Greenwashing and tips to identify suitable ESG products

There has been a marked increase in the demand for Environmental, Social and Governance (ESG) /Sustainable style products and this trend looks set to continue. Unsurprisingly many firms are seeking to capture some of this growth through the launch of new products, but also rebranding of existing funds. This has led to concerns of ‘Greenwashing’, which is the overstating of a product’s ESG credentials or misleading investors on how environmentally sound or ethical a fund really is.

The challenge for advisers is finding products that are most closely aligned with their clients’ ESG or ethical beliefs. It is rare to have clients with exactly the same beliefs or principles. This blog will suggest key steps and identify freely available resources to match genuine ESG products with investor demands.

What should an ESG product look like?

There are two key features that all ESG style funds should have:

- Negative screens or tilts – companies/industries that are excluded or held at underweight positions relative to the market

- Positive tilts – companies/industries that investors want overweight exposure to relative to the market

Negative tilts

Typical negative screens include fossil fuels, alcohol, and gambling. These industries can result in some form of harm, for example the burning of fossil fuels results in environmental (E) impact that is contributing to climate change. Similarly, alcohol and gambling can have negative community and social (S) impacts due to the potential damage on the health and wellbeing of individuals. In the Russell Investments Australian Responsible Investment ETF (RARI), we exclude stocks using all three of these criteria - Fossil Fuels, Alcohol and Gambling. This is a good example of meeting the first criteria of a sound ESG product above.

Source: Russell Investments

Positive tilts

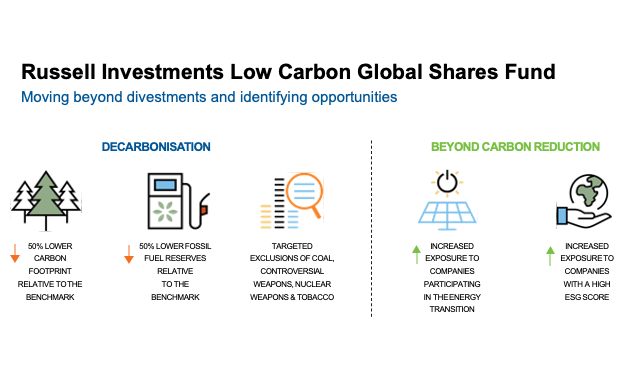

Positive tilts in ESG products will also often use Environmental or Social metrics to identify stocks to include in a portfolio and take an ‘overweight’ position. Examples include renewable energy, education, or health care. Another approach is to score companies across a wide range of ESG metrics – and then overweight stocks that have the highest aggregate ESG scores. This is the approach we use in RARI. In the Russell Investments Low Carbon Global Shares Fund we tilt positively to both ESG scores, as well as companies participating in the Green Energy transition.

Source: Russell Investments. The benchmark for this fund is MSCI ACWI ex Australia Index Net.

In the Russell Investments Low Carbon Global Shares Fund shown above, the negative tilts are shown to the left of the vertical dotted line and includes underweights to high carbon emitting securities, and outright exclusions of industries such as coal and tobacco.

The positive tilts are shown to the right of the dotted line. In addition to having higher ESG scores than the benchmark, the portfolio also overweights utility securities that use renewable sources to produce most of the power they generate (green energy). We believe such stocks are exactly the stocks a low carbon strategy should overweight since they are clearly positioning for the energy transition (the move away from fossil fuels to green energy to produce power). A good example of this is Danish utility, Orsted, that is held at an overweight and has been an important positive contributor to the fund’s returns. This illustrates the strong ESG credentials of the fund – clear negative screens and intentional positive tilts.

Responsible Investment Association of Australasia (RIAA)

Help is at hand for advisers overwhelmed by the deluge of ESG related marketing from investment providers. RIAA has an invaluable, and independent, source of guides that are all available on their website. Most importantly, they provide Product Certification for ESG products (found under the RI Certification section of their website) and a search function that allows advisers to identify what Certified Products match their clients ESG beliefs. If a product has the below certification, as RARI and the Russell Investments Low Carbon Global Shares Fund do, it should provide advisers with comfort that the product has genuine ESG credentials.

A 3-step check for advisers

When choosing the right ESG product for clients, ask yourself:

- Do the product’s negative screens match my clients’ beliefs?

- Are the positive tilts also consistent with the ESG themes that are important to them?

- Is the product certified by RIAA?

For example, if renewable energy/energy efficiency was an important positive tilt and the client wanted to avoid fossil fuels (negative screen), both of the Russell Investments funds highlighted in the blog would be deemed as suitable for a client using the RIAA search function.

How ‘Green’ is your client?

As highlighted at the start of the blog, investor demands around ESG criteria are often unique to them. Some clients are likely to want very hard exclusions and have nil exposure to fossil fuels and mining for example. Such a client might be evaluated as being ‘dark green’, i.e. their ESG beliefs are very hard and take precedence over missed investment opportunities.

When we designed RARI in 2015, we sought to produce a genuine ESG product that sat somewhere in the middle ground of the ESG spectrum. Whilst we exclude fossil fuels and have tightened this negative screen in recent years, RARI still has exposure to some mining stocks, for example Fortescue Metals which scores well on overall ESG criteria. We are also encouraged by the direction Fortescue is taking towards renewable energy. Similarly, we have not kicked bank stocks out of RARI after recent scandals, in part due to concerns the Russell Investments’ Responsible Investment Committee had around performance risks (of disposing of stocks when a lot of bad news had hit prices).

Products like RARI will not suit all ESG minded investors but it should meet the ESG expectations of most, and the RIAA Certification provides further reassurance of its ESG credentials.