Re(de)fining Your Responsible Investment Policy – a strong governance health check

1. Education and Stakeholder Engagement

Begin by educating key stakeholders about the trends, terminology, and practices in the responsible investing landscape, including any fiduciary and legal implications. Gather their views and preferences through surveys, focus groups, existing research, and data analysis. Your investment provider with responsible investing expertise can help facilitate this process.2. Define Organisational Beliefs

Key questions to consider include:

- Do we believe these ESG risk concerns will impact our portfolio from a risk and return perspective?

- Do certain ESG risk factors matter more to us than others? (e.g., instead of divesting from companies that may be unsustainable or have poor business practices, investing or staying invested can allow an investor to influence that company’s behaviour and make it more sustainable)

- What changes need to be made to our policy or investment strategy to reflect our beliefs stated above?

When reviewing your investment policy, consider the following:

- Does it reflect current beliefs and strategies?

- Are goals and targets on track? How well has the policy been implemented?

- Should recent research or peer activity prompt a policy review?

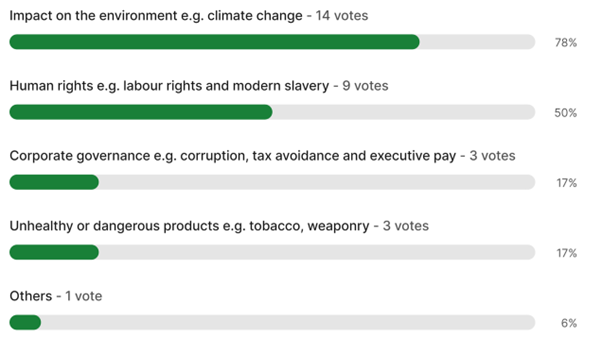

As an example, I recently spoke at the AUSFOG conference1 for Australian Universities, senior finance professionals. When asked about their top two concerns regarding sustainability, the below poll results highlighted what’s important for the audience. If you survey your key stakeholders and senior leaders, what do you expect the outcome to be? If they haven’t been clearly identified or defined, that can be a first step—find out your organisational beliefs and how your mission statement reflects your responsible investing commitment or principles.

3. Implementation Approaches

Once the organisational beliefs and goals are defined and articulated, the next step is to explore and understand various implementation approaches. There has been a growing effort in standardising sustainable financial terms globally, with the UN PRI, CFA Institute, and GSIA harmonised definitions to the five following approaches in late 2023, described as below:

- Screening: Applying rules to determine whether an investment meets specific criteria, such as exclusionary, negative, positive, best-in-class, and norms-based screening.

- ESG Integration: The systematic and explicit inclusion of ESG factors into financial analysis.

- Thematic or Sustainability-Themed Investing: Selecting assets to access specified trends, such as climate change and the shift to a circular economy.

- We have seen rapid product expansion in this space across asset classes. Under the Europe SFDR framework, they are characterised as light or dark green funds. Sustainable mandates tend to have a significant overweight to Europe and underweight to the US due to Europe's stringent sustainability regulations and enhanced disclosures. On average, the tracking error (deviation in returns from traditional investing) tends to be higher for these mandates, through exclusions and positive focus on a narrower set of companies. Investors should be mindful of these characteristics and know what to expect from such solutions.

- Stewardship/Active Ownership: Using investor rights to protect and enhance long-term value, including board participation, filing shareholder resolutions, proxy voting, and setting industry standards and policies.

- While engagement is more common among equity investors, our annual ESG Manager Survey showed that fixed-income managers are beginning to leverage the unique features of fixed-income investing more implicitly. Fixed-income practitioners with equity offerings leverage their equity counterparts to increase influence.

- Impact Investing: Investing to generate measurable social or environmental impact alongside financial returns, such as adding renewable energy capacity or creating affordable housing.

These approaches are not mutually exclusive and are often used in combination. RIAA2 has a similar but more granular approach, specifically breaking down “Screening” further.

4. Developing a Reporting Framework

A crucial element of responsible investing is having a clear reporting framework to measure and communicate the implementation and positive impact of your policies. This can include climate disclosures and metrics-driven reporting, aligned with frameworks like the Task Force on Climate-related Financial Disclosures (TCFD).

In our latest ESG Manager Survey, we found an increase in ESG metrics reporting for all funds, with carbon emissions standing out as the top metric. Demand for metrics-driven reporting is generally twofold: one for ESG criteria broadly and one for metrics related to climate change, such as carbon footprint. Ensure your provider can produce detailed ESG reports both at the individual fund and total portfolio level. These reports should include key statistics on ESG factors such as ESG risk scores, various carbon metrics, and exposures to certain sectors (i.e., tobacco).

5. Communicate and Collaborate

Reporting is just the beginning. In the long run, effective communication of ESG policies and initiatives will help your organisation stand out, demonstrate your efforts to the wider world, and build lasting stakeholder confidence. You can also seek out and collaborate with organisations that share your values to increase knowledge sharing and leverage collective power.

In summary, establishing a feedback loop throughout the policy-setting or review process is essential:

- Define policy settings based on the organisation’s beliefs and values.

- Work with investment partners to translate beliefs into sustainability objectives and approaches.

- Communicate with stakeholders to ensure transparency and accountability by setting up a reporting framework to track progress and keep stakeholders informed and engaged.

To find out more, please refer to the Russell Investments responsible investing site

1 Australian University Senior Finance Officers Group, https://www.hesforums.edu.au/ausfog