Are your clients worried about a market crash? A checklist for survival

It's the end of the world!

Well, it is if you believe what you read on some Internet sites and some people on YouTube.

The other day I was sharing stories with an advisor on what was happening in the markets, what people are worried about, and the predictions made by various investment pundits on the internet.

The topics ranged from:

- The U.S. Federal Reserve (Fed) is going to keep rising rates, and that will be painful for many investors.

- China's currency is going to take over from the U.S. dollar.

- The current volatility is the start of a massive crash.

- The global economy in going into a recession.

- The U.S. housing market is going to crash.

- There will be a continuous supply shortage.

The list of concerns could go on and on. Whether or not any of them come true, we all know that once investors let their emotions rule their investment strategy, all is lost. As we have noted time and time again, much of the value that an advisor providestheir clients is preventing them from making the behavioral mistakes that can harm their portfolio.

Still, when markets are volatile, investors may not be soothed by the knowledge that markets go up 74% of the time1 or that they generally rebound – and rather quickly at that – from any downturn. They're convinced that this time it's different.

If this belief were actually true, then we should all begin to worry about other aspects of our life.

So, let's suppose we are on the brink of an apocalypse and the subsequent hardship that would bring. Here are three checklist items to prepare.

Water — There are three main methods of making water safe to drink:

- Boiling (water will need to be at a full, rolling boil for at least 5 minutes)

- Chemical purifiers

- Store-bought charcoal or ceramic filters

Food — You will have to find your own sources of sustenance:

- Trapping

- Hunting

- Foraging

Shelter — Crucial for keeping you warm and concealing you from predators. Here are a few tips to build your camp:

- Avoid anywhere the ground is damp

- Avoid mountaintops and open ridges where you are exposed to cold winds

- Avoid being in the bottom of narrow valleys which are colder at night

- Avoid ravines or washes where water runs when it rains.

