Missing the Forest for the Trees Why Valuation Matters

All aboard the bandwagon

At Russell Investments, we believe there are three primary forces that drive financial markets: cycle, valuation and sentiment. Cycle refers to the market cycle of peaks and recessions in an economy or in a specific financial market segment. Valuation refers to the worth of an asset class, in comparison to market norms. And sentiment refers to the feeling, or attitude, of investors toward that specific portion of the market.

In the short-term—let’s say within twelve months—we believe that typical market behaviour can be attributed to each of these three factors along the following percentages:

- Cycle: 40%

- Sentiment: 40%

- Valuation: 20%

Sentiment is a powerful market driver, and we believe that it’s a primary force driving U.S. equities today. As human beings, we tend to focus on trends. If something is going up, everyone piles on. We find it hard to resist the pull of momentum and go against the grain. This is investing herding behaviour at its most basic level.

In our view, cycle is another major factor in today’s market. The better things get, the more people take notice and jump on the bandwagon, and the more the cycle extends.

As a result, we believe that we are in a late-cycle, momentum-driven market—especially in the U.S., where equities have been expensive for years. Sentiment continues to push prices upward, while the business cycle breathes further life into the current market peak. But how much higher can the peaks rise, before we drop toward the valley floor?

Today’s valuation asymmetry: Is it worth the risk?

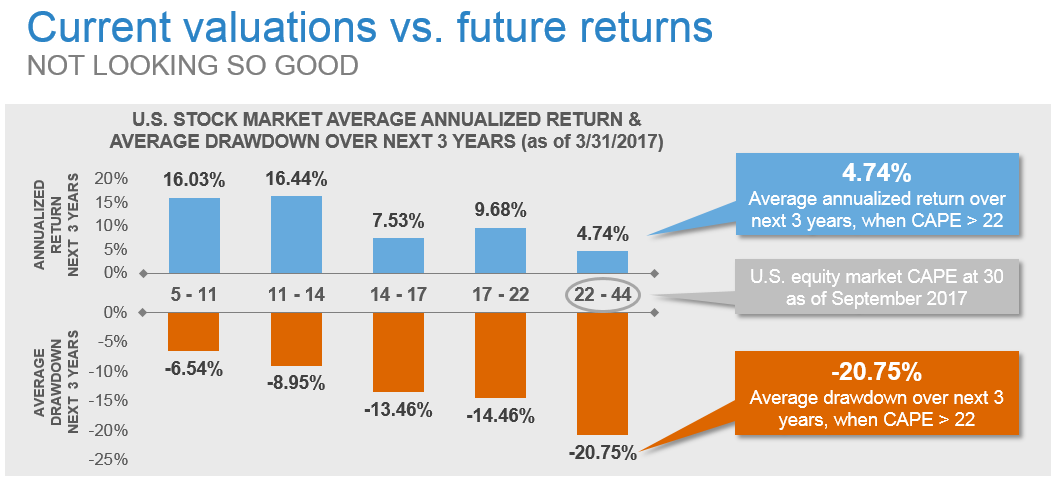

If cycle and sentiment have pushed the U.S. equity market so high, then looking at the valuation of that market becomes even more critical. The following graph shows that, for U.S. equities, historically when the market has been in the 20% most expensive range, the average future return has only been 4.74% over the next three years. In contrast, the average maximum loss in that same timeframe has been -20.75%. In our view, that’s a lot of risk for minimal gain. Put another way, the bar to overweight U.S. equities in the short term is extremely high. The juice simply isn’t worth the squeeze.

Source: http://www.econ.yale.edu/~shiller/data.htm 1

We believe that when valuations become asymmetrical like this, a long-term outlook becomes much more important than a short-term one. In our view, it’s better to give away a little on the upside in the here-and-now than risk losing too much on the downside. This is why we recommend zooming out of the typical one-year time horizon and focusing instead on what’s likely to happen in the next three to seven years. Taking a step back from the giant Redwoods and picturing what the rest of the forest could look like down the road.

Valuation: King of the long-term

If you look out beyond a few years, the importance of valuation becomes far more apparent. This is because within a seven-year time horizon, we’re usually likely to experience an entire market cycle, an entire credit cycle and an entire economic cycle. So, cycle becomes far less important. Likewise, sentiment loses almost all of its significance. Trends die, and sentiment, after all, is the very definition of ephemeral. Beyond seven years, valuation truly is king.

The conclusion? We believe that a significant, short-lived market pullback could occur in the near future, given current valuations and the current market complacency. Mean reversion theory has demonstrated this time and time again. Already, we believe that cycle and sentiment are long in the tooth in their support of U.S. equities. Because of this, valuation for this segment may become more and more paramount—not solely in the long-term, but in the short-term as well. Strategies that identify pockets of value—i.e., hunting for bargains and overlooked assets that have upside—may be the key to protecting the health of your portfolio. At Russell Investments, for instance, we recommend underweighting U.S. equities and focusing instead on European and emerging markets.

We know it’s easy to be tempted by short-term focus and market momentum. Sentiment and cycle urge us to jump on board, to hitch our wagons to today’s sky-high U.S. equities. But we believe it’s not worth it. And valuation agrees with us.

1 Yale Professor Robert Shiller calculates a Cyclically Adjusted P/E Ratio based on stock price divided by prior 10-year earnings. U.S. stock market is represented by an index created by Professor Shiller. The stocks included are those of large publicly held companies that trade on either of the two largest American stock market exchanges: the New York Stock Exchange and the NASDAQ. Prior to 1926 his data source was Cowles and Associates Common Stocks Index, after 1926 his source has been S&P. Index returns represent past performance, are not a guarantee of future performance, and are not indicative of any specific investment. Indexes are unmanaged and cannot be invested in directly. Forecasting represents predictions of market prices and/or volume patterns utilising varying analytical data. It is not representative of a projection of the stock market, or of any specific investment. Average drawdown is the percentage return from period start date to the market trough within the subsequent three years.