Complete your portfolio with the X factor

Scott Bennett, Director, Equity Strategy & Research, Investment Division at Russell Investments explores how you can use a portfolio completion solution to correct biases in your portfolio exposure.

Factor exposure

Factor exposure is growing in relevance for institutional investors, who are finding themselves under increasing transparency and cost pressures.

But thankfully, getting these exposures into your asset allocations and funds is not as hard as it seems at first. In fact, it can be quite straightforward and can result in some unique and differentiating allocations.

Essentially, a factor - and I agree with Google here - is "a circumstance, a fact or an influence that contributes to a result or outcome". In relation to investments and what we do particularly with equity investments, it still holds true.

Factor exposure was highlighted in a recent survey by the Economist of American institutional investors. The study found that 62 per cent of respondents either agreed or somewhat agreed with the statement that factor-based strategies can yield long-term outperformance relative to benchmarks.

However, only 47 per cent disagreed that factors are too complicated to use in everyday asset allocation. So there seems to be a bit of a disconnect between the opportunities available through factor-based investing and the ability to incorporate it into portfolios.

Natural tailwind

At Russell Investments, we have views on particular factors. We want to be overweight value, we want to be overweight momentum, we want to be overweight quality, and we want to be neutral on volatility. These are our beliefs. This is what we want to embed in our funds to provide as much of a natural tailwind as possible.

But how can we embed those beliefs in our funds while allowing the underlying managers to freely roam the full investment habitat? For a Russell Investments' equity portfolio, it would look something like the following chart.

Dynamic completion portfolio

When we set up a portfolio, we set our strategic beliefs then identify managers and combine them in a way that fulfils those beliefs. We also embed a lot of conviction.

We then need to manage those allocations, as managers change, their staff and portfolios change, and different factors, sectors, regions and countries come into play. Active risk levels are not static either. There are times when certain exposures present a really good opportunity and there are times they present significant challenges.

Centripetal force

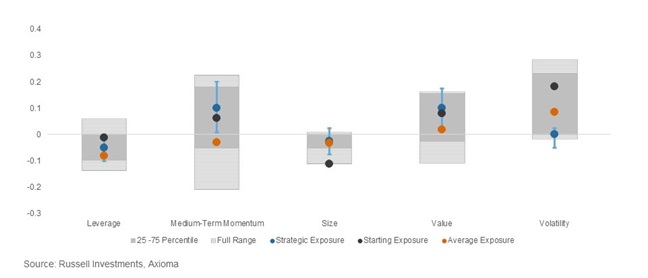

So, how do we allow the managers to find their best ideas and get those best insights into the funds without running off the road? The answer is to ensure we have a centripetal force (a force by which bodies are drawn or impelled, or in any way tend, towards a point as to a centre1) in the portfolio to make sure we stay on track, given we're going at such fast speeds. That's how I like to think about a dynamic completion portfolio.Dynamic completion portfolio factor exposure ranges

If we were to build a portfolio without any manager insight, ceteris paribus, the blue dots on this chart shows what it might look like. It would be underweight on leverage, also known as overweight quality. It would be overweight momentum, slightly underweight size, overweight value and neutral on volatility.

However, this chart represents an actual portfolio that was set up in 2007 for our US investors. The orange dots represent our average exposures, the blue are our desired strategic exposures and the black are starting exposures of the portfolio.

In the chart, we can see that although the portfolio started with exposures consistent with our strategic preferences, the portfolio at times diverged materially from these strategic exposures.

At the heart of the issue is that while we want to allow managers the freedom to find high-alpha opportunities, we also don't want to be persistently caught on the wrong side of our own beliefs.

So what we need is a way to counterbalance when these active strategies seem to be hurtling in one direction or another on a particular factor. We're able to do that through the dynamic completion portfolio.

Using a dynamic completion portfolio we set ranges for each factor (blue bars) then, through monitoring and managing, we can construct a counterbalance portfolio that doesn't change the manager positions and doesn't temper their bets. Importantly the dynamic completion portfolio is focused on identifying complementary positions that preserve the underlying active manager insights. This allows our total portfolio to capture both the underlying manager insights and our strategic preferences.

Setting up the process

Here's how we do it. The first criteria is to identify what exposures need to be managed. So we measure them. What gets measured, gets managed.

We have a very extensive process of identifying factors that we develop strategic preferences for and embed them in what we call a strategic benchmark, represented by the blue dots on the chart.

Then we build a complementary portfolio, not a plug. The use of a plug can be highly effective at reducing risk and for positioning the overall portfolio. However, plugs are very blunt instruments and by including a plug you can compromise the underlying stock selection from your active managers and serve to only dampen the excess returns. A plug represents a static allocation, it is not complementary and is usually conflicting (i.e. a manager is underweight REITs, so you plug that gap with a passive exposure to REITs).

Using a dynamic completion portfolio, we can look at the underlying factor exposures in that REITs allocation and manage them in a more complementary manner. That way we don't compromise any of the stock selection insights from the underlying managers.

The third component is monitoring and managing portfolios in real time so we can execute to rebalance them.

We have some clear examples of where we think factors can add value, but we also think you can customise those factors to your own experience. And we work with the largest institutions around the world to make sure we're getting them not just any factor but a factor that is relevant for them.

1 Definition attributed to Isaac Newton.