2023 Year in Review

As 2023 draws to a close and we look back on how markets evolved, several major developments and surprises have occurred.

If we draw our minds back to the start of 2023, economists were almost universally concerned about recession risk. The Philadelphia Federal Reserve’s Survey of Professional Forecasters showed that the proportion of forecasters expecting a recession was at historical highs. We also thought that recession risk was elevated given how much the Federal Reserve had tightened interest rates but were cautious about reducing risk too aggressively, given the uncertainty around that.

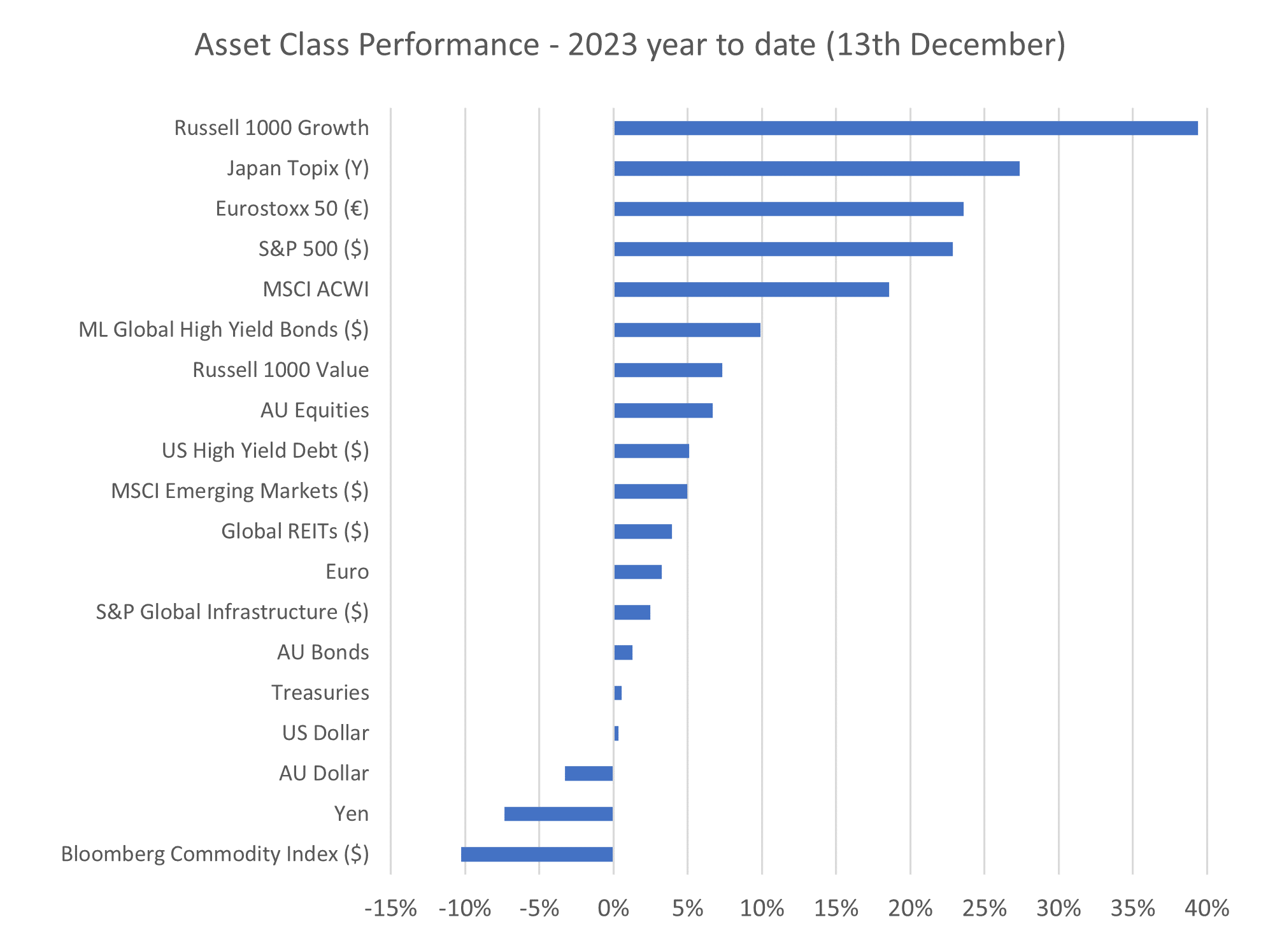

Today, global equity markets (using the MSCI All Country World Index as our proxy) are nearly 20% higher for the year. Growth companies have significantly outperformed value companies in the US, which has been driven (again) by megacap tech names.

