Keep calm and keep your plan participants invested

Retirement plan participants are faced with headlines every day that inevitably cause them to consider bailing on investments when markets get jittery. Whether it’s a global pandemic, trade war talks or a looming election, headlines can be very distracting.

On days where headlines are alarming and plan participants are wondering what’s happening to their retirement savings, it's more crucial than ever to remind them of the bigger picture. At Russell Investments, we believe that plan sponsors can help their participants prevent missteps that can lead to bigger shortfalls than they are already facing. Recent events have served as a reminder of this. Investing can be uncomfortable for a lot of people, but does it have to be?

To help ease some of the angst, here are three general guidelines to help keep participants calm and invested.

No one (really) can time the markets

"In the financial markets, hindsight is forever 20/20, but foresight is legally blind. And thus, for most investors, market timing is a practical and emotional impossibility." – Benjamin Graham, The Intelligent Investor

Even the most sophisticated of investors will tell you that it is virtually impossible to accurately predict the market's short-term moves. In fact, mistiming can be disastrous to investment returns. In a low growth/lower return environment, what does this mean for your most vulnerable participants? In today's reality, where investors are more likely than ever to face retirement income gaps, they can't afford to miss out on returns.

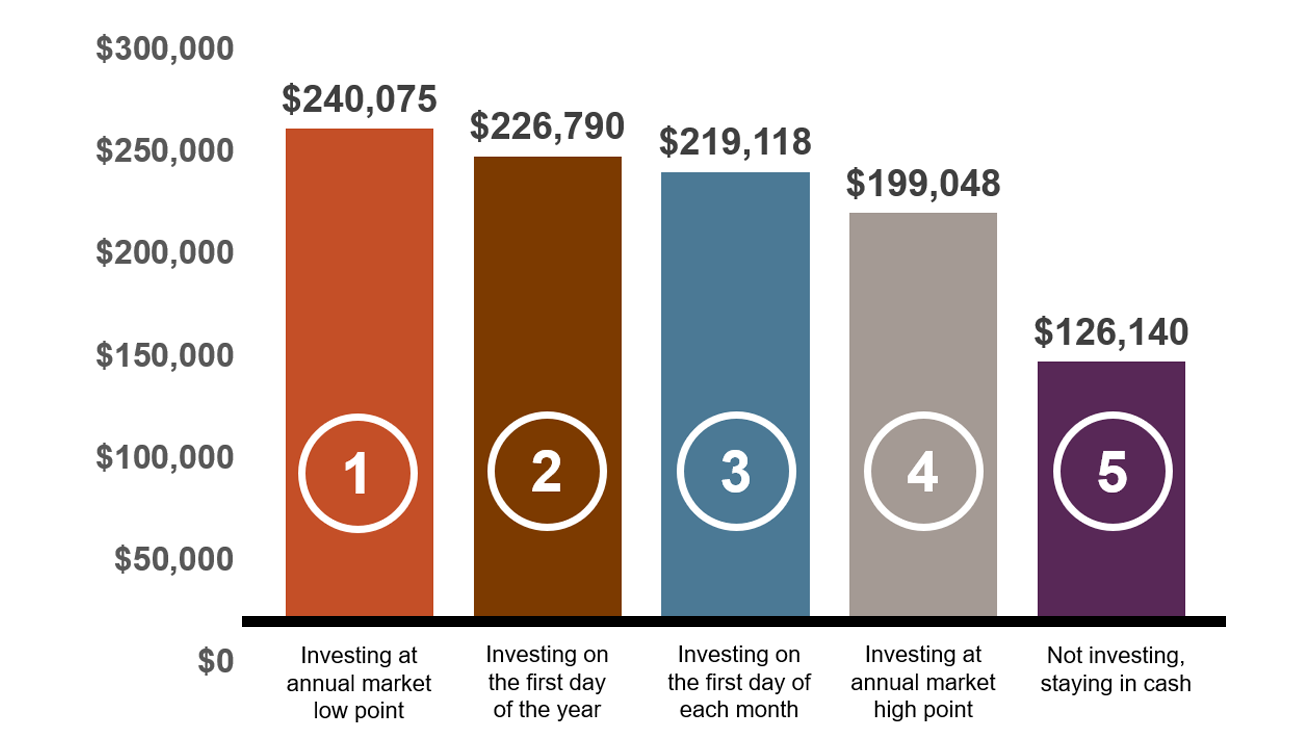

We believe in the power of being invested over the long-term. Not being invested (strategy #5 in the chart below), and simply leaving money in cash, yields by far the worst ending wealth of any investment option. Even investing your money on the worst days of the market (strategy #4) is still more favorable than not investing at all.

Be invested, stay invested

Focusing on long-term outcomes

|

Perfect timing |

First of |

Dollar cost averaging |

Perfectly wrong timing |

Holding cash, no investment |

| This strategy is ideal yet implausible. | Investing your money for the most amount of time can yield the most gain in most market environments. | A popular rules-based strategy. May help investors cope with uncertain or volatile markets. | Despite bad timing, assets invested in the market may grow faster than if left in cash. | Holding cash too long can result in the least growth of wealth. |

Hypothetical ending wealth after investing $12,000 per year for 10 years

Period ending February 29, 2020

Note that one year represents a 12-month period ending February 28 or 29 (depending on leap year).

