Today's bumpy markets have created some "road hazards" for advisors. Here’s how to navigate through them.

Advisors have long been described as financial guides, helping clients and their families navigate the twists, turns and inevitable bumps along the road of financial life. A quick Google search provides numerous examples of this metaphor, from photos of scenic cliffside highways to artistic renderings of compass icons.

The expert guidance that advisors provide to their clients is most valuable during the bumpy stretches, when uncertainty and market volatility can leave investors looking for the nearest exit ramp. While great advisors help their clients stay on track despite the bumps, the best advisors embrace the challenge of the bumps as opportunities to bolster their client relationships and impart positive long-term decision-making. Sometimes the bumps, or better yet road hazards, along the way can leave you as an advisor feeling like more a director of traffic than a navigator of the road ahead.

How can you turn these road hazards into opportunities? The three issues we’re hearing that are presenting the biggest opportunities for advisors today are around fees, performance and taxes.

Road Hazard 1: My client’s account values are down. How can I avoid challenges to my advisory fee?

It’s no surprise that many advisors say they are being challenged on their fees more in the last seven months than in the last seven years, given what markets have been up (or should we say down) to lately. Even experienced advisors with successful practices may be dealing with this issue right now.

It might be tempting to address fee questions from the perspective of performance, but that ultimately puts you on your back heel, defending market activity over which you have little control.

Instead, if you meet fee questions as an opportunity for deeper conversations, you can deliver value that simply can’t be matched by addressing just the surface objection. In this case, recognize that a client’s concern about fees often comes from a deeper, more emotional place, prompted by fears of money experience and attitudes in the client’s past. So, in order to help a client navigate the road ahead, advisors who use fee questions as an opening for deeper engagement find themselves retreading past ground first. Helping the client uncover the connection between their past and present experiences can increase the likelihood that those clients will stick to their long-term plan.

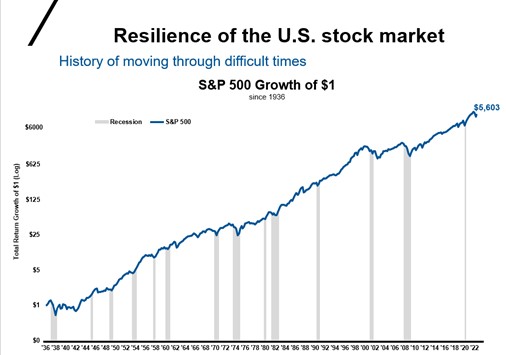

As we have noted in our annual Value of Advisor study, an advisor’s value is derived from the broad variety of services you provide your clients. This includes keeping them from making behavioral mistakes when markets are challenging. Remind them that their investment plan was designed to help them meet their financial goals and that bumps in the market are just that—bumps. As the chart below shows, despite many bumps along the way, the U.S. stock market has moved higher over the longer term.

Click image to enlarge

Source: St. Louis Fred & Morningstar Direct. S&P 500 index as of 8/31/2022. Log: Lognormal scale. Total Return: Includes dividend reinvestments.

Road Hazard 2: This is the first prolonged downturn in recent years. How do I address the calls from clients to make changes in professionally managed models?

It’s quite common for clients to suggest or demand to make changes to their holdings when the market is down. Clients expect action from you during times like these. Action can feel reassuring: it’s a way out of an uncomfortable situation. But responding to a client’s invitation to make changes to my portfolio looks different in an advisory relationship than in a brokerage account.

In an advisory relationship, the best first action in most cases like this one is decidedly not to overhaul the investment strategy you have agreed on. Instead, review together with the client their goals, circumstances and preferences that formed the basis for selecting the current investment strategy. If those important details haven’t changed, overhauling the investment strategy is likely a costly exercise without much benefit.

At the end of the day, your client’s portfolio is meant to help fulfill their financial goals. Starting the conversation with a discussion around what may or may not have changed in their life to determine where are we now on their individual journey, gives you the context necessary to determine whether material changes to their strategy are necessary. This seemingly small action can have a big impact on a client’s ability to better tie the portfolio solution of today to their future outcomes. Being able to make the connection that your client is still on track is often more than enough for most.

For some, shifting goals may mean reallocating or rebalancing to help realign the investment strategy. Taking a systematic approach can reassure your client about when and why you make changes. This can help clients differentiate between the act of making constructive change to address shifts in the plan versus reactive change to satisfy the urge to respond to undesirable market conditions.