Source: LSEG Datastream, 14 December 2023

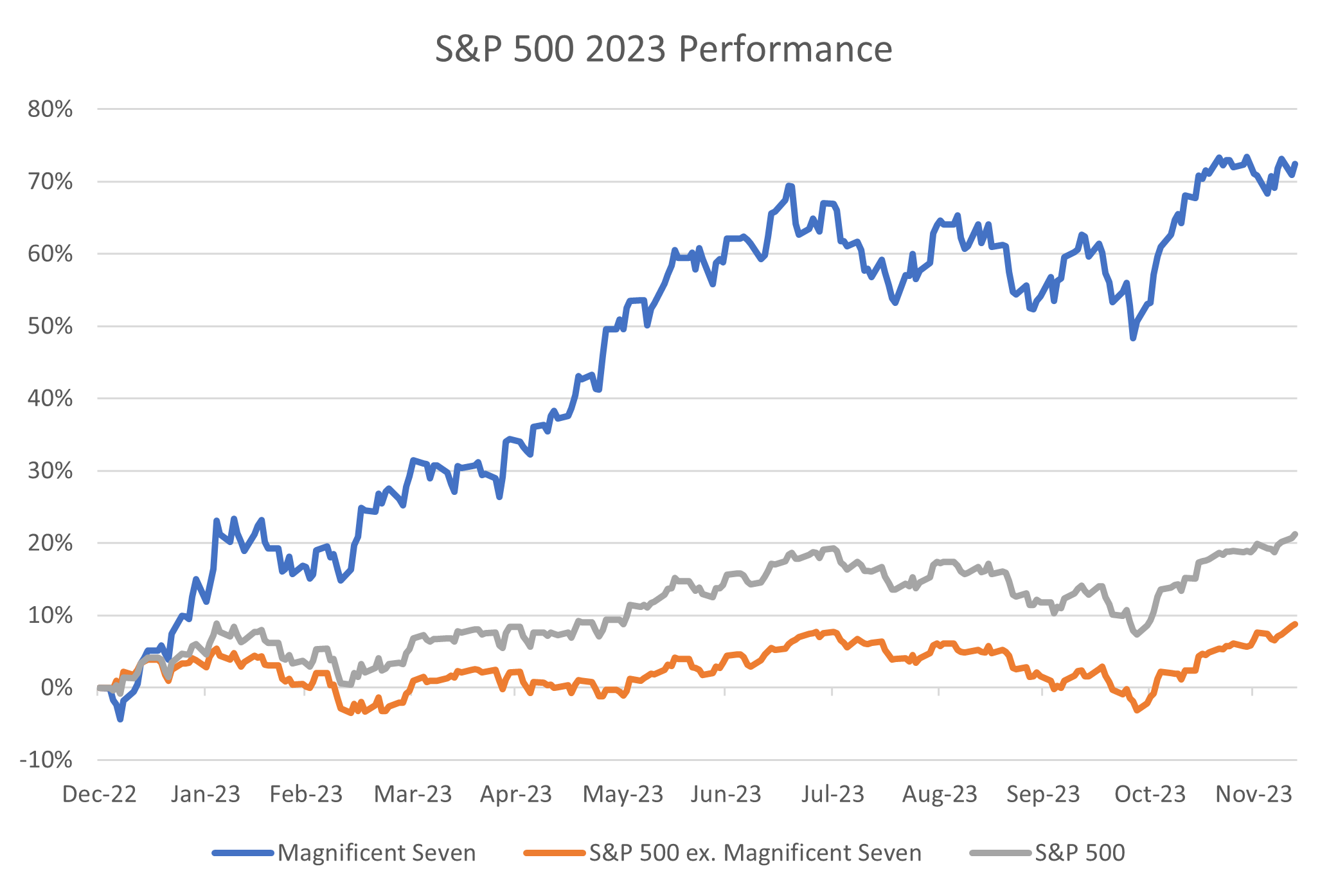

Indeed, the magnificent seven (Nvidia, Apple, Alphabet, Amazon, Microsoft, Meta, Tesla) have accounted for more than half of the S&P 500 return this year on the back of excitement around the potential for Artificial Intelligence after the release of ChatGPT earlier in the year. We think that AI will provide a significant boost to productivity in coming years that will likely align with what was seen during the introduction of electricity and the early internet.

