CalPERS increases equity exposure. We believe a different approach may be worth considering.

The California Public Employees’ Retirement System (CalPERS) made a splash last month when they raised their equity exposure from 46% to 50% and decreased cash from 4% to 1% in their portfolio. While mathematically appealing, we believe it may not be the best course of action for investors to follow suit and increase risks levels in their portfolios, given current valuations.

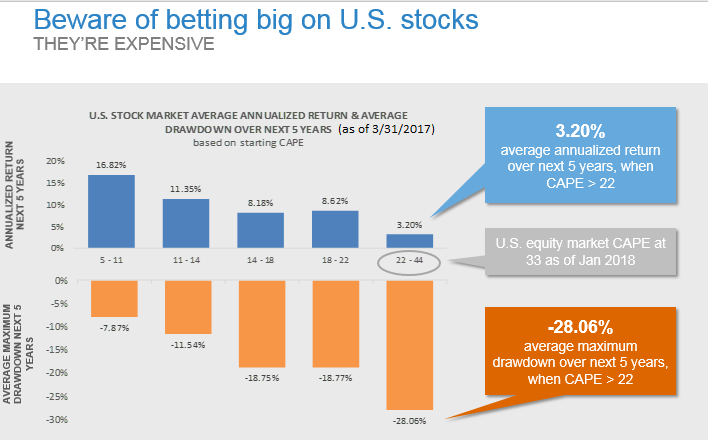

We’ve talked a lot about the low return imperative for the coming decade. That imperative is because starting valuations on bonds and equities are quite high. As the chart below shows, forward-looking returns are low. We believe there are four ways investors can consider addressing this problem:

- Risk-up portfolios, increasing equity exposure

- Contribute more to their portfolios

- Patiently wait until returns will be higher

- Squeeze more juice out of their portfolios

Source: http://www.econ.yale.edu/~shiller/data.htm.1

Russell Investments believes that the first option may not be the best. The math says most investors need higher returns than current asset allocations will provide, so an actuary may tell you (and they would be right) to increase the allocation to the higher-returning asset types in the portfolio. In other words, increase equity exposure.

I am sure CalPERS has greatly debated this approach. And their approach is mathematically correct over the long-term. But I believe it under-appreciates the specific, current path which the pool of assets may take to the end objective. Increasing equity risk at a time like this, when equity valuations are so high, greatly increases both the probability and the magnitude of a meaningful portfolio drawdown in the coming five years. Investors like CalPERS may be setting themselves up for a large drawdown—and a worse starting point after this drawdown occurs. It would be hard for even the most stalwart investor to stay on such a volatile path. To achieve long-term growth, it is inherently important to not only grow the upside, but arguably even more important to protect the downside.

Instead, we believe investors may want to consider a different route—a road less traveled: one that works to deliver the returns the portfolio requires along a path that the investor can survive. This goal is a reason why we believe in a best-practice, multi-asset approach that combines long term professionals with actuarial backgrounds with multi-asset portfolio managers who bring to bear in-the-market, intermediate-term thinking.

The hard truth: Increase contributions

Instead of simply increasing risk through greater equity exposure, we believe that a combination of greater contributions, patience, and getting the most juice from an existing portfolio is an approach worth considering. Increasing contributions can be quite painful for investors. It’s an acknowledgement of the uncertainty, and mediocre long-term outlook, of markets and the necessity to pitch in. It’s also one of those fierce conversations that many asset managers try to avoid having with their clients. I get that. As the father of young kids, I can attest that no one likes being told to eat their vegetables. But the best asset managers act as true fiduciaries. To fulfill our duty, we need to speak the truth, no matter how much it hurts. The tempting alternative is to overpromise higher returns. As an industry, we asset managers must avoid that temptation and thus help investors avoid failing allocations.

Plain old patience

The first two options are where a skilled asset manager can carry its weight from an investment perspective. Option three—plain old patience—is a behavioral nightmare because FOMO—fear of missing out—is inherent in all of us. Valuations have historically been a fantastic guide for future long-term returns.2 The problem here is the long-term part. The 12-month return for the S&P 500® Index prior to a market peak over the last 50 years on average has been 25%.3 In the most extreme example, in the late 1980’s Japanese equities rallied from a cyclically adjusted price-to-earnings (CAPE) ratio of 50, all the way up to above 70 over the next three years, producing a return over 100% before undergoing one of the most painful drawn-out valuation compression cycles in history over the coming 20 years.4 The US equity market is only at a CAPE (cyclically-adjusted price-to-earnings ratio) of 33 as of Jan. 4, 2018,5 so patience is behaviorally difficult.6 But we believe asset managers acting as true fiduciaries will maintain robust checks and balances to ensure they limit the opportunity to fall prey to these emotions we all have.

How much juice can you squeeze from your portfolio?

