Process is key when determining the right tactical decision

Our global dynamic process is focused on assessing "unsustainable extremes" in the near-term. The Russell Investments Managed Portfolios are underweight U.S. tech stocks and hold nearly zero exposure to high yield debt. Together with allocations to commodities and volatility strategies, these have been positive contributors in early-2022.

In this blog, we discuss our overall process, as well as our latest research and insights into portfolio management. We believe a process should be repeatable when determining the right tactical decisions, and we've seen evidence of success over the 2020-2021 pandemic period. Right now, we think it's best to be ready but slightly more patient before adding outright exposure into global equities and high yield debt.

What's driving the weakness in global equity markets?

2021 was a very strong year for equity and credit markets. However, in early-2022, equity, bond and commodity market volatility has risen globally. The year started off with U.S. tech stocks de-rating, after some mixed earnings results and increasing expectations of higher interest rates, lifting the cost of capital for companies. More recently, Russia's invasion of Ukraine caused further uncertainty, as commodity prices rose due to the potential supply shortages; and credit markets has started to show signs of weakness.

In Australia, markets have been much calmer as the domestic economy reopens from the latest lockdowns and as commodity prices rise. The domestic property market is more evenly balanced, and the Reserve Bank of Australia is going to be slower in raising rates than other major central banks.

Why is a dynamic investment process key in different market conditions?

My colleague, Alexander Cousley (Asia Pacific Investment Strategist) and I are members of the global macro strategy team. This team is responsible for assessing and recommending whether portfolio managers should buy or sell growth assets over a tactical time horizon.

