Income is the outcome, Part 2: An assessment of today’s lifetime income product categories

The need for lifetime income is becoming more widely recognized among retirement plan sponsors, thanks in large part to the passage of the SECURE Act as well as the nation’s aging workforce. Yet, as we demonstrated in our last blog post on the topic, the specific needs of each retiree vary far and wide, depending on the degree of value each individual places on sustainability, predictability and flexibility. For these reasons, it's unlikely the retirement income marketplace will mature into a universal, one-size-fits-most solution like traditional target-date funds (TDFs). After all, the retirement spend-down complexion of every person is different. A spectrum of investment options for the spend-down phase, which has long been the construct for the accumulation phase, can help retirees in all situations put together the pieces to create an income stream tailored to their specific circumstance regarding benefits package, outside assets, Social Security, required minimum distributions and other household assets and income.

A curated spectrum of decumulation options may eventually win out as the preferred approach to implementing lifetime income in defined contribution (DC) plans. However, as the saying goes, if you don't start somewhere, you won't get anywhere. So, where should a DC plan sponsor start?

Implementing lifetime income: Where should sponsors begin?

A logical starting point is a qualified default investment alternative (QDIA) with a guaranteed payout option, along with a managed account that includes a payout provision. This provides lifetime income bookends for the employees in the plan that want to take their hands off the wheel and receive professional guidance on asset allocation and annuity purchase decisions. Additional lifetime income options could be added to fill in the spectrum as demand increases, and those who are not one-size-fits-all could opt out of the default and choose an alternative. Without including a lifetime income option in the default, participant demand and adoption could remain low, even with a well-designed, post-retirement income menu. We offer it, but no one uses it is an all-too common refrain from DC plan sponsors.

With so many options available in the marketplace, how will a plan sponsor choose? Referring to the three primary financial needs of retirees outlined below–sustainability, predictability, and flexibility–we can design a streamlined array of post-retirement solutions that broadly maps to these different financial needs. A useful starting point is creating a framework to align the different types of lifetime income solutions to high-level participant needs and preferences.

Overview of lifetime income product categories

The chart below briefly describes the various types of lifetime income product categories generally available in the marketplace today and provides a qualitative assessment of the directional indicators of success for each product category. (For a broader description of what each product category entails, please see last December's blog post.)

Chart: Alignment of lifetime income products with metrics of success

| Description | Level of income | Sustainability | Predictability | Flexibility/ Liquidity |

Residual balance |

Explicit costs | |

| Self-managed withdrawal | Self-driven withdrawals over time | |

|

|

None | ||

| Managed payout fund | Provides income based on market performance | |

|

|

|

|

Medium |

| Income-oriented bond fund | Portfolio of fixed income securities with high income potential | |

|

|

|

|

Medium |

| Target maturity bond fund | Portfolio of fixed income securities with a series of pre-determined maturity dates | |

Low | ||||

| Target date fund with guaranteed income¹ | Target date fund that allocates to annuities over time with the option to annuitize in the future | |

|

|

|

Low | |

| Guaranteed lifetime withdrawal benefit (GLWB)¹ |

Balanced portfolio variable annuity provides income regardless of market returns |

|

|

|

|

|

High |

| Intermediate annuity¹ | Insurance product that provides guaranteed income in exchange for an upfront cost | |

|

|

|

|

Not applicable |

|

¹ Insurance product (may be optional) Source: Russell Investments |

|||||||

Mapping lifetime income solutions to participant preferences

To map the lifetime income solutions to employees’ needs in retirement, we must first provide a holistic assessment of each solution on these metrics.

Let's first consider sustainability, which is the goal of not outliving one’s assets in retirement. The probability of running out of money in retirement is low with all of the types of products shown in the chart above—even in poor markets—due to the payout mechanism and/or option to annuitize embedded within them. They are designed to produce sustainable lifetime income, and, in our independent assessment, pass the test.

The next consideration is predictability, or consistent income throughout retirement. The types of solutions that deliver the most income consistency are guaranteed solutions like the immediate annuity and guaranteed lifetime withdrawal benefit (GLWB) and fixed income solutions like the income-oriented bond fund and target maturity bond fund. The TDF with guaranteed income does reduce income volatility², but to a lesser degree, because part of the account balance remains invested in the target date fund glidepath and may require spending adjustments based on capital market performance. The TDF with guaranteed income does establish a predictable and guaranteed income floor that could be used to cover non-discretionary expenses such as food, housing, transportation and health care. Conceivably, discretionary spending outside these items is easier to adjust if one where to experience an unexpected drop in the remaining TDF account balance.

Then, let's consider financial flexibility and liquidity, which is defined as maintaining control over assets throughout the retirement period. The only solution that is truly illiquid is the immediate annuity.³ The guaranteed lifetime withdrawal benefit (GLWB) and TDF with guaranteed income offer less liquidity than the rest. The GLWB can provide liquidity, but at a price. Any withdrawal in excess of the annual guaranteed income amount will reduce the benefit base and, as a result, also reduce the future guaranteed income amount. The TDF offers partial liquidity. The portion of the account balance that remains invested in the TDF is liquid; the portion annuitized by the participant is not.⁴

Finally, we consider the sustainable spending level and remaining account balance at the time of death. The two goals are inter-related. Solutions that maintain a higher allocation to equities in retirement, such as the managed payout fund, guaranteed lifetime withdrawal benefit (GLWB) and target-maturity bond fund,⁵ will generally support higher sustainable spending levels and leave a higher remaining account balance at the time of death. However, an appetite for risk is required, and poor market returns, especially early in retirement, can cause sustainable spending levels to decline below the spending levels of other less aggressive product types.

