Income is the outcome, Part 1: Is DC lifetime income ready to take off with SECURE Act changes?

Think about the beginning of your last vacation abroad. After spending hours in the air flying to your final destination, you likely spent the last minutes of the flight in a state of semi-exhaustion—tired, hungry and more than ready to be on the ground.

But, desperate as you were for the flight to end and your vacation to truly begin, imagine how you would have felt if the pilot had parachuted out of the plane at the last moment, leaving you to maneuver the landing on your own. Panicked, shocked and unprepared are the top words that come to mind.

This is akin to how many newly-retired defined contribution (DC) plan participants feel when assessing their financial futures. Because the sole focus of DC plans has historically been to accumulate assets during the working years, plan participants are often provided with little support when they retire—leaving them high and dry when it comes to budgeting their finances during their post-working years.

To continue with the plane analogy, there’s often been a lack of landing gear to help participants smooth the transition from saving for retirement to utilizing their savings during retirement. In other words, there’s been little to no guidance on converting their accumulated savings into a lifetime income stream.

Fortunately, change—at long last—appears to be in the air.

Key catalyst for change: SECURE Act

Five years ago, in a paper on lifetime income for DC plans, we described plans for lifetime income products as being very much in the talk stage. While still largely true today, there’s no denying that such talk is different now. Perhaps most tellingly, the need for lifetime income is now being discussed at plan sponsors’ investment committee meetings—rather than just at industry conferences—often in conjunction with broader committee conversations about asset retention and workforce planning.

What sparked the change? The SECURE Act passed in December 2019 was a key flashpoint. It provided a new fiduciary safe harbor for selecting an insurance provider as a distribution option, and made mandatory inclusion of lifetime income projections on participant statements a reality. We anticipate the SECURE Act will be a catalyst for more organizations evaluating, and eventually adopting, lifetime income for their DC plans.¹ Still, the notion of finding a single income solution that checks the box for all plan participants isn’t realistic for many plan sponsors.

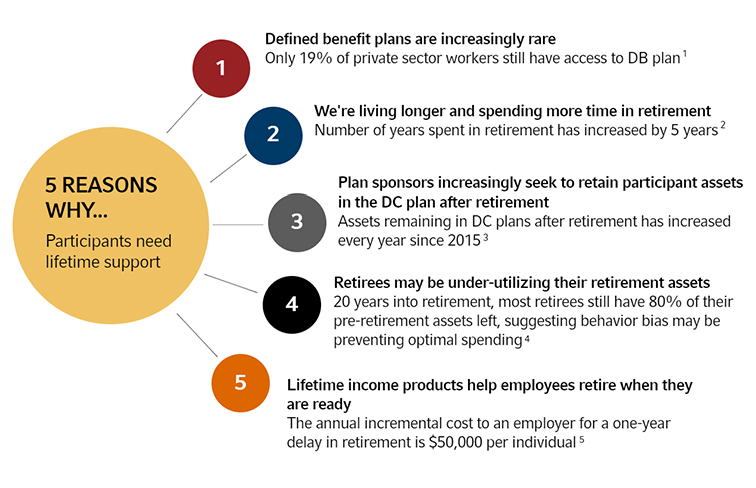

Systemic factors are also stoking the winds of change. The transition from a DB to DC retirement system has shifted several risks from employer to employee. These include contribution risk, behavioral risk and, inescapably, longevity risk. An aging working population also creates an impetus to seek solutions that help manage the high cost of employees not being able to retire on time.

¹ Russell Investments, Sam Pittman, Rod Greenshields (2012) Adaptive Investing: A responsive approach to managing retirement asset.

Exhibit 1: Five systemic forces behind the need for lifetime income solutions

1 Employee Benefits Research Institute (EBRI) Databook;

2 Since 1940 life expectancy of those who reach 65 has increased by five years. Social Security Administration – Life Expectancy for Social Security https://www.ssa.gov/history/lifeexpect.html

3 T. Rowe Price. Percent of DC assets remaining in defined contribution (DC) plans 1 year after separating from service

4 Spending retirement assets…or not? BlackRock Retirement Institute

5 Prudential Insurance Company, “Why Employers Should Care About the Cost of Delayed Retirements."

Ultimately, providing a more certain benefit to employees in retirement is within reach. Amid this backdrop, we encourage plan sponsors to take a multi-faceted approach to helping participants secure income in retirement. This is because participant needs are highly personal—especially in retirement, when everyone is funding toward different objectives. Fortunately, there’s an increasing multitude of products designed to help participants generate lifetime income. Let’s take a closer look at the range of solutions.

