Federal Budget: May 2026

This summary provides commentary on the economic view of the Federal Budget announcements and highlights key changes for investors, advisers and members, particularly in superannuation.

The 2026-27 Federal Budget was delivered with the backdrop of geopolitical tensions, higher oil prices, stubborn inflation, three consecutive RBA interest rate increases, and a national economy that has suffered from a prolonged patch of poor productivity. With this context, it is not surprising that the Government positioned the Budget as targeting ‘Resilience and Reform’.

The Budget has delivered several key changes, with reforms focused on capital gains tax, negative gearing, a reduction in NDIS spending and a ‘Working Australian Tax Offset,’ which will see every working taxpayer receive a $250 income tax reduction from July 2027.

Many of these reforms are, of course, just proposals at this stage and will have to be passed in Parliament before they come into effect.

Key numbers

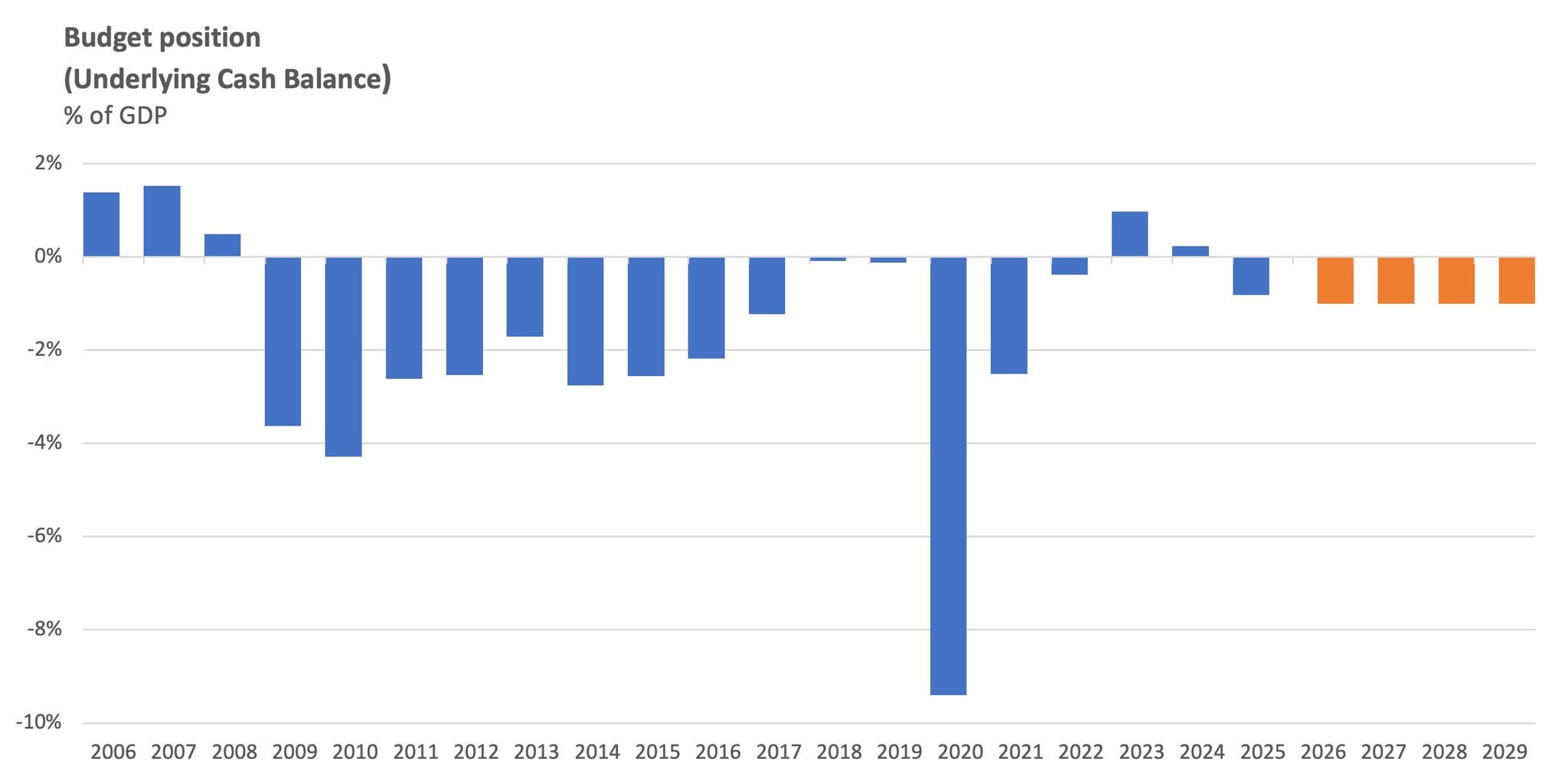

The 2026-27 Financial Year (FY26) is expected to see a fiscal deficit of 1%, which is better than what had been anticipated at the Mid-Year Economic & Fiscal Outlook. Looking further ahead, a set of similar fiscal deficits are expected. The fiscal impulse (i.e., the change in the size of the deficit) is zero in FY27, suggesting that the Federal Government will not be adding to demand growth in the economy.

Indeed, the fiscal impulse is anticipated to be flat through the period to FY29 and the Budget is anticipating that deficits are likely to be $45 billion lower over the coming five years. However, it is important to note that most of this improvement is expected to come from inflation, a slight pick-up in migration expectations, and economic growth. As we note below, we think some of the assumptions around the outlook are quite optimistic. Looking further ahead, the Budget is expected to get back into balance in FY35.

At the margin, this is some (albeit small) relief for the Reserve Bank of Australia (RBA) given they have been highlighting the excess demand that currently exists in the economy.

The graph below shows the historic and expected budget position in coming years.

Source: LSEG Datastream, Australian Treasury May 2026. Orange bars reflect Treasury projections.

