Year-end strategies for advisors. Will you make SANTA’s "nice" list?

Executive summary:

- Now is the time for advisors to prepare for a strong start to 2024.

- The letters in SANTA's name help spell out a series of strategies advisors can adopt to get the new year off on the right foot.

- The list spans ideas to grow your practice, to improve the tax-efficiency of your clients' portfolios, as well as how to get your clients back into equities.

When I was growing up, Christmas was my favorite time of year. There were colorful lights everywhere, and all my cares would just fade away as Christmas neared. My favorite toy of all time was my Voltron set. If you know, you know. Before I got that toy, I remember my parents asking if I was on Santa's naughty or nice list? I am not going to sugarcoat it… I definitely had to put in some work before the big day. Thankfully, I did get on the nice list that year, but it was a close call.

As I start thinking about Christmas this year, I decided I want to be on the nice list again, so I put together some useful year-end actions and ideas for financial advisors. I might not get a Voltron set again, but hopefully some advisors find this list helpful. Let's be honest, who doesn't like a good list? To make this one a little more interesting, I wanted to pay homage to the bearded man himself, SANTA.

Segment your client base

Ask better questions

New customized investment approaches

Tax-Loss Harvesting

Address how to move cash off the sidelines

Segment your client base

Segmentation is something I always talk about with advisors, however very few of them actually go through the process. We have all heard about the 80/20 rule, but have you heard about the 50/5 rule? It posits that 50 percent of your book produces less than 5 percent of your revenue. That means your best clients are subsidizing the rest of your book.

I know advisors can't or don't want to segment their clients, but segmentation has huge benefits for both the client and the advisor. When clients are put in the right service model, they feel heard and valued. This allows the advisor to spend time with the right clients. Remember "You have to treat clients fairly, not equally." Segmentation will also make it easier for an advisor to determine the value of their book of business.

This becomes important when an advisor is thinking about succession planning. My first question to an advisor who asks me about succession is: "have you got a valuation on your book?" Deals are all over the board, so you better know what your book is worth. Segmenting by revenue and age will allow an advisor to get a better handle on the worth of his or her business. Here at Russell Investments, we can help you with segmentation. We have been helping clients through this process for many years. I have personally had the segmentation discussion with more than 100 advisors.

Ask better questions

I have always said one of the ways an advisor can get better is by learning how to ask better questions. I wrote a blog on this topic a while ago. The reason I bring this up again is that many of our clients' goals and lives have radically changed in the past five years. Their thoughts on retirement have also probably changed.

I personally think that as adults, we change our outlook every 10 years or so. I don't have science or numbers to back that up. Still, I believe that I am a completely different person now than I was when I was 38, and even more so than when I was 28 and, well, you can imagine me at 18… just imagine more hair and a hemp necklace and jean shorts.

Sorry about taking you down this particular rabbit hole, but I am trying to illustrate that the questionnaire you did with that client 10 years ago likely needs to be updated. No one really wants to do an old school "check the box" questionnaire. Most clients still need help clarifying their goals. If you ask good questions, clients will naturally share important details about their lives that you can use to help them map out their goals. Be that advisor and ask better questions and help guide your clients to where they want to go.

New customized investment approaches

When I first got in the financial services industry in 1997 not many advisors did financial planning. There was also not a lot of talk about turnkey solutions or model portfolios. My, my how things have changed. The amount of personalization that you can offer clients is mindboggling now. The main product to provide that personalized investment plan that many advisors are using currently is Direct Indexing. Direct indexing is a topic we at Russell Investments have been talking about for a while now. If you want to learn more about it, here's a guide to Direct Indexing that we produced. The reason it has become so popular is because of the way it can help you manage a client's tax liabilities and the level of customization you can provide. We all know that if you can customize a product to a client's exact need, they are more likely to stay in it. Why do you think the online personal style service Stitch Fix is so popular? If people are provided with a more customized approach, they might be more willing to stick with a product longer. If you have more questions on Direct Indexing, please contact us.

Tax-Loss Harvesting

I probably don't need to tell any advisor this, but now is the time to tax-loss harvest. Not only is it a good thing for clients, but it also shows clients you are watching their accounts. This activity also gives you a reason to reach out to your clients' CPA (chartered professional accountant) and continue to build that relationship. Hopefully your clients' accounts are not down this year, but if you tax-loss harvest you will have at least one positive thing to talk to clients about.

