Evergrande ordered to liquidate

After first defaulting on its bonds in December 2021, Chinese property company Evergrande has been ordered to liquidate by a Hong Kong court. This has been a piece of news that the market has been largely anticipating, and indeed we saw Chinese equity markets largely shrug off the news. There is still an open question as to how it will be interpreted in China, given that most of the assets of Evergrande are in the mainland.

From an economics perspective, the first question to ask is what happens to the work that is currently underway. It has been the priority of the government and policymakers to ensure that pre-sold projects are completed, and suppliers are paid. It is very likely that we see a continuation of that focus, which mitigates the risk of a bigger impact on the real economy. The second question is the extent of contagion that this could mean, and here it is important to go through a couple of points.

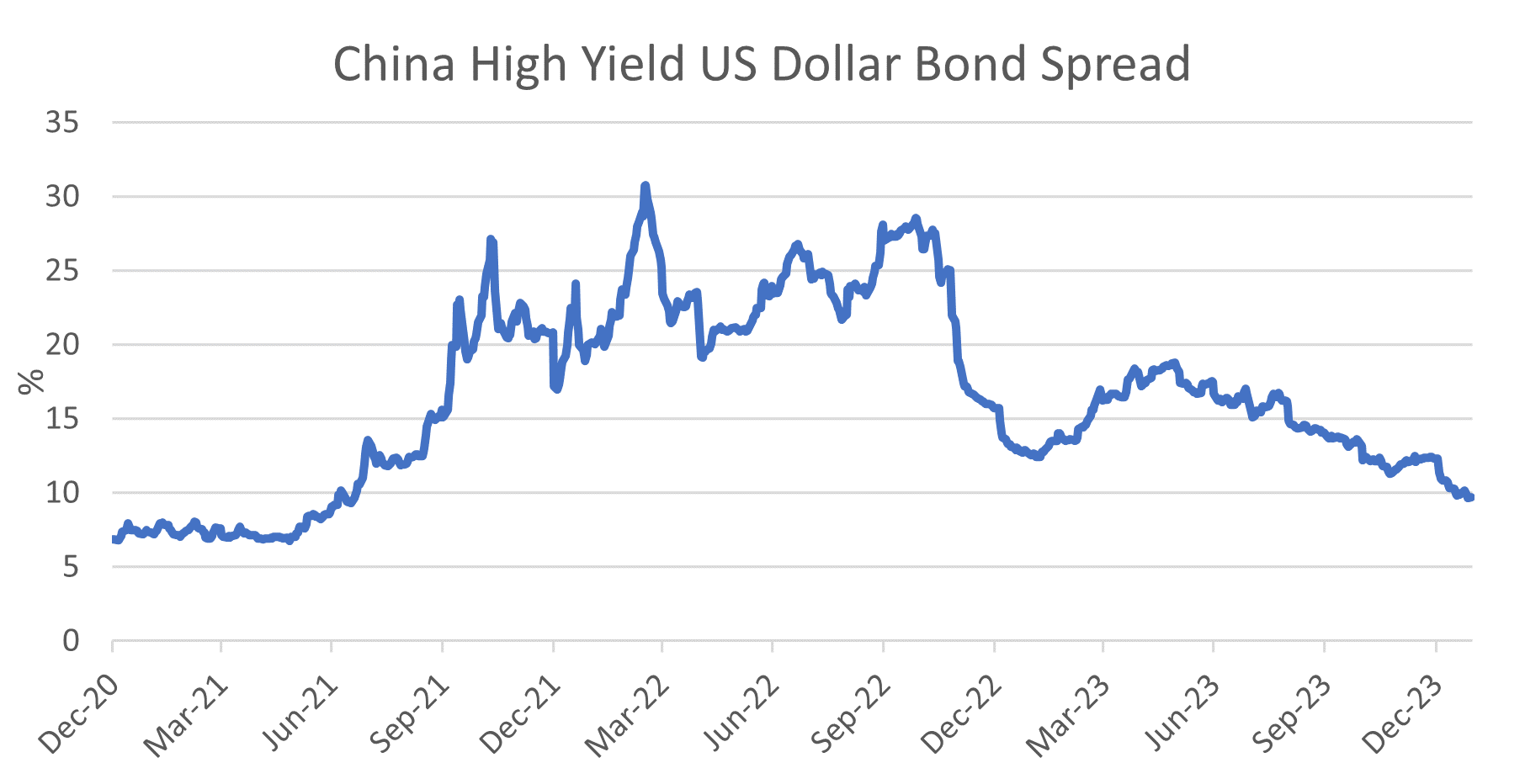

Firstly, much of the Evergrande debt has already been trading at levels that imply very little chance of recovery. Secondly, this pricing is also being seen in the broader real estate sector. The chart below shows the credit spread for Chinese high yield US Dollar bonds – they have been quite elevated for some time as the market has priced in the very soft property market and the impacts that has on property developers.

