Why you can't automate your retirement

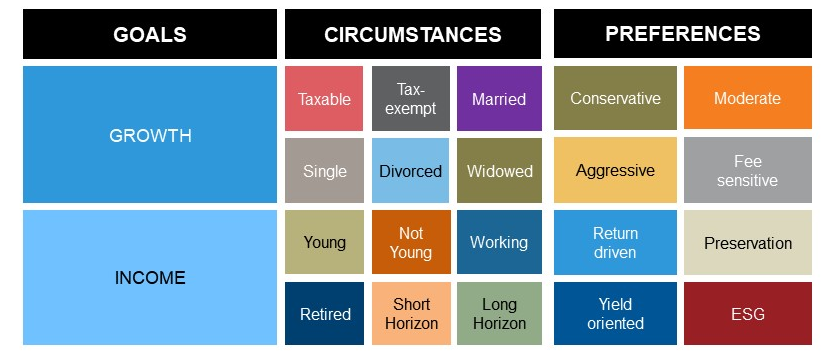

I recently read an opinion piece on why target date funds are the best and only retirement investment you’ll ever need. After seeing how messy the markets and investing can be, I cringe when I see articles promising a single solution to meet your retirement needs. A one-size-fits-all solution might apply to other areas of our lives but when it comes to retirement, your goals, circumstances and preferences will be very different than anyone else’s.

{kind=link}

Since corporate pensions have disappeared for most of us, we investors are forced to take on the investing responsibility in our 401(k) plans. This can be exciting or painful depending on your investing prowess. If you’re a novice, it’s easy to miss considerations for proper asset allocation, risk tolerance and expected return. It’s not surprising that target date funds are the default solution when you’re young and land your first job out of college.

I remember combing through my 401(k) options for the first time and it felt like a daunting task. Let’s face it, when you’re just starting to build your wealth, an investment option that offers broad diversification and a set it and forget it approach is very attractive as a new investor. It’s not surprising that this has become an attractive option, with trillions in assets, and continues to be one of the fastest growing categories of mutual funds.

What’s appealing about target date funds?

The main appeal is that they’re likely great for many people who may have no interest in taking charge of their investments. After all, they automatically provide you with a glide path that gradually reduces your exposure to equities and gradually increases your exposure to bonds as you get older. The best part is you don’t have to think about it. But in my experience, when it comes to your money and as you get older, very few things should be automated. Sure, it’s fine to automate the cable and electric bill payment, but your retirement nest egg is different.

We believe you need to be actively engaged and ensure your goals are on track and that your risk tolerance matches an appropriate asset allocation. This doesn’t mean changing your investments every month, but it does mean a more sophisticated approach than the set it and forget it mentality of target date funds.

Drawbacks of target date funds

We assume too much in this business. We assume everyone will retire around the same age, we assume that everyone should adhere to a pre-determined asset allocation and we assume that when someone is ready to retire, their portfolio will be set for life. If you’re 50 years old, do you think another person who is 50 years old will have the same risk tolerance? How about the same saving habits? Maybe you will get an inheritance and they won’t.

Making assumptions for every shareholder is the main drawback with target date funds. Since it’s solely focused on your birthday, they determine a specific percentage allocated to stocks and bonds. While this can be helpful to some shareholders, every shareholder has different circumstances in life—such as receiving a lump sum, sale of a business, or sale of real estate—or experiences changes in the market itself. Kudos to you if you predicted the global pandemic this year.

It’s also important to note that target date funds don’t consider all the holistic services a trusted financial professional provides to you that can impact your proper asset allocation. Whether it’s social security tips, long-term-care insurance, planning for estate taxes, or advice regarding company stock, a target date fund simply doesn’t have the ability to factor this into your situation.

The next evolution: Personalized retirement solutions

We believe the next evolution of target date funds is a managed account solution. Managed accounts are personalized and easy and they can target retirement income. They offer participants individual asset allocation customization while leveraging the preferred products/options selected by the plan advisor and plan sponsor for the plan menu. Managed accounts customize an asset allocation for each participant from data gathered by the recordkeeper (age, salary, savings rate, etc.). Managed accounts focus on meeting plan participants’ target retirement income rather than solely focusing on accumulation. This is to help plan participants gather sufficient income in retirement to maintain their lifestyle and adapt as circumstances change. By helping you build out a custom asset allocation, managed accounts can help improve that probability.

We do this for our institutional clients, and we strive to make that a reality for advisors helping individual investors. Instead of spending the time to build a menu of funds to only watch investors go into a target date fund, managed accounts typically use a plan’s core investment options as selected and monitored by the financial professional. By adopting managed accounts as the plan’s qualified default investment alternatives (QDIA) you’re fulfilling two major fiduciary responsibilities: customized allocation and investment selection.

The bottom line

Technological automation has taken over our lives. Let your retirement portfolio be the area where you take a more hands-on approach. Working with a trusted financial professional to make sure your retirement portfolio reflects your entire financial picture and not just your birthday is the sensible approach to take for the short and long term. Your retirement nest egg is a top financial priority—thus we believe an active approach is required.

When we buy big ticket items like a house, few things about the process are automated. We hire an agent that can help fulfill our requests, we spend hours researching online if the neighborhood is good and we hire a home inspector to make sure our capital isn’t at risk. Doesn’t your retirement nest egg deserve the same personalized approach?