Turning our attention to the debt situation, net debt is anticipated to increase from 19.9% of GDP in FY26 to a peak of 21.9% of GDP in FY29. Interest payments are expected to reach around 0.9% of GDP in FY29. This is a marginal improvement relative to previous expectations, which is supportive of Australia’s credit rating of AAA with a stable outlook.

Economic outlook

The Budget’s assumptions on the economic outlook look more optimistic than the RBA’s, and we tend to lean with the RBA. The Budget expects economic growth to be meaningfully higher over the next two years relative to the RBA. We expect economic growth to remain below trend for the next two years, whilst inflation is expected to remain largely above target—with an uplift to 5% this financial year, given the increase in oil prices.

Household consumption is expected to be sluggish, weighed down by the increase in interest rates. The risks around the consumer outlook are balanced right now. It is possible that we see a more protracted slowdown in spending as the RBA interest rate hikes have an impact. On the other hand, we could see a version of the K-shaped economy emerge—where higher income, asset-rich consumers drive spending forward.

Two key risks to the Australian outlook and Budget are protracted tension in the Middle East and a steep decline in the Chinese economy. Our base case is that the Middle East tensions ease given the pressures of the mid-term elections in the United States. The Treasury notes that in the event of a protracted conflict where the oil price was to rise to USD $200 per barrel, inflation would likely peak at close to 7%. We think the Chinese economy is still in a tough spot, but we have seen some early signs of stabilisation. It is important to note that the Budget has maintained the conservative forecasts for the iron ore price that they have held over the last couple of years.

The changes to the capital gains tax and negative gearing will likely have mixed implications for the housing market. Negative gearing will only become available for newly constructed dwellings (existing investment properties are grandfathered), so this could provide an incentive for more housing supply. However, we expect the impact will be marginal. In the near term, the combination of these changes to negative gearing and capital gains taxes are likely to see mild upward pressure on rents.

