Municipal bonds: Back to the basics

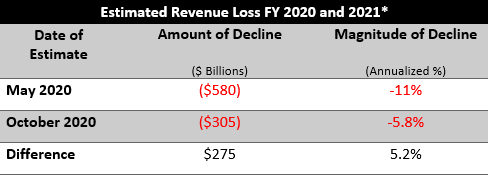

Starting almost a year ago, there has been a veil of negativity surrounding the municipal bond market, with concerns on how COVID-19 has impacted state revenues and the ability of issuers to make promised payments. In the chart below, estimated state revenues for fiscal year 2020 and 2021 were projected (as of May 2020) to be down $580 billion, or 11%.

When your investment’s ability to make promised payments becomes unclear, negative headlines are bound to stir up your emotions. However, as the dust began to settle, the estimates of revenue declines were reduced by half as of October 2020. Recognizing how embedded fundamentals have historically helped certain issues prevail during times of stress could help address some doubts you may be facing in the short term about this market. After reading, if you take away two things, I hope it is that some areas of the municipal bond market are more equipped to handle financial distress, and that taking an active approach is necessary to find these areas.

Source: Center on Budget and Policy Priorities

*Combined total of 2020 and 2021 divided by 2.

Municipal bond quality – Embedded fundamentals

Given concerns around government finances and the ability of states and municipalities to fulfill their debts, certain sectors and issuers that do not have the power to adjust their means of cashflow could see elevated defaults in 2021. However, we believe investors can look to three fundamental characteristics of the municipal bond market for reassurance. These characteristics have historically helped preserve not only credit quality, but defaults, and should play a large part in managing how the municipal market navigates 2021.

1. Monopolistic power & reliable cash flow

In general, certain municipal bond sectors have safety levers they can pull to continue making promised payments to bondholders. As long as payments are made, default rates tend to be regulated.- General obligation bonds (GO bonds): These generate cash flows from multiple sources of revenues like income and property tax, and are also backed by the full faith and credit of the issuing government. For these reasons, GO bond issuers provide steady payments, and in the event of a disruption in expected payments, municipalities have the power to raise taxes to meet obligations. Furthermore, under congressional mandate, GO bond issuers cannot declare bankruptcy.

- Revenue bonds: These are backed by public-service company fees (e.g., utilities and airports).The fees tend to be earmarked to service debt and most issuers have the flexibility to increase fees to make promised debt payments. On the other hand, if these issuers were private or in the corporate bond market, increases in fees would likely require approval from the board and shareholders.

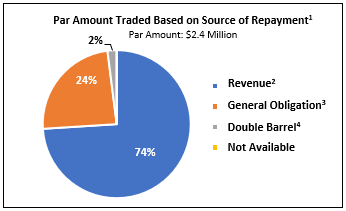

Since GO bonds tend to be seen as a more secure way of municipal bond investing, activity in this sector was muted in 2020. Revenue bonds are riskier as repayment uncertainty is more elevated, which could explain why there was so much activity in the sector in the year. As you can see below, revenue bonds have accounted for 74% of the trading activity in the municipal bond market. This means that for those investors who traded away their revenue bond holdings, there are investors on the other side buying at a discount who understand that the municipal market has levers in place to support riskier revenue bond issuers.

Source: Municipal Securities Rule Making Board (MSRB). Data as of 1/1/2020 – 12/31/2020

https://emma.msrb.org/MunicipalTradeStatistics/ByTradeCharacteristic.aspx

https://emma.msrb.org/EmmaHelp/UnderstandingMarketStatistics#sourceOfRepaymentAnchor

Both GO and revenue bonds have the potential advantage of offering more flexibility than privately owned issuers (i.e., privately owned utility companies and corporate bonds). This is one reason why municipal bonds have illustrated lower default rates over the last 15 years relative to privately owned and corporate issuers.

2. Essential services & everlasting existence

Most of the $3.9 trillion in outstanding municipal bond issues back essential services (roads, bridges, schools and transportation). These are services that are imperative to run a municipality, and are therefore likely to be supported by government funds in time of stress. Furthermore, most issuers have a corner on an aspect of day-to-day life. When looking at this through a wide lens, ask yourself … what would it take for roads, bridges and other means of transportation to no longer need funding? It would likely require a seismic shift in our lifestyles. Granted we have seen large changes since 2020, but funding is still needed in these areas for years to come.- Utility bonds tend to be a safer sector within the municipal bond market, and in addition to what was discussed above, these issuers are imperative to our day-to-day activities and well-being. These issuers are not only supported by the ability to increase taxes and fees, but they also have additional government support that can be directed their way in case higher fees and taxes don’t fill the void.