Assumes a one-time investment of $12,000 per year into a hypothetical balanced portfolio with no withdrawals between February 28, 2010 and February 29, 2020. Source: Russell Investments

Cash return based on return of $12,000 invested each year in a hypothetical portfolio of 3-month Treasury bonds represented by the FTSE Treasury Bill 3-month Index without any withdrawals between February 28, 2010 and February 29, 2020. Source: Morningstar

Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, and are not a guarantee of future performance, and are not indicative of any specific investment.

Hypothetical analysis provided for illustrative purposes only.

Nothing, especially volatility, lasts forever

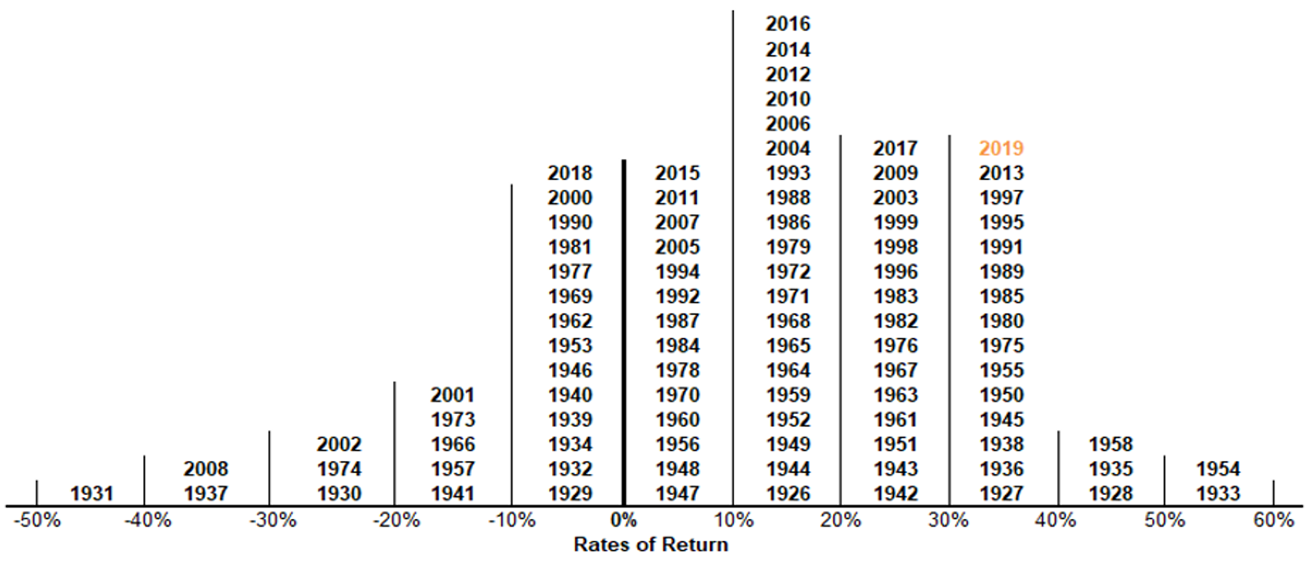

There have been many times throughout history where markets have pulled back—but these relatively short periods are most often followed by the most favorable returns. Unfortunately, due to loss aversion—one of the principles of behavioral economics—people tend to remember the bad twice as much as the good¹. This means that despite having experienced the longest bull run in history, a few bad days in the markets can cause investors to rethink their long-term investment strategy.

Since 1926, stocks have more often finished the calendar year in positive rather than in negative territory—in fact, 73 percent of the time, as evidenced in the chart below. It’s extremely challenging to predict whether a calendar year return will be positive or negative.

Historically it has paid to own stocks

Calendar year S&P 500® Index returns 1926-2019

73% of the time, U.S. equity market has posted calendar year returns above zero

Source: Represented by the S&P 500® Index from 1926-2019.

Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

Diversification matters

"The only investors who shouldn't diversify are those who are right 100% of the time." – John Templeton²

Having a robust strategic asset allocation with regular rebalancing, or investing in a professionally-managed asset allocation solution like a target date fund, can potentially enhance returns, but more importantly, manage volatility.

Asset classes change leadership regularly. Russell Investments has consistently advocated for investors to consider a global multi-asset approach to investing. We believe doing so puts investors on a smoother path toward meeting their goals. Put simply, investors diversify because the future is uncertain, and no one can predict with certainty which asset class will win or lose over the upcoming cycles.

The bottom line

While navigating uncertainty and extreme market volatility is difficult, it’s important for participants to keep the big picture in mind and stay focused on their long-term goals. Historically, over the long term, markets have been positive more often than negative, as shown in the previous chart. Volatility is a reality, even in positive markets, and diversification is a tool every investor can rely upon to help them withstand market corrections. Down markets offer the opportunity to "buy low" with regular, monthly 401(k) contributions via payroll deduction. Whether a plan participant is invested in a professionally managed target date fund, or is a "do it myself" investor, economic uncertainty will always be a cause for anxiety, so it’s important to try to remember these guidelines when the markets get choppy.