines, everyone has (or should have) their go-to discovery questions.

- What is it for?

- Why do they have it in cash rather than something else?

- What level of risk is appropriate for your situation?

The second question is key, as that is how you can tell if there is an opportunity or not to invest the money. Most client responses can be narrowed down to two key points:

- Cash carries little perceived risk to many investors, while investing in the market can have a downside. People like the idea that cash is inherently safe: no market risk comes with having your cash sitting in the bank.

- Cash is liquid. People like knowing they can access it at the drop of a hat.

Let's address these.

Cash carries low risk

We can start with the obvious: inflation exists. Inflation is the silent killer of cash value. The RBA has a target inflation rate of between 2-3%5, and currently the expected inflation rate is currently 2.1%. This becomes important when we consider the excess cash in banks, when interest rates are so low.

Therefore, if an investor placed their money in a one-year Term Deposit which offers 0.25% p.a. and after adjusting for expected inflation, the real return on cash is -1.8%6 . The investor is effectively paying the bank to store their cash.

To help your clients understand this challenging concept, consider sharing our client-ready resource beware of the hidden cost of cash.

Cash is liquid

That brings us to the second reason many investors hang onto cash: liquidity. This one is simple, yet it is all too often misunderstood by clients. If they have their money in a managed account, managed funds or ETFs, when necessary they can liquidate, and the money can hit their bank accounts within just a few days.

The next time a client is concerned about liquidity, ask them ‘What the odds are that they will need to access their money with less than three days’ notice?’

Summary

Uninvested cash is one of the best opportunities to help clients reach their financial goals and articulate another value add of having a financial adviser. Whether it’s post pandemic stimulus, saving, or personal circumstances such as inheritance or the sale of a home or business, or some other source – an adviser can help design a best game plan for sidelined cash as we emerge from the pandemic.

1 Source: RBA Financial Stability Review April 2021, Box C: What did 2020 reveal about liquidity challenges facing superannuation funds?

2 Source: Australian Prudential Regulation Authority (APRA) – Monthly authorised deposit-taking institutional statistics (June 2021)

3 Source: RBA average three-year fixed rate for homeowner occupier is 2.2%, investor is 2.6% (July 2021).

4 Source: RBA March 2021 Bulletin: Cash demand during COVID-19

5 Source: RBA inflation target, accessed July 2021

6 One-year Term Deposit rate: Retail deposit and investment rates; Banks' term deposits ($10,000) (Source RBA). Current inflation as measured by current Consumer Price Index (CPI) rate of 1.1% as of March 2021 (Source ABS). Expected inflation

as measured by the Australian Break-even 10-year inflation rate as of March 2021 (Source RBA)