Also be on the lookout for capital gains in the next couple of weeks. You don't want to be the advisor who puts clients' money to work at the end of the year and then the client gets surprised by a capital gain that is taxed. Those are tough conversations.

Address how to move cash off the sidelines

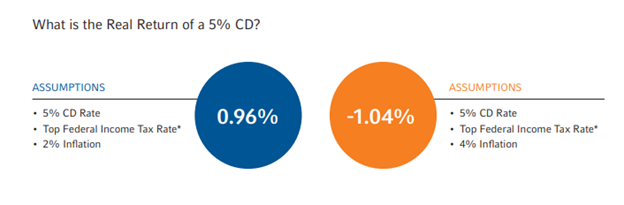

The last topic on this list is what to do with all of this cash that has come in and is sitting on the sidelines. I know there has been a ton of money put into Certificates of Deposit (CDs) and fixed annuities, but I am not sure those yields will give clients enough return to get to their goals.

I recently looked at a McDonald's menu. What do you think a Big Mac combo meal costs? In my neighborhood, it's $11.89. So, if you figure a married couple gets a Big Mac meal each for lunch over 20 years of retirement… That will cost $23.78x7300 days (20 years x 365) = $173,594 just for Big Macs. That does not include tax and that is only one meal per day. As you can see in the chart below, a CD paying 5% might actually not result in 5% going into your client's pocket.

(Click image to enlarge)

Source: Barclays and Russell Investments. Certificates of deposit (CDs) offer a fixed rate of return, and the interest and principal on CDs will generally be insured by the FDIC up to $250,000. Top Federal Income Tax Rate* and Taxable Equivalent Yield: Based on maximum tax rate of 40.8% for Married Filing Jointly, including 3.8% Net Investment Income Tax.

Since your clients are likely not actually getting 5% in CDs they may need to think about adding some equities to their portfolios. Here are some ideas to help clients get into the market.

- DCA. Dollar cost averaging. Look at the graph below. Dollar cost averaging allows the client to invest the same amount over a certain amount of time. This allows the client to take the emotion out of when to put money to work in the market. The market is one of the only things that when it goes on sale no one wants it. If you can get your client to dollar cost average, they are more apt to get in the market because they are not going in all at once.

- Split Ticket. I learned about this idea 20 years ago. If you have a cautious client, have them put 80% of their money into something with a fixed rate of return, and the other 20% in the market. That allows the customer to see most of their money growing slowly while still participating in the market's performance.

- Finally, just sweep the interest your client is getting from the fixed income assets held in the portfolio and put that in the market. You are not reinvesting back into the bonds, but hopefully that money will grow in the stock market.

Dollar cost averaging – Keeping the emotion out of investing

| INVESTMENT DATE |

INVESTMENT AMOUNT |

SHARE PRICE |

SHARES PURCHASED |

| January | $1,000 | $10.00 | 100.00 |

| February | $1,000 | $10.50 | 95.24 |

| March | $1,000 | $11.00 | 90.91 |

| April | $1,000 | $12.00 | 83.33 |

| May | $1,000 | $9.50 | 105.26 |

| June | $1,000 | $9.50 | 105.26 |

| July | $1,000 | $10.00 | 100.00 |

| August | $1,000 | $8.00 | 125.00 |

| September | $1,000 | $7.50 | 133.33 |

| October | $1,000 | $9.00 | 111.11 |

| November | $1,000 | $8.50 | 117.65 |

| December | $1,000 | $10.00 | 100.00 |

| TOTALS | $12,000 (total investment) |

$9.47 (average price/share) |

1267.09 (total shares purchased) |

Whatever you think will get clients to at least dip their toe into the equity market is worth a thought. History has taught us that most people will live longer than they think, retirement will be more expensive than people think and historically the market goes up more than it goes down. Quite frankly equities might be the best chance clients have to eating at McDonald's versus working at McDonald's.

So, before you close your books for the year, really think about what I have just written. Take this list and use it to finish the year out strong and or get a great start to next year. In the meantime, happy holidays everyone!