Momentum Investing: Buying Winners and Selling Losers

The popular adage when it comes to investing is "buy low and sell high". Another way many investors approach their portfolios is to "sell the winners and buy the losers", recycling capital from winning stock bets to average in on stocks that have not been successful. Whilst this sounds like a good strategy, in practice, and especially in Australian equities, doing the opposite has been a winning strategy – buying winners and selling losers has historically generated strong excess returns for investors in the Australian stock market. This is the basis of momentum investing.

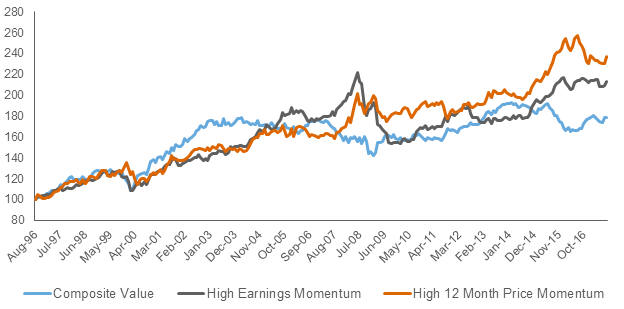

For example, comparing a portfolio of high momentum stocks and a portfolio of high value (i.e. cheap) stocks in Australia shows that the return to high momentum stocks is strong, and has historically outperformed the return from a portfolio of value stocks.

Cumulative Excess Return - Momentum and Value Factors in Australia

Source: Russell Investments, UBS

Russell Investments has strategic beliefs about a number of factors in equity markets and how we expect them to perform through time1. Our belief on the momentum factor is that high momentum stocks will outperform low momentum stocks over a market cycle, and actually tend to outperform for most of a cycle. Momentum stocks are typically defined by relatively strong price performance over the past 12 months, or relatively strong recent earnings. Stocks in the Australian market that are currently "high momentum" include Aristocrat Leisure, Boral, and Qantas. One way to explain the existence of the momentum premium through time is behavioural, in that investors tend to show herding behaviour and have a “fear of missing out” on stocks that have been appreciating in value.

Due to our belief in the momentum premium, our equity funds are generally exposed to an allocation of high momentum stocks through a market cycle in order to harvest this expected excess return stream. As can be expected when buying a portfolio of stocks that have performed well (and are generally expensive), momentum portfolios can be volatile and subject to “momentum crashes”. As such, it is important to dynamically manage allocations to these high momentum stocks. To do this, we look at three broad indicators. Whilst valuation is a key decision-making input for any investment decision, it is also important to consider where we are in the economic cycle as well as gauge market sentiment.

Rolling 12 Month Excess Return - Momentum Stocks can be Volatile

Source: Russell Investments, UBS

Cycle

In order to measure where we are in the cycle and how this affects different segments of the market, we look across three categories of indicators in earnings, economic, and policy. Overall, we see these signals as currently neutral on momentum as we do not expect material change in the outlook for earnings in the market for the next 12 months, nor do we expect substantial changes in the economic and policy environment for Australia in the near term.

Valuation

We currently see the aggregate value metrics on a portfolio of high momentum stocks as modestly attractive, across a combination of asset- and earnings-based measures relative to the market, as well as relative to each individual stock’s history. Comparing valuations relative to history helps us further understand how the market has historically priced different market segments. For example, a stock or sector may be expensive on a P/E (Price Earnings ratio) basis relative to the overall market at a point in time, however relative to its historical P/E range it may be cheap.

Sentiment

Sentiment signals are more technical in nature, and look at how the market’s behaviour can help us make informed timing decisions of when to enter and exit (or increase and decrease) positions. Currently, we see sentiment for momentum is slightly positive. Momentum stocks have started to perform well this year after being aggressively sold off in the second half of 2016, however on a 12-month basis (which is a key timeframe for sentiment), momentum stocks are not yet showing strong metrics. One positive sentiment signal is that there is a good amount of breadth amongst the recent performance of momentum stocks.

After the market’s rotation last year which saw momentum stocks dumped and left behind in favour of value stocks, we view the current market as an attractive entry point to begin incrementally adding back exposure to high momentum across our Australian equity funds.

1https://russellinvestments.com/au/insights/library/inside-smart-beta--making-sense-of-investment-factors