Is the 60/40 balanced portfolio broken? Not forever.

Executive summary:

- The promise of diversification failed in 2022 as both equities and fixed income declined

- Some investors are questioning whether the traditional 60% equity/ 40% fixed income balanced portfolio remains a valid strategy

- Over history, balanced portfolios have rebounded quickly from declines

Everyone knows it by now: 2022 was not a kind year for investors, particularly balanced fund investors. There were no silver linings, no shelter from the storm; it seemed that no matter what levers you had in place to protect clients’ wealth, there was very little to cheer about on investor return statements.

Clients are probably asking themselves (and you): how did this happen? While we can point to a number of likely causes (stubbornly high inflation, central bank tightening, increasing recession risk), I think we can sum it up by admitting that in 2022, the promise of diversification…failed.

When I think of diversification, I think of the classic mix of 60% equities and 40% fixed income commonly known as 60/40 that we’ve all know and trusted for more than seven decades.

When Nobel Laureate Harry Markowitz introduced the 60/40 investment portfolio in his dissertation on Modern Portfolio Theory in 1952, it fundamentally altered the way that both individuals and institutions would invest. Markowitz demonstrated what many before him had not uncovered: that the performance of an individual security mattered less in an overall, well-diversified portfolio. It meant that investors could reduce their portfolio’s risk by investing in a mix of securities that differed in asset classes, capitalization, industries, geographies and return profiles. For years, his theory was proven right. A 60/40 portfolio generally provided a smoother ride for investors than pure equities.

Fixed income has historically been considered the ballast in a portfolio, offering stability and diversification against equity market fluctuations. Over the last 40 years, a balanced portfolio of 60% Canadian equities and 40% Canadian bonds would have returned 8.5% annualized with standard deviation of 9.3%. While a portfolio consisting solely of fixed income would have had lower return with lower risk, a portfolio consisting solely of equities would have had only slightly higher return but substantially higher risk.

| 1/1983 - 12/2022 | Canada Equities | Canada Bonds | Balanced Portfolio |

| Annualized Return | 8.8% | 7.2% | 8.5% |

| Annualized Volatility | 14.4% | 5.3% | 9.3% |

Source: Refinitiv DataStream. Canada equities=S&P/TSX Composite Index, Canada bonds=FTSE Universe Bond Index. Balanced Portfolio=60% S&P/TSX Composite Index, 40% FTSE Universe Bond Index. Indexes are unmanaged and cannot be invested in directly. Past performance is not indicative of future results. Volatility is measured by standard deviation. Standard Deviation is a statistical measure of the degree to which an individual value in a probability distribution tends to vary from the mean of the distribution. The greater the degree of dispersion, the greater the risk.

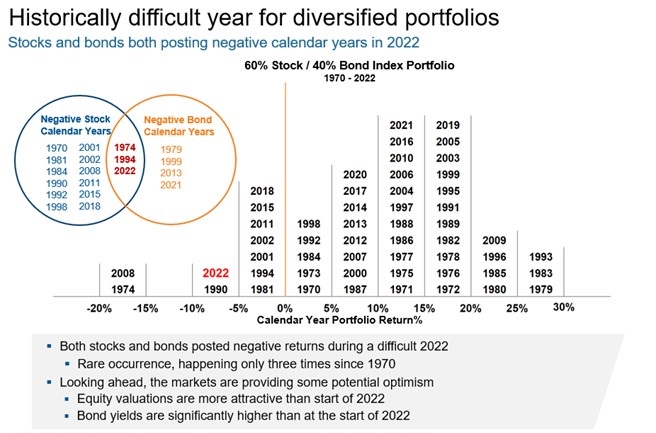

2022 was a bit of an unusual year in that regard. Both stocks and bonds posted negative returns, which has only happened three times over the last five decades. Investors that would have once counted on the stability of fixed income to counter the volatility of equities, were left stranded. Can you blame them for questioning the validity of this asset mix going forward?

Click image to enlarge

Index portfolio of 60% S&P/TX Composite Index and 40% FTSE Canada Universe Bond Index (prior to 1980: FTSE Canada Long-Term Bond Index). Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

Where do we go from here? At Russell Investments we believe the 60/40 strategy is poised to make a comeback in 2023.

Reasons for optimism about bonds

There are a lot of reasons to be optimistic about bonds this year, and not only because it seems that inflationary pressures are finally easing, or that central banks are nearing the end to their tightening cycle. Whether or not you consider it a fixed income renaissance, the fact is that bond yields are at multi-year highs. Higher yields mean that investors can be better protected against future rate increases and if there were to be a recessionary storm, this is a better position for investors to be in, potentially reasserting fixed income’s role as the risk offset to equity market volatility.

While we do see the potential for a mild recession in the next 12 months, one silver lining coming into this year is that investors have choice. One silver lining of the painful fixed income adjustment is that we are finally escaping the world of TINA—there is no alternative—where ultra-low interest rates forced investors into equities and a risky search for yield. Higher interest rates mean that TARA—there are reasonable alternatives—is now a better description of the investment opportunity set.

The return of TARA signals that the traditional balanced portfolio made up of 60% equities and 40% fixed income is poised to make a comeback after its worst year in living memory.

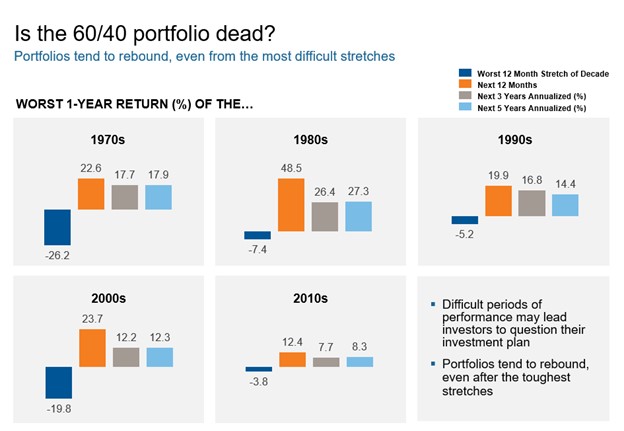

When you further diversify a portfolio by adding U.S. and global equities, there is even greater potential for a smoother ride, The chart below shows that a 60/40 globally balanced portfolio has rebounded from past declines, with the strongest gains coming in the 12 months immediately after a bad stretch. As 2023 hits its stride, we can already see signs the 60/40 global portfolio is recovering from the rout it experienced in 2022.

Click image to enlarge

Source: FactSet. 60/40 Portfolio comprised of 20% S&P/TSX Composite Index, 20% S&P 500 Index, 20% MSCI EAFE Index, 40% FTSE Canada Universe Bond Index (prior to 1980 FTSE Canada Long Term Bond Index). Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

The Bottom Line

Are we going to be okay? In our view - yes. As we all have heard quite regularly: Past performance is not an indicator of future returns. Last year was a challenging one, an anomaly, but as we’ve said before, there is tremendous value in reminding clients of the bigger picture and sticking to the investment plan. Asset allocation strategies may be bruised, but we do not believe they are broken.