The last option—squeezing more juice from the portfolio—is my favorite, because, as a self-described geek, I get to help solve a complex problem with all the capabilities a world-class asset manager has to bear.

In discussing the low-return imperative, we have said there are three main ways to adapt to the current environment prudently:

- Search out returns wherever they are, even when it is uncomfortable.

- Ensure every risk in the portfolio has a return attached to it.

- Pay explicit and laser-focused attention to costs and fees, reducing them where prudent.

Costs and risk management are vital, but we can save them for another day and focus on searching out returns, wherever they are in the marketplace. We believe it may be wise for investors to consider the following:

- Use valuation as a guide. As of Sept. 30, 2017, and according to the MSCI Emerging Markets Index, emerging-markets (EM) equity is trading at roughly half the valuation of U.S. equity.7 We believe investors should have meaningfully more EM equity in their portfolio today, as compared to 2007 when the reverse was true. This may improve long-term returns.

- Invest uncomfortably. Raise your hand if investing in Venezuelan or Russian debt gives you warm fuzzies? It’s not comfortable, but today, EM debt has a forecasted return that is not meaningfully different than U.S. equity over the long-term, but has a drawdown risk that is only half of U.S. equity in a stress scenario.8

- Sell liquidity. We believe in an illiquidity premium. That is to say, we believe investors are paid over the long-term for foregoing their ability to get their money back right away. Investors need to be careful today selling liquidity, because valuations in all spaces are high. We believe that being selective with active managers who are patient (there’s that word again) in deploying capital may be an approach worth considering.

- Use leverage, explicit and imbedded. For many, leverage and derivatives are dirty words, but prudent use of these tools can help improve portfolio efficiency. For instance, we believe that define-benefits plans should be efficient in their use of capital by extending duration and over-allocating to return-seeking assets.

- Capture risk premiums within asset classes. We believe there are return premiums for tilts in portfolios toward certain factors. Over the long term, greater exposure to the value factor in equity, or to the momentum factor in currency, may add incremental return to the portfolio.

- Increase selection alpha. We are big proponents of hiring active managers who let it fly, while we worry about holistically managing total-portfolio risk. In this go-forward environment, we believe asset managers that allow the presence of ballast in the portfolio—through managers of mediocre conviction—leave returns on the table.

- Manage alpha dynamically. Clients should expect their asset manager to adapt portfolios responsibly in real-time, to capture returns and manage risk. This is difficult. And it comes with a lower information-ratio proposition, compared to risk premiums and selection alpha. But we believe it is a requirement for success today.

Einstein was famous for saying, “Make things as simple as possible, but no simpler.” When it comes to solving the low-return imperative, there is an understandable desire for simplicity. And rational investors, like CalPERS, may find solace in taking on the future risk of drawdown in the pursuit of higher returns, because it offers a solution with less complexity. We believe that is a dangerous over-simplification.

The solution outlined here is detailed and more complex, because markets are unavoidably complex. Multi-faceted solutions are required to solve multi-faceted challenges. As investors, we need to take our medicine and contribute more. We need to fight our behavioral tendencies and be patient. And we need to use all of the tools in the toolkit to try to enhance returns. The alternative may be comfortably failing, slowly through time, and then all at once.

1 Yale Professor Robert Shiller calculates a Cyclically Adjusted P/E Ratio based on stock price divided by prior 10-year earnings. U.S. stock market is represented by an index created by Professor Shiller. The stocks included are those of large publicly held companies that trade on either of the two largest American stock market exchanges: the New York Stock Exchange and the NASDAQ. Prior to 1926 his data source was Cowles and Associates Common Stocks Index, after 1926 his source has been S&P.

Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly. Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment. Average drawdown is the percentage return from period start date to the market trough within the subsequent three years.

2 Source: Russell Investments research paper: Pittman, Sam and Srinivasan, Sangeetha, Designing portfolios with lower drawdown risk, September 2017

3 Source: http://www.businessinsider.com/average-performance-of-sp-500-before-and-after-market-peaks-2015-11

4 Source: Nikkei 225 Index. https://siblisresearch.com/data/japan-shiller-pe-cape/

5 Source: https://www.multpl.com/shiller-pe

6 Source: http://www.econ.yale.edu/~shiller/data.htm.

7 Source: Russell Investments, MSCI Emerging Markets Index. https://www.bellevue.ch/all-de/all/bellevue-deutschland

8 Source: Russell Investments Capital Market Assumptions. Please note all information shown is based on assumptions. Expected returns employ proprietary projections of the returns of each asset class. We estimate the performance of an asset class or strategy by analyzing current economic and market conditions and historical market trends. It is likely that actual returns will vary considerably from these assumptions, even for a number of years. References to future returns for either asset allocation strategies or asset classes are not promises or even estimates of actual returns a client portfolio may achieve. Asset classes are broad general categories which may or may not correspond well to specific products.