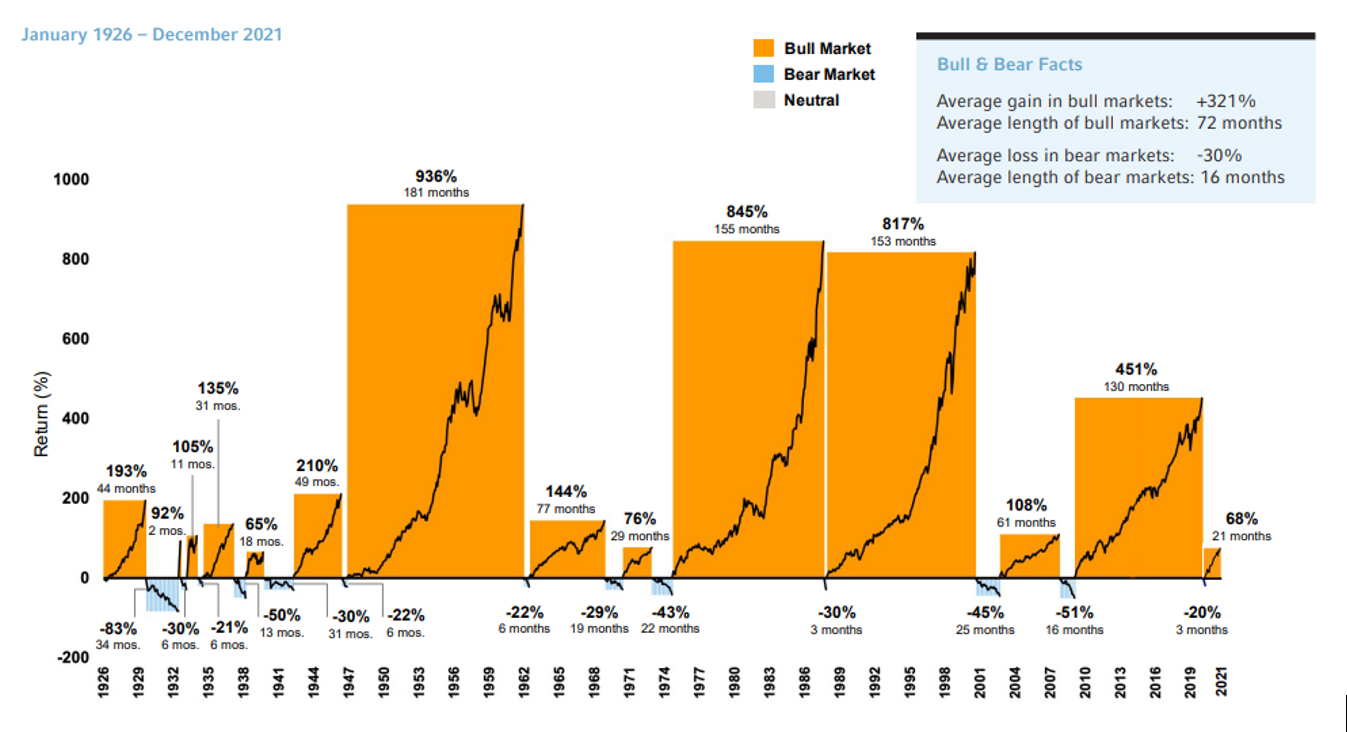

When you look at this list, a market crash seems a lot more survivable, doesn't it? That's because it is. Markets have had significant downturns in the past and as the chart below shows, they always bounce back eventually.

Click image to enlarge

Sources: U.S. Equity – BNY Mellon, Refinitiv DataStream, Russell Investments. Returns based on S&P 500 Index. Indexes are unmanaged and cannot be invested in directly. Returns represent past performance and are not a guarantee of future results and are not indicative of any special investment. As of December 2021.

Just like you can prepare for an apocalypse, you can help your clients prepare for a potential market crash. When it comes to investing, there are three things that are in our control: Taxes, Asset Allocation, and the investment plan.

- Taxes (the biggest mistake your clients can still make this year)