Source: LSEG Datastream, 14 December 2023

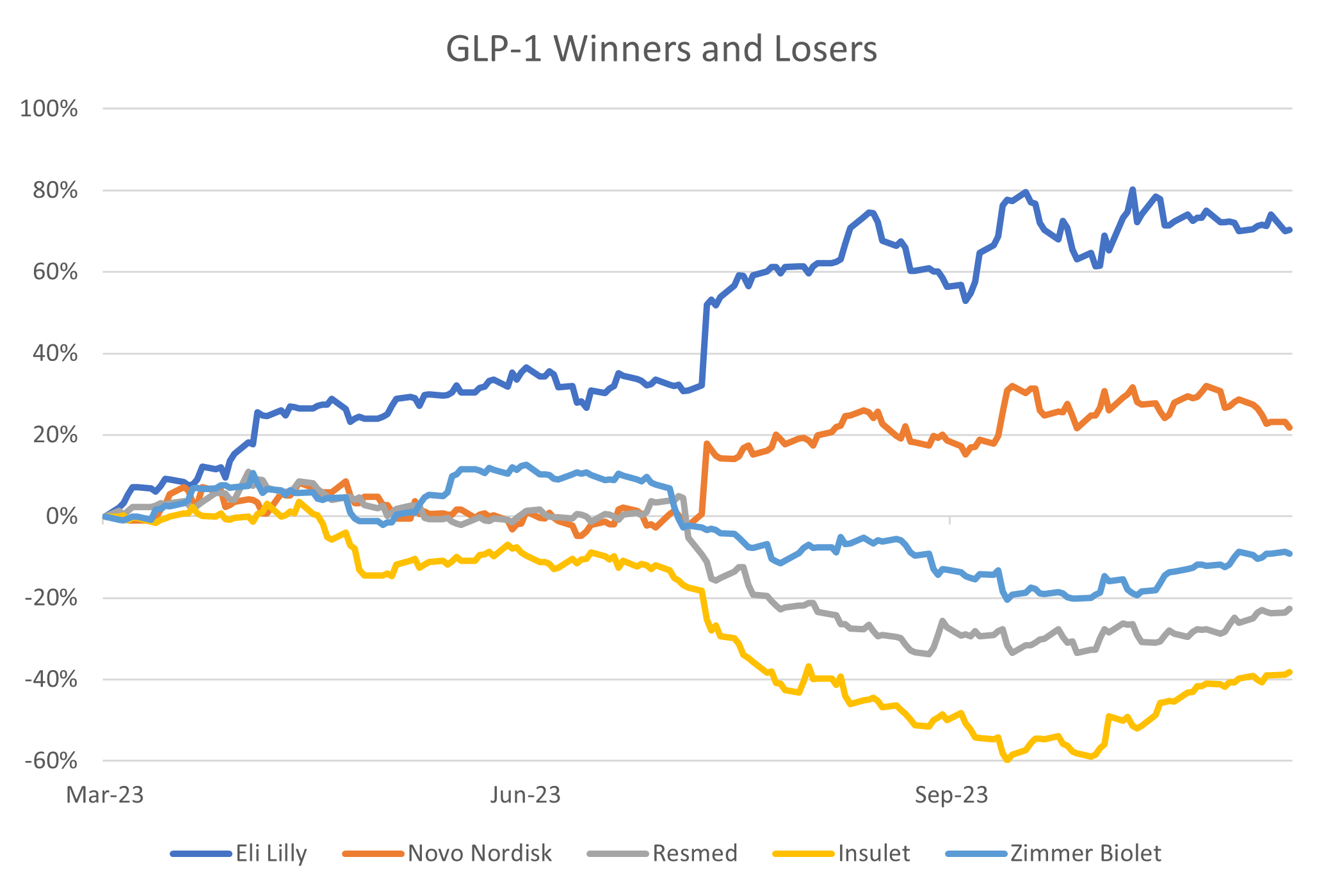

The rise of weight loss drugs

The other thematic that gathered a lot of excitement was the GLP1 drugs, such as Ozempic and Wegovy, which have been shown to boost weight loss significantly.

The chart below shows the share price performance of the ‘winners’ of GLP1 – namely Eli Lilly and Novo Nordisk- and the ‘losers’ – which include Resmed. This has dragged our Australian equity performance down as some of our hired managers have been overweight Resmed. We believe that the market has overestimated the potential impact of these GLP1 drugs on our companies, and we believe that our Australian equity portfolios are well-positioned for the year ahead.

Source: LSEG Datastream, 14 December 2023

Interest rates and bonds

The final developments have been in interest rates, the bond market, and the stock-bond correlation.