A range of solutions for a range of participants

Retirees consistently express three primary needs concerning their assets in retirement. The first is sustainability—the risk of outliving their assets. The second is predictability—consistent income. The third is financial flexibility—liquidity. Together, these key individual needs, in addition to preferences about income level and portfolio volatility, affect participants’ lifetime income decisions. The degree of value assigned to each of these distinct needs typically informs the type of retirement income solution that best matches each person’s unique needs and circumstances. Eventually, we believe consideration of these preference will be used to determine the ideal allocation between investments and insurance products for each individual.

While not intended to be an exhaustive list, the products categories below represent the range of retirement income solutions available in the marketplace today.

|

Self-managed withdrawals |

Self-managed means participants manage their own retirement income by developing an investment plan after retirement along with self-driven annual withdrawals. In this analysis we assume annual withdrawals of 5% of their account value, in line with both the GLWB and the managed payout fund. This strategy assumes that participants understand their income needs and have the willpower to stick to the plan. |

| Fixed immediate/

fixed deferred annuities (includes QLACs)

|

Fixed annuities are an insurance product that allow participants to exchange their retirement assets for a defined periodic payment starting now (e.g., a fixed immediate annuity) or at a future date (e.g., a fixed deferred annuity). Due to interest compounding, the longer the income payment from fixed deferred annuities is delayed, the greater the income payment will be. Qualified Longevity Annuity Contracts (QLACs), sometimes referred to as “longevity annuities,” are a type of deferred annuity where the income payments are deferred until late in retirement. QLACs purchased within retirement accounts using qualified funds have limits, currently the lesser of 25% of the account balance or $135,000 and are exempt from required minimum distributions until age 85. |

| Variable annuity with guaranteed lifetime withdrawal benefits (GLWBs)

|

GLWBs allow participants to invest in a portfolio of stocks and bonds (e.g., a static 60/40 stocks/bonds mix) with a guaranteed withdrawal rate based on a high-water mark of the account value. Upon retirement, a participant may withdraw a contractually defined amount for life, regardless of market performance. This account value is tied to the high-water mark of the participant’s account balance in the GLWBs, and whenever the participant’s account value reaches a new high-water mark, the participant is entitled to an increase in the guaranteed withdrawal amount. Each year on the participant’s birthday, if the participant’s account value in the GLWB exceeds the prior year’s GLWB benefit base, the benefit base is increased to match the account value on that date. |

| Target date fund with guaranteed income

|

A target date fund that allocates to embedded annuities over time to hedge longevity risk. At retirement, participants are provided with the option to use a portion of their account balance to purchase an individual annuity contract directly from insurance companies that will provide guaranteed lifetime income. Only a portion of assets go toward purchasing the annuity as determined by the asset allocation glide path and the remaining balance can remain invested in the target date fund series or be transferred to other investment options. |

| Managed payout fund

|

A broadly diversified fund specifically designed to automatically provide equal and predictable monthly income payments to investors. The payments may be made using investment income, capital gains and return of principal and there are no guarantees related to the payout amount. The funds generally target a specific payout percentage, but actual income distributions may vary based on financial market performance. Managed payout funds can be stand-alone or integrated into a target date fund series. |

| Income-oriented bond fund

|

Fixed income funds that focus on income as a driver of total fund return. Income-oriented bond funds target a high and consistent monthly income distribution by allocating to higher yielding securities while seeking to preserve principal over time. |

| Target maturity bond fund

|

Fixed income funds with a time-based payout mechanism that targets a defined payout at a pre-determined time in the future. The funds use a laddered bond allocation strategy to invest in fixed income securities that mature within a specific year, resulting in repayment of principal plus interest income in that specific year. |

| Managed accounts with payout component

|

These are a feature of a managed account service that provides advice on converting savings into retirement income during the post-retirement decumulation phase. The spending advice can facilitate stable monthly payouts with the option to purchase an annuity out of plan. This product category was excluded from the quantitative analysis because the asset allocation and spending advice is unique to each individual. |

Lifetime income: Helping land the plane smoothly

Let’s return to where we started: the airplane analogy. Ultimately, we believe that reaching retirement should not be a point of abrupt disembarkation for participants, but rather the beginning of a smooth passage into another phase of their journey.

We see this as best accomplished by the increasing utilization of lifetime income products—the landing gear necessary for today’s DC plans. To support participants with this transition, we believe the next step for DC plan sponsors is to include solutions in their investment menu that convert accumulated retirement savings into a lifetime income stream.