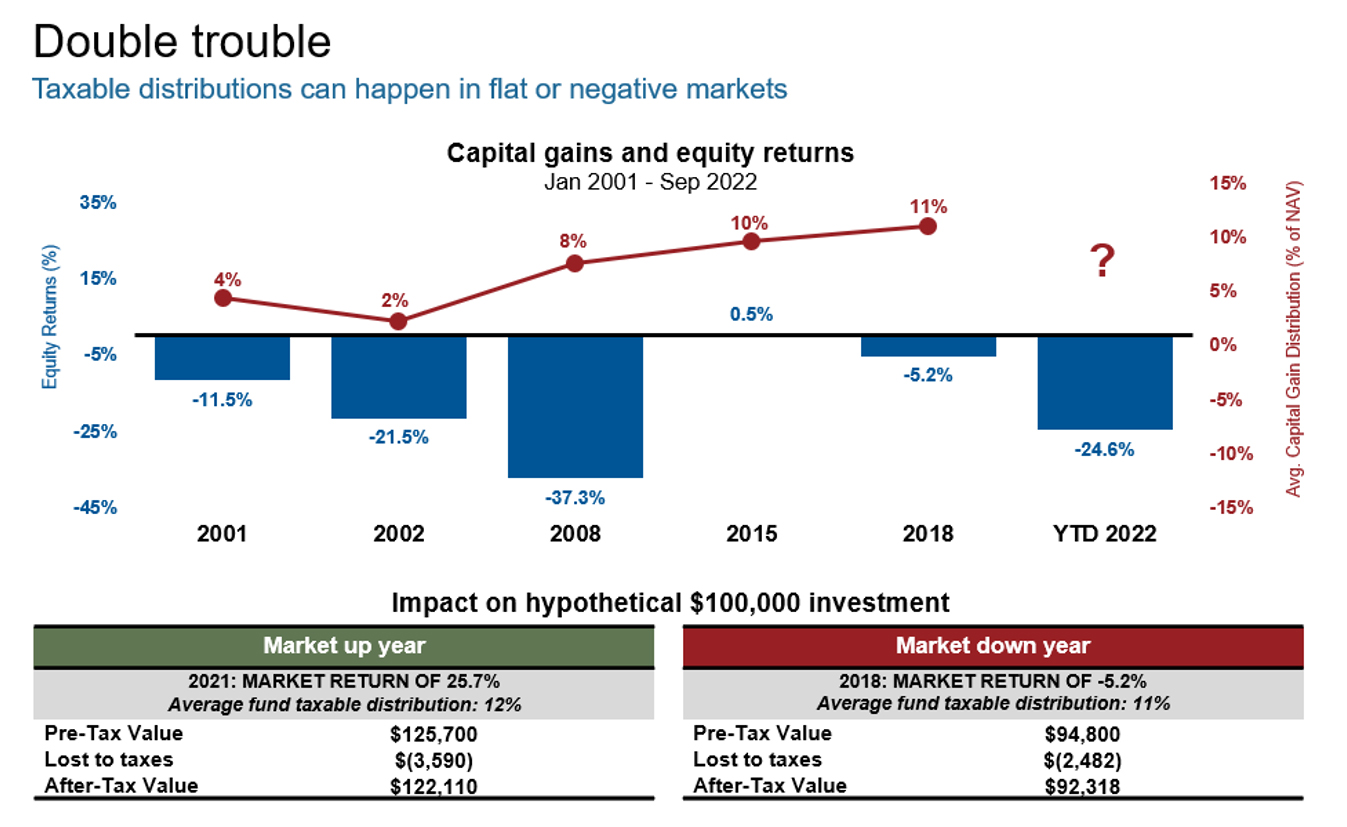

There is a common myth that if the markets are down, the tax bill on investments will be lower. Historically, that has not been the case. As you can see from the chart below, capital gains distributions have been made every year since 2001 regardless of the market's performance. History doesn't repeat but it might rhyme.

Not many people like to pay more taxes than they have to. You, the advisor, can help your clients minimize the impact of taxes on their portfolios. In difficult times such as now, tax management makes sense. There's not much you can do about the volatility, the effects of inflation or rising interest rates, the geopolitical environment or the onset of winter, but you can help your clients lower their tax bill.

The outlook for the markets remains cloudy but as we have already discussed, that won't necessarily mean your clients won't receive capital gains distributions. Now might be a time to explore the potential benefits of tax-managed investing. To get a feel for how much of a difference a tax-managed fund could potentially make for a client, take a look at our Tax Impact Comparison tool.

Click image to enlarge

Source: Morningstar Direct. U.S. Stocks: Russell 3000® Index. U.S. equity funds: Morningstar broad category "US Equity," all other categories are based on Morningstar Category Group each including mutual funds and ETFs. For years 1990 through 2013, used oldest share class, 2014 forward includes all share classes. Average Capital Gain Distribution % = calendar year cap gain distribution ÷ year-end NAV (For years 2001 through 2020). Indexes are unmanaged and cannot be invested in directly. Returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. All data as of 9/30/2022 except 2022 Mid-Year capital gain distribution table which is as of 9/9/2022. Calculation methodology: Assumed starting hypothetical portfolio value of $100,000. U.S. equity market return applied to starting value to arrive at ending pre-tax value. Percent lost to taxes is the estimated taxes due divided by $100k. This amount is then subtracted from the ending pre-tax value shown to arrive at final after-tax value. Distribution is assumed to be made at last day of year and reinvested. Tax rate is 23.8% (Max LT Cap Gain 20% + Net Investment Income 3.8%).

- Asset Allocation

If realtors can say location, location, location, financial professionals should use diversify, diversify, diversify as our tag line.