Implications for portfolios

As noted above, we think that the Australian economy faces some headwinds, as a result of weak consumer confidence and the tightening of monetary policy. Additionally, as noted above, there is very little fiscal impulse coming to support the Australian economy. As a result, we largely prefer international equities compared to Australian equities.

Our multi-asset portfolios, and Australian fixed income portfolios, are overweight Australian duration (i.e., interest rate exposure). We believe government bonds offer attractive value in Australia and should benefit if we see a more meaningful slowdown.

One potential implication of the changes to taxation policy is that superannuation has become a more tax-efficient vehicle relative to other investments (in particular properties).

What the Budget means for superannuation

Significant superannuation related Budget night announcements are becoming rare—with no new major superannuation changes in the Government’s ‘Resilience and Reform’ themed Budget.

There were, however, a number of tax related announcements that will likely impact superannuation investing and the flow of money in and out of super. The Government also re-announced its ongoing review of the superannuation performance test which aims to ensure the test does not create unintended consequences to investment and that it fully aligns with super members’ long-term interests.

More broadly, the Government announced a number of initiatives, which aim to boost economic productivity by streamlining the regulatory system and uplifting Digital Identification. These will (hopefully) have positive flow on impacts for super.

Tax reform

While super was by and large exempt from the proposed investment related tax changes, they may impact the relative attractiveness of super vs non-super investments, and of the different asset classes. If these reforms are legislated, we expect some changes to individuals’ wealth creation and asset allocation strategies.

The key changes proposed were:

- Change in Capital Gains Tax (CGT) discount rules. From 1 July 2027 the 50% discount will revert back to the pre-1999 approach of cost-base plus CPI indexation. A minimum 30% tax rate on net capital gains will also apply.

- Negative gearing tax deductions will be limited from 1 July 2027 to new builds or investments in ‘affordable housing’. Properties purchased before Budget night will be exempt and will continue to be able to be negatively geared.

- From 1 July 2028, a new minimum 30% tax on taxable income of discretionary trusts.

The Government also announced a new Working Australians Tax Offset (WATO). The $250 offset for all working Australians will apply from the 2027-28 financial year, and is expected to be a permanent benefit that will benefit over 13 million Australian workers.

Existing changes from 1 July 2026

With no amendments announced in the Budget, the following changes will occur as scheduled from 1 July 2026:

- Payday super – Employers must send super contributions when salary and wages are paid, instead of waiting until the end of the quarter. This important measure means that these contributions are invested sooner, and it increases the visibility of super payments.

- The Government will pay superannuation on Commonwealth Government-funded Paid Parental Leave (PPL) for parents of babies born on or after 1 July 2025, with the payments made annually to individuals’ super fund accounts from 1 July 2026.

- Individual income tax cuts. From FY26-27 the tax rate on the $18,201 – $45,000 bracket will decrease by 1% as per the table below.

| Income range ($) | Rates in 2025-26 (percent) | Rates in 2026-27 (percent) | Rates in 2027-28 (percent) |

|---|---|---|---|

| 0-18,200 | Tax free | Tax free | Tax free |

| 18,201-45,000 | 16 | 15 | 14 |

| 45,001-135,000 | 30 | 30 | 30 |

| 135,001-190,000 | 37 | 37 | 37 |

| > 190,000 | 45 | 45 | 45 |

Source: ATO

The Australian Taxation Office (ATO) recently released details of the various thresholds that will apply for FY27:

- The general Transfer Balance Cap (the maximum a person can transfer to a tax-free pension product) will increase from $2 million to $2.1 million. The Cap is indexed to the Consumer Price Index (CPI) in increments of $100,000.

- The Concessional Contributions Cap will increase from $30,000 to $32,500 and the Non-concessional Contributions Cap will increase from $120,000 (four times the concessional cap) to $130,000. The concessional contributions caps are indexed to wages (Average Weekly Ordinary Time Earnings or AWOTE) in increments of $2,500 and did not increase last year.