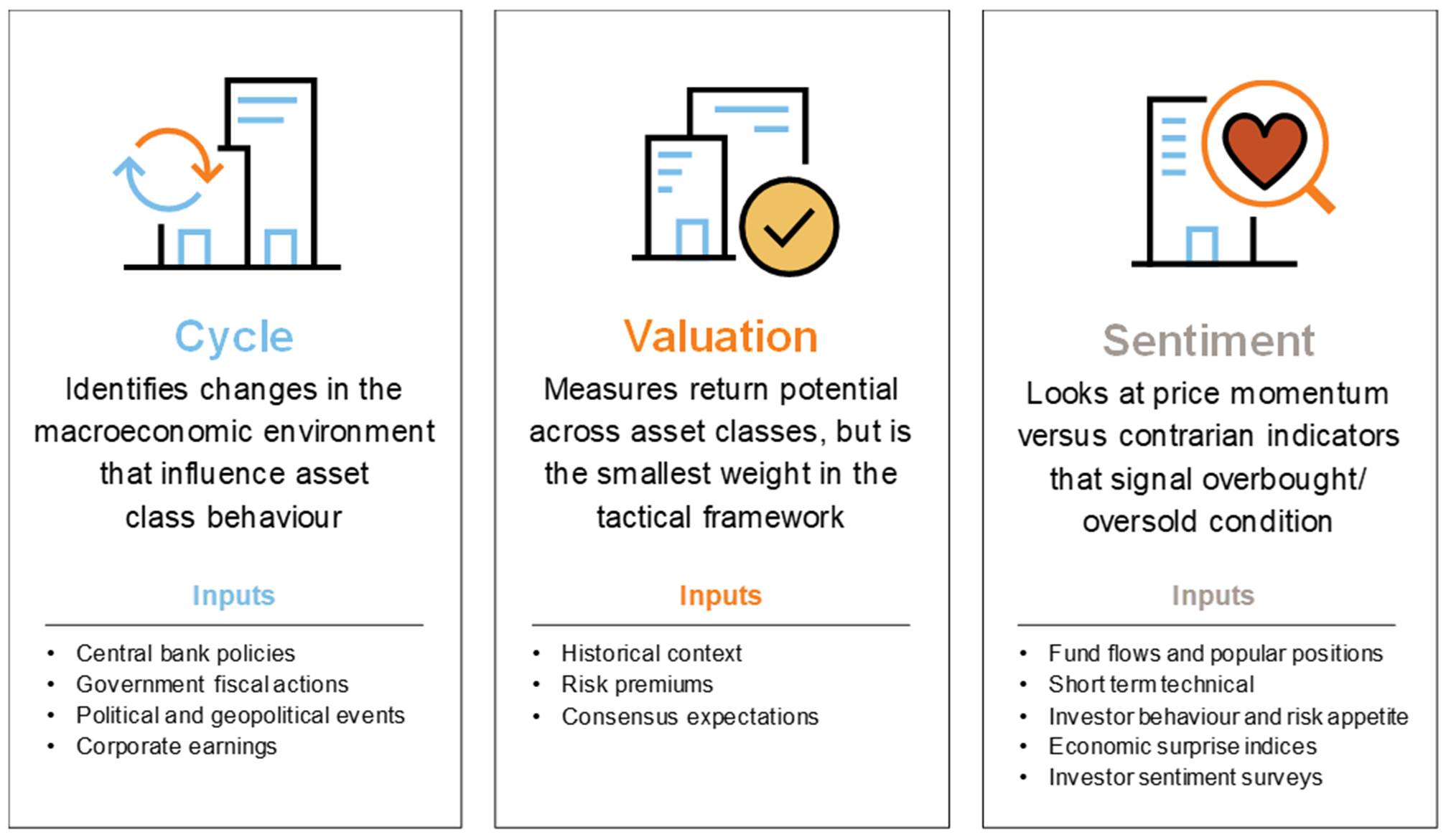

In March 2020, during the early and most volatile stages of the pandemic, the team recommended portfolio managers increase exposure to growth assets with strong conviction. This recommendation was supported by the view that the market was at an "unsustainable extreme" and the global economy would eventually rebound from the sharp and deep recession. This recommendation is based on our investing framework that focuses on the Cycle, Value and Sentiment (CVS) of equity markets.

Click image to enlarge

Source: Russell Investments.

Following this recommendation, Russell Investments' global model portfolio was updated in 2020 to reflect this high conviction buy signal. This model portfolio process is a communication, and risk budgeting exercise that requires portfolio managers to debate and decide on the sizing of each position.

Fast forwarding to the present day, it is our view (before and after the Russia-Ukraine crisis) that we should be getting ready to buy into global equities and high yield debt. We've had numerous global calls and walked through the different bull, bear and base scenarios. The Cycle view is positive, despite some increasing uncertainties. Equity markets are closer to fair value outside of U.S. Our proprietary Sentiment indicators are showing some strong oversold signals, however, they are not yet at an "unsustainable extreme". And later this month, our Global Head of Investment Strategy, Andrew Pease, will be discussing these views in greater detail in our Q2 Global Market Outlook.

What's the plan going forward?

If there is a formal signal to buy, we will be looking to add 2-3% of global equities, to take our managed portfolios back to the higher range of growth assets held in early-2021. We'll also consider buying into global high yield debt. This becomes a more attractive proposition if credit spreads were to widen by 1 to 1.5% (i.e. increase in yields provides greater risk-adjusted compensation).

Lastly, we'll plan for a stage 2 buy signal if we see further weakness in markets. It is possible that a sharp and quick selloff could occur, as markets may panic very quickly, as we saw in December 2018 and March 2020. This is not our base case. However, the macro strategy team will focus on our "CVS" framework and the portfolio management team will plan for multiple scenarios. This is consistent with the example in March 2020. For now, we're sticking with the current positions.

The bottom line

The plan across the strategy and portfolio management teams is to add growth assets. We continue to follow our global process which worked during one of the greatest crises ever seen. We're constantly fine-tuning and debating the different nuances, as equity selloffs occur for different reasons. The Russell Investments Managed Portfolios are positioned for an eventual rebound in growth assets but at the same time we are preparing for more near-term volatility.