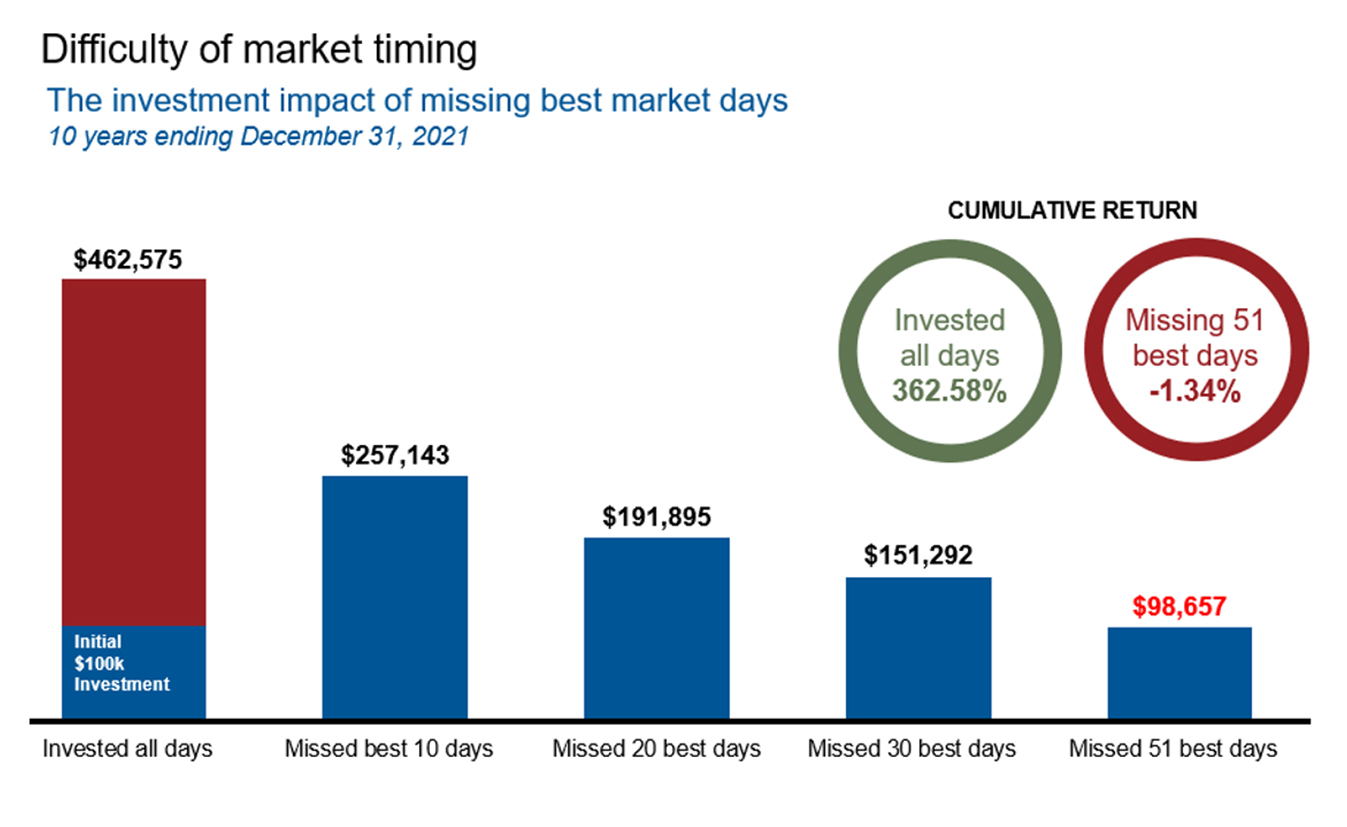

We all know we should be doing it, but how many practice it? From the many proposals we have run so far this year it's amazing to see how many investment portfolios are allocated 80-100% to US Large Cap equity. Sure, it was the place to be for the last decade or so, but will it be for the next? No matter what happens, diversification among asset classes and regions can help smooth out the ride. As we say, a smooth ride is an investable ride: clients are more likely to remain in the markets if their portfolios are less volatile. If they can't deal with the volatility, they might step back from the market. Then they might miss some of the best days, and as the next chart shows, you don't want to miss the best days. The thing is – we never know when it will be a good day or a bad day in the markets. Diversification can help keep your clients invested so that they don't miss any of the good days, while the bad days are potentially less bad.

Click image to enlarge

Source: Morningstar. In USD. Returns based on S&P 500 Index, for 10-year period ending December 31, 2021. For illustrative purposes only. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly.

Let us help check your client's diversification with a proposal or maybe one of these tools would be helpful.

- Build a Robust Investment Plan

A good investment plan requires a lot of work. It includes a robust discovery process and the selection of investments that align to your client's needs, goals and circumstances, then continues with regular reviews. And your services can encompass anything from succession planning to tax planning to the best way of leaving a legacy. But as you already know, the best investment plans can withstand the ebbs and flows of the market. That is the value you bring to your clients. Teach them about everything that you do for them, they might be unaware.

Let them know that their plan is about mapping outcomes for life.

They will have some bumps in the road and more bumps will come, but keep them focused on the outcome, and remember why they are invested. Remind your clients that the key to successful investing is to start as early as possible, be patient, and stick to their plan. As Warren Buffett says, "someone's sitting in the shade today, because someone planted a tree a long time ago."

As always, let us know how we can help.

1 Source: Russell Investments. Represented by the S&P 500 Index from January 1, 1926 to December 31, 2021.