- Transportation bonds are used to finance local public transportation projects (transit systems, toll roads and airports) and are considered to be riskier than public utility issues, although they should be considered essential for the foreseeable future. However, when a crisis impacts their ability to generate revenue, their ability to make bond payments come under pressure. As with GO bonds and safer utility bonds, depending on how important the service is to the community, additional support could be warranted from higher levels of the government. For instance:

- Government tax revenues could be directed toward keeping transit system and state highway bonds afloat until revenue generation returns to normal levels.

- Additionally, issues like state highway bonds can rely on toll revenue, as well as certain budget changes—such as increasing the gasoline tax—to supplement any revenue that has been lost.

In the two examples of transit systems and state highways, the impact on revenues could be mitigated by income offered from more reliable areas, not to mention government backing. Once investors are able to see this opportunity, yields could become more normalized and prices could be driven higher.

3. Strong legal pledges

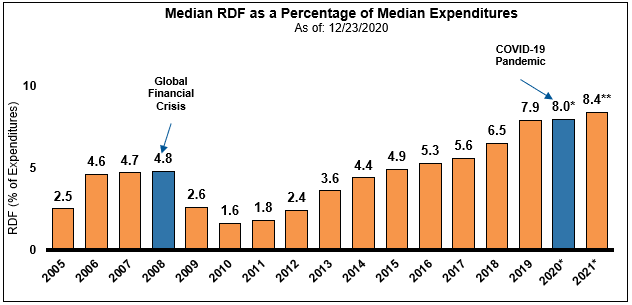

Since the Global Financial Crisis in 2008-09, minimum balances of rainy-day funds (i.e., emergency reserves), which vary by state, were put in place. This bucket of money is earmarked mainly as a safety net to municipalities during financial crises. In the chart below, you can see that rainy-day funds (RDF) have grown exponentially since 2008. Said another way, municipalities have experienced crises before and had strong snap backs, even with a lower level of emergency reserves.

Click image to enlarge

Source: Rainy Day Fund Growth: National Association of State Budget Officers. *2020 fiscal year figures estimated, **2021 fiscal year figures projected based on governors’ recommended budgets (Both Pre-COVID-19). Figures for fiscal 2020 and fiscal 2021 exclude Oklahoma and Wisconsin.

The bottom line

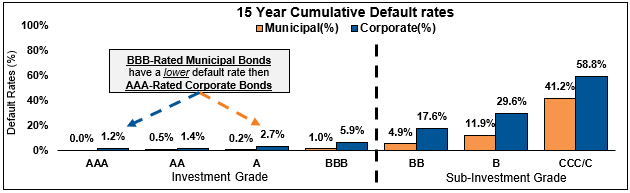

When you couple the three supporting factors with the potential investment benefits offered by municipal bonds, you come away with the following potential advantages: Fundamental drivers have helped the municipal bond market offer attractive rebounds historically, as seen in the chart below. Additionally, municipal bonds have generally carried lower default rates relative to corporate bonds. Investment grade corporate and high yield corporate defaults have been 12 times and three times, respectively, more frequent than comparable municipal bonds.

As an investor, municipal bonds could offer you tax-exempt income which can carry more attractive advantages if current tax rates increase, and higher income-generating capabilities after accounting for tax. Don’t let market-wide panic disrupt your investment plan. At Russell Investments, we believe investors should rely on active management to navigate times of uncertainty.

Click image to enlarge

Source: Standard & Poor's (S&P). For municipal defaults, S&P’s study period was Jan. 1, 1986 to Jan. 1, 2020. For corporate defaults, S&P’s study period was Jan. 1, 1981 to Jan. 1, 2020. The calculation period represents a 15-year cumulative default rate. CCC/C includes all ratings in the C category ranging from CCC-C rated bonds.

1: Par – amount of municipal transactions based on the source pledged by the issuer for repayment of the securities, according to definitions provided by Standard & Poor’s Securities Evaluations, Inc. If no information is available, “Not Available” will be displayed.

2: Revenue – a security that is payable from a specific source of revenue and to which the full faith and credit of an issuer with taxing power is not pledged. Revenue bonds are payable from identified sources of revenue and do not permit the bondholders to compel taxation or legislative appropriation of funds not pledged for payment of debt service.

3: General Obligation – a security that is secured by the full faith, credit and taxing power of an issuer. General obligation securities issued by local units of government are typically secured by a pledge of the issuer’s "ad valorem" taxing power; general obligation securities issued by states are generally based upon appropriations made by the state legislature for the purposes specified.

4: Double Barrel – a security with characteristics of both revenue and general obligation instruments.