Why downside protection may matter more than upside growth

This uncertainty presents a challenge for investors who are looking to generate attractive returns while preserving capital during market volatilities.

Against this backdrop, preserving capital may be more important than seeking the growth of capital, i.e. downside protection. It matters, because, in the investing world, losing less means requiring less to bounce back.

In fact, avoiding losses appears to be more important than achieving gains.

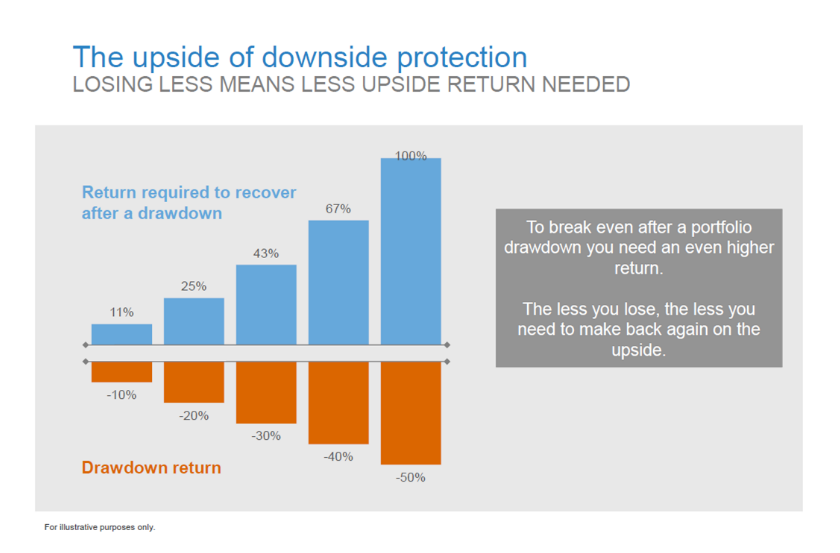

The following chart shows the historical returns required to recover after a drawdown.1 The returns investors need significantly increase as losses go deeper after a period of underperformance. A drawdown of 20% would need 25% to recover, whereas a drawdown of 50% would need 100% to regain ground. This example demonstrates that a dollar of excess return in a down market is worth more than a dollar of excess return in an up market. To achieve long-term growth, it is inherently important to not only grow the upside, but it is arguably even more important to protect the downside.

As data show, strategies that provide both potential upside and downside protection can help enable investors to weather market changes and stand better chances of outperforming benchmarks. With valuations inching higher, how can investors identify such opportunities? The key is through diversification.

In recent years, Russell Investments has consistently advocated for investors to consider a global multi-asset approach to investing for a variety of reasons, and the centre of it is around helping clients take a smoother path towards their objectives. While the objectives of multi-asset strategies may vary, some are designed specifically to help provide investors with better downside protection while providing the growth they require. A multi-asset approach can help achieve these goals through three main phases:

- Design: In the design phase of a portfolio, when asset allocations are established, a nuanced asset allocation may help to capture the things in-between core equity and bonds – such as bank loans, high yield debt, emerging-market local and hard currency debt, mortgage-backed securities, and other alternative strategies—that are not modeled in a traditional 70/30 fixed income and equity allocation. This differentiated approach to diversification is designed to deliver growth, and, perhaps more importantly, to minimise the big downward dips.

- Construct: When the portfolio is actually built, we believe a true multi-asset approach applies a wide network of skilled, active money managers who specialise in each asset class. This may be complemented by smart beta and passive exposures to seek to effectively manage the total portfolio. By spreading such a broad net for manager expertise—well, think of it as an additional layer of diversification to help against downside risk.

- Manage: After the portfolio is built, we believe a true multi-asset approach continues to dynamically manage that portfolio. This dynamism across asset classes is intended to help manage downside risk and gain exposure to high-conviction investment opportunities. This can include managing a portfolio of physical securities—such as stocks or bonds—or implementing overlay-based strategies such as options, currency forwards and futures.

Combining all these levers, a multi-asset approach may help investors with downside protection.

It’s understandable that so much of the world is chasing growth. Growth is enticing. But we believe savvy investors will focus on what the data tells us. And the data shows that protecting against downside just may get you more bang for your buck.

1 This was calculated using mathematical principles of percentages. For example, a 10% loss of $100 is $90. An 11% gain—or an additional $10—is needed to go from $90 to $100. A 20% loss of $100 is $80. A 25% gain—or an additional $20—is needed to go from $80 to $100