Another way to use this type of question to elevate your conversation and demonstrate the value of an advisory relationship, is to prompt a beneficiary review. Aside from the benefits of accurate recordkeeping, it helps your clients take action in a meaningful way, fosters loyalty and offers you an opportunity to uncover potential additional assets. Most of all, a beneficiary review helps you get to the heart of who and what your client is investing for, which in turn can help you understand how to keep them on track during times of uncertainty in the future. Because chances are, the current volatility will not be the last that you and your clients will weather—hopefully together.

Road Hazard 3: Capital gain season is looming. How do I engage in a productive conversation around the impact of taxes when my client’s accounts are down?

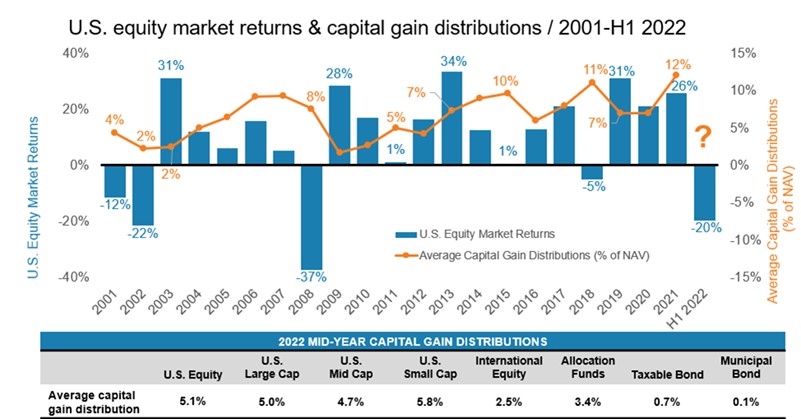

Capital gain distributions can materially impact your client’s pocketbook and after-tax returns, even in the worst market years. You’d expect capital gain distributions to be up in up markets; clients can generally accept that logic as well. It’s the down market years that are a double-whammy head-scratcher for most people. Investors often correlate distributions to portfolio gains, leading to plenty of confusion and uncomfortable conversations when capital gain distributions are made in negative market years.

Consider that in 2018, where the year-end return on the S&P 500® Index was -5%, with 91% of U.S. equity funds being negative for the year, 86% of funds still paid a capital gain distribution to investors. On average that distribution was 11% of net asset value (NAV). While we don’t know today what the market and capital gain distributions situation will be at the end of the year, the potential remains for an additional hit to your clients’ pocketbook.

Click image to enlarge

Source: Morningstar Direct. U.S. Stocks: Russell 3000® Index. U.S. equity funds: Morningstar broad category ‘US Equity’, all other categories are based on Morningstar Category Group each including mutual funds and ETFs. For years 2001 through 2013, used oldest share class, 2014 forward includes all share classes. Average Capital Gain Distribution % = calendar year cap gain distribution ÷ year-end NAV (For years 2001 through 2020), = total cap gain distribution ÷ respective pre-distribution NAV (For 2021 & 2022). Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment.

The first step in avoiding this painful bump in the road is to use tax-managed strategies for non-qualified assets. Not doing that systematically yet? That’s ok. This year’s weak market may be offering you and your clients a silver lining: an opportunity to potentially realize lower gains in non-qualified accounts, creating an opportunity to transition those assets to a more tax-advantageous investment approach. This could have the potential to help your clients save money on taxes in future years and make their long-term goals more achievable.

How can you get started? Review your book for non-qualified accounts that could be better positioned in a dedicated tax-managed strategy instead, and talk to your clients about making this meaningful and constructive change. It will give you an opportunity to reframe the tumultuous markets in a more favorable light for your clients, focus their attention on something they can control and demonstrate your value in being an astute asset locator for your client’s wealth.

Conclusion

Today’s investing environment can wear down clients and advisors alike. The questions around fees, performance and taxes can add to the challenging times we are facing in the markets. But they don’t have to.

Many advisors keeping clients on the road ahead toward their goals are empowering their clients to focus on the factors within their control. Connecting the client’s portfolio to what’s most important to them and their family is foundational. Using that connection to help mitigate the calls for making changes during volatility can be very helpful. Lastly, helping clients act on the potential tax impact on their investments helps keep the focus on the bigger picture—keeping more of what you make better enables clients to reach their goals.

This won’t be the last uncertain and challenging year we see. But in our experience, there’s no more valuable opportunity to be a true navigator for clients than when the road to achieving client’s goals is fraught with hazards.