Source: LSEG Datastream, 30 January 2024

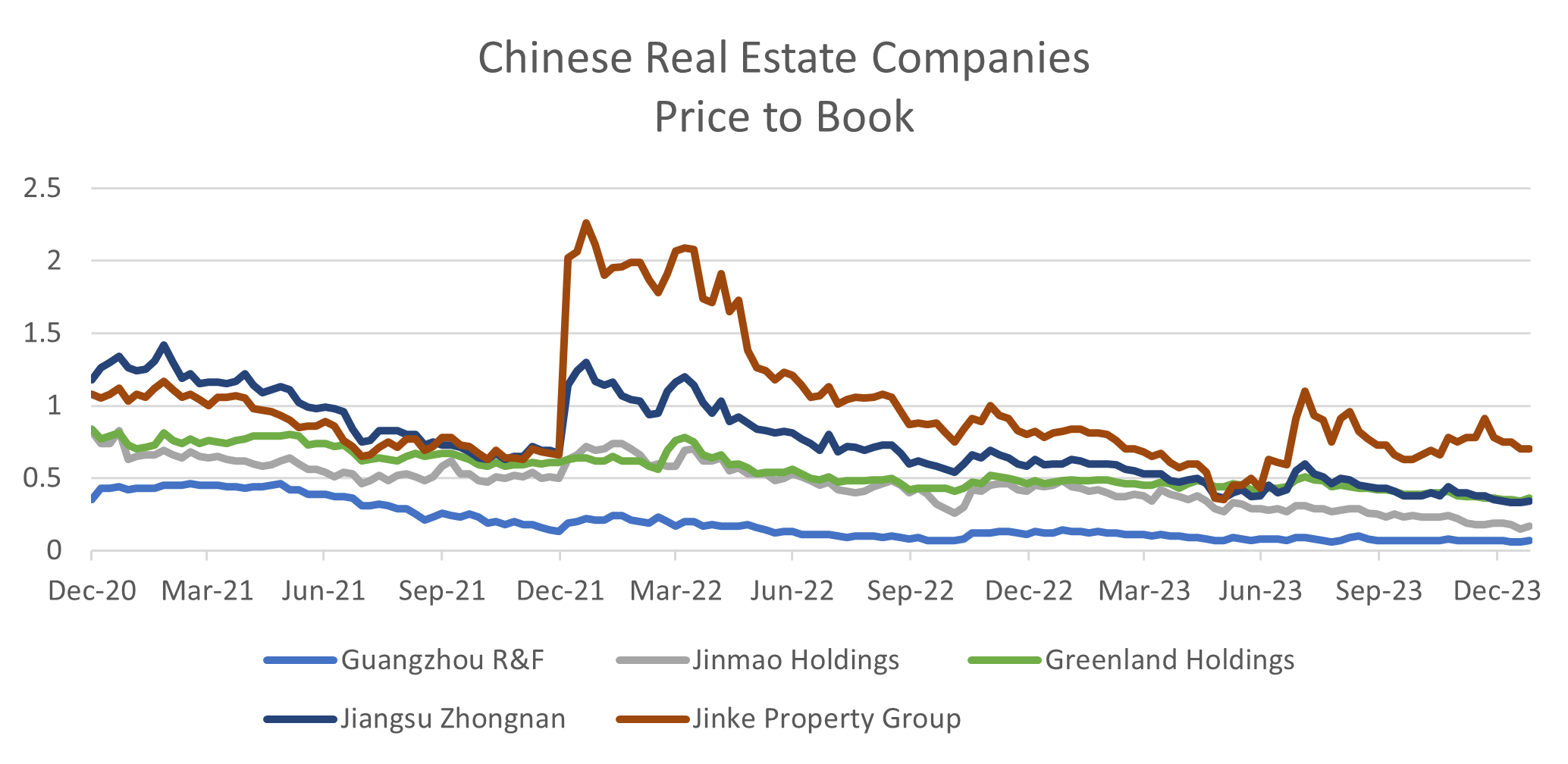

We have also seen equity markets discount Chinese real estate companies by quite a lot, with real estate companies trading at a price to book value of less than 1 i.e. less than the liquidation value of the net assets.

Source: LSEG Datastream, 30 January 2024

Ultimately, does Evergrande change the economic outlook for China in a meaningful way? We don’t think it does, largely because the market had already discounted that Evergrande would eventually be forced into a liquidation. At the margin, it may add to the headwinds that are facing the property market if we see discounted prices being offered for the assets. Our broader economic outlook for the Chinese economy right now is that economic growth is likely to be 4.5-5 per cent in 2024, but that will likely require some more stimulus from the government. In recent weeks, we have seen several policy announcements to support the equity market – we think that these are unlikely to be too impactful without broader measures to support the real economy. The Politburo meeting will be held in March, where the government are likely to announce the economic growth target for the year and any new stimulus measures.