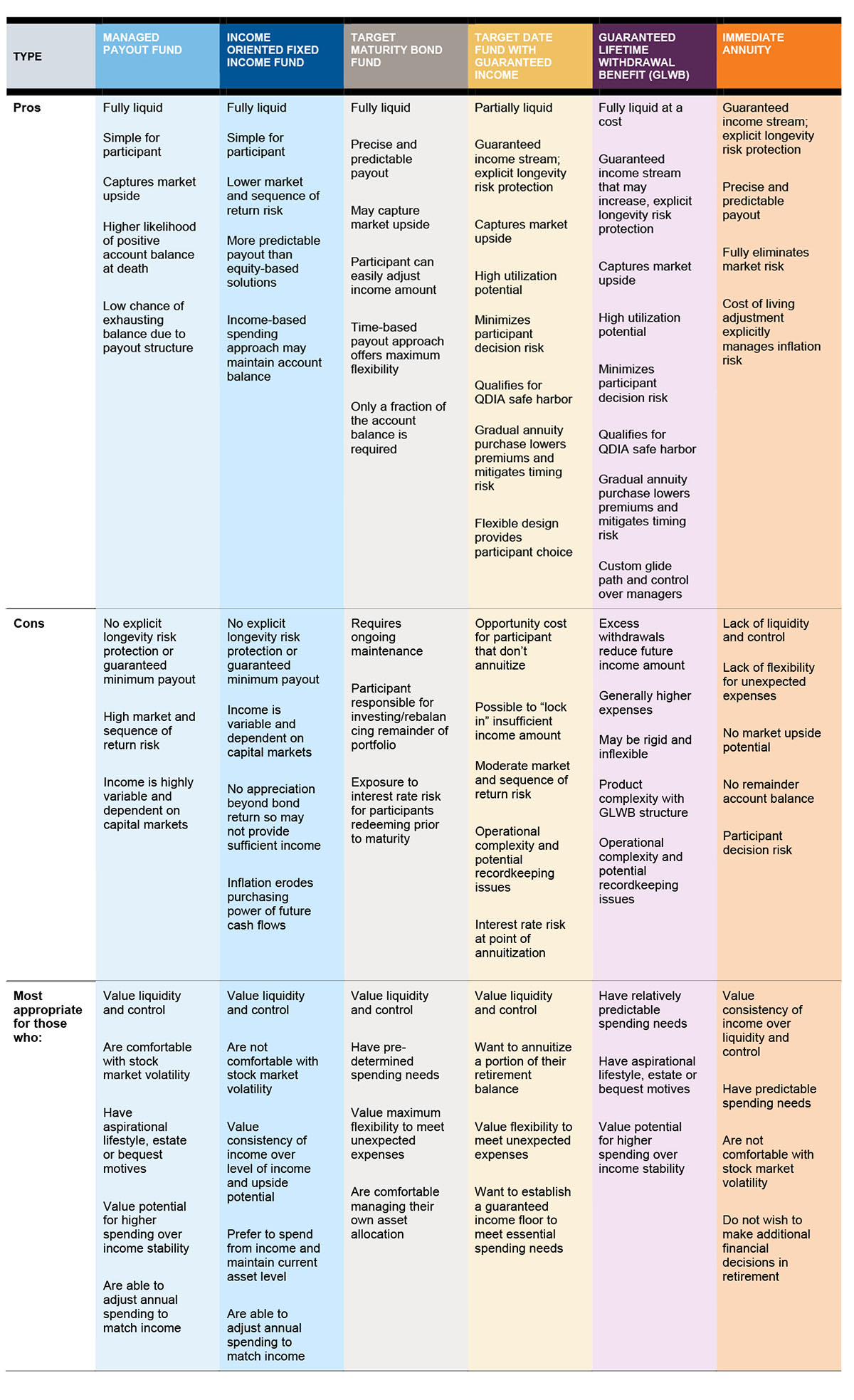

The chart below provides a mapping of the type of participant each product category may be most appropriate for based on the participant's financial needs, objectives and preferences along with the potential strengths and weaknesses of each product category.

Exhibit: Mapping the product categories to retiree needs and preferences

Click on image to enlarge

The bottom line

Our assessment shows that a variety of valid approaches exist to meeting employee needs in retirement. Ultimately, it is unlikely that any one lifetime income solution will fit the majority of employees. Ideally, plan sponsors will elect to a range of lifetime income solutions, leveraging a framework to determine how different product types align with participant needs, preferences and decision factors.

² Assumes the participant elects to annuitize the portion of their account balance allocated to pre-fund the annuity purchase.

³ Subject to annuity contract terms with the insurance company.

⁴ Subject to annuity contract terms with the insurance company.

⁵ Assumes the participants invests the portion of the account balance not invested in the target-maturity bond funds in a target-date fund with a glidepath approximated by the Morningstar industry average. The participant is responsible for investing the portion of the account balance not invested in the target-maturity bond funds.