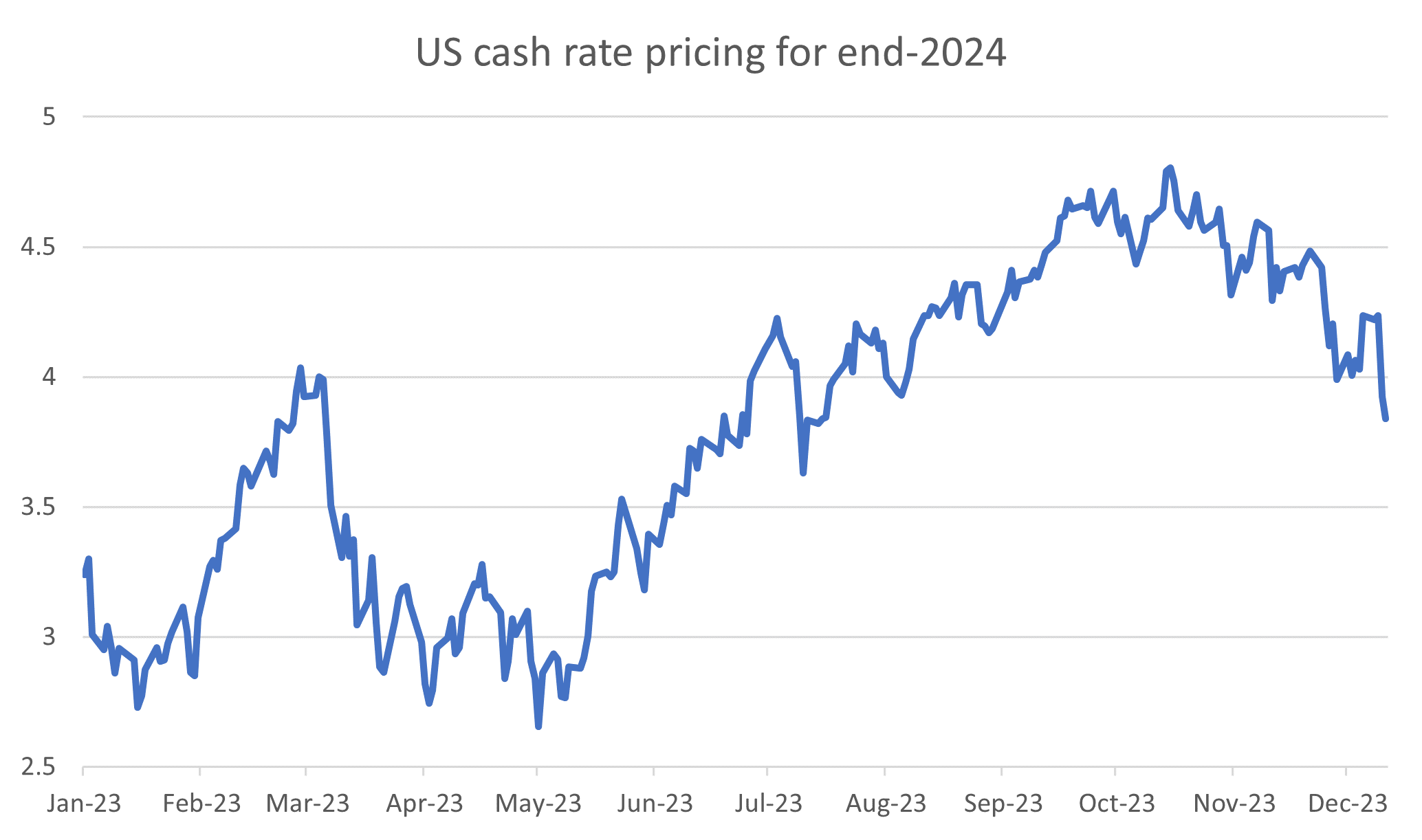

Over this year, central banks have raised rates by more than expected as inflation proved more stubborn in the first half of the year. That said, the Federal Reserve ended the year with a more balanced update – hinting at the potential for three rate cuts in 2024 and highlighting concern about the risks of keeping rates too high for too long. The chart below shows the market pricing for the Fed Funds rate for the end of 2024 and illustrates the volatility and uncertainty evident throughout this year.

Source: LSEG Datastream, 14 December 2023

We have believed for some time that government bonds present an attractive investment opportunity, and we continue to think that is the case. Valuations look attractive in most developed markets, and our concerns about weaker economic growth are a positive tailwind. Additionally, as we wrote in our recent Global Market Outlook, we believe that government bonds will reassert their role as a diversifying asset if we see equity market volatility next year.

Honing in on Australia, we think that recession risk is lower than the northern hemisphere. The recently announced migration reduction will provide less of a buffer but is still a buffer, nevertheless. Additionally, there will be some fiscal support through the second half of 2024 as the stage three tax cuts are implemented, and the potential for some other measures, given the budget balance has been running ahead of expectations. The RBA are likely to return from their extended Christmas break and leave rates on rate for the first half of 2024.

Looking to 2024

One of the most common questions is, ‘What keeps you up at night?’. As we approach 2024, there are a couple of key watchpoints and events.

- Will the United States economy enter a recession? We believe that recession risk is elevated and will be closely looking for signs of fragility.

- The US election in November – historically, US elections do not matter much to markets. However, Trump’s potential candidacy could create some volatility.

- Taiwanese election in January – based on polling, the incumbent DPP looks likely to win the presidency but lose the legislative Yuan, which would lock in a status quo outcome regarding China-Taiwan relations.

- Does China’s consumer confidence rebound on the back of more policy support from the government? China’s property market continues to struggle, which has weighed on the consumer. China’s government has been releasing several new policies, and we will be looking to see if they gain traction.

- The strength of the Australian consumer and the direction of fiscal policy – we have seen about 85% of the RBA’s interest rate increases flow through to households now as fixed rate mortgages have rolled off, and we will monitor the evolution of household spending through the first half of next year. We will also be looking to see whether the Labor government will spend some of the uplift